📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to build wealth in your 30s is one of the most important financial questions you will ever ask — because your 30s are the decade where small financial decisions create the biggest long-term differences. Learning how to build wealth in your 30s means understanding that you still have 30+ years of compound growth ahead, but that the habits and systems you establish now determine your financial trajectory for the rest of your life. This complete guide on how to build wealth in your 30s gives you 10 proven strategies, a clear roadmap, and the exact steps to follow to reach a strong net worth by 40.

Why Your 30s Are the Most Important Decade for Building Wealth

Your 30s are unique for wealth building for three reasons. First, your income is typically higher than in your 20s — giving you more capital to deploy. Second, you still have 30+ years until retirement — enough time for compound interest to turn $1,000 into $7,600 at 7% annual returns. Third, the financial habits you establish in your 30s — saving rate, investment discipline, debt management — tend to stick for life.

The decade between 30 and 40 is when most Americans either start building serious wealth or fall further behind. The difference between those two outcomes is almost entirely behavioral — not income. Read our guide on what is net worth to understand the exact number that measures your progress.

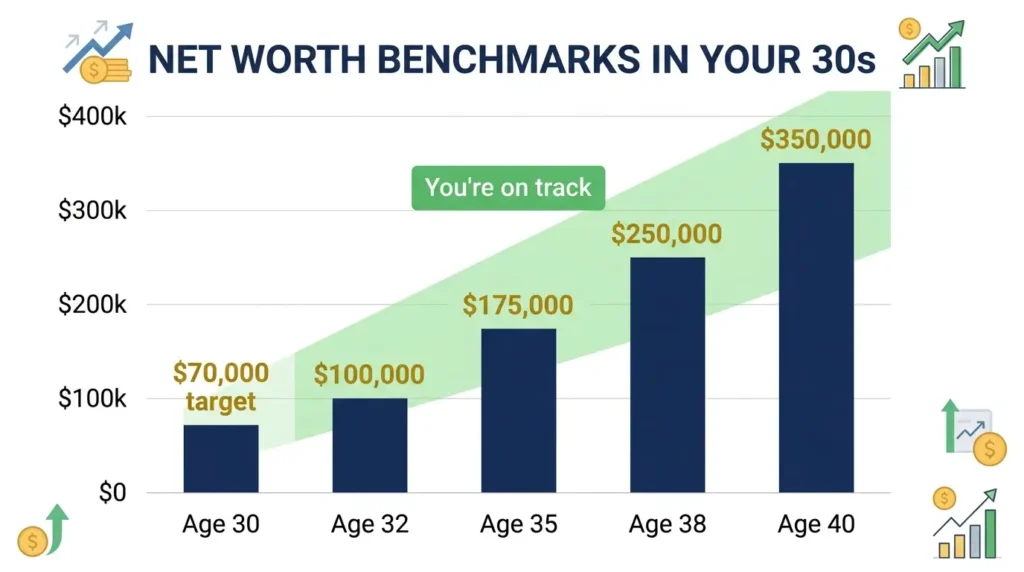

Where Should Your Net Worth Be in Your 30s?

Before diving into how to build wealth in your 30s, it helps to know where you stand. A commonly used benchmark is to have net worth equal to your annual salary by age 30, and three times your salary by age 40. Here are typical targets across income levels:

| Age | Net Worth Target (1x salary = $70K) | Net Worth Target (1x salary = $100K) |

|---|---|---|

| 30 | $70,000 | $100,000 |

| 35 | $175,000 | $250,000 |

| 40 | $210,000 | $300,000 |

If you are behind these benchmarks, do not panic — focus on the strategies below. If you are ahead, accelerate. The benchmarks are guides, not verdicts.

Strategy 1 — Eliminate All High-Interest Debt First

You cannot build wealth in your 30s while paying 20%–28% APR on credit card debt. High-interest debt is a guaranteed negative return — every dollar sitting in a credit card balance is costing you more than any investment can reliably earn. Before any other wealth-building step, eliminate all credit card and high-interest personal loan debt.

Use the debt avalanche (highest rate first) for maximum savings, or the debt snowball (smallest balance first) if you need motivational momentum. Read our guide on how to get out of credit card debt for the complete strategy. Low-interest debt like student loans below 4% or a mortgage can coexist with investing.

Strategy 2 — Build a 3-to-6 Month Emergency Fund

In your 30s, the stakes of a financial emergency are higher — mortgage, car payment, children, larger monthly obligations. A 3–6 month emergency fund is no longer optional — it is the foundation that allows you to build wealth in your 30s without being derailed by life’s inevitable surprises. Without it, every unexpected expense becomes a credit card charge that unravels your progress.

Keep your emergency fund in a high-yield savings account earning 4%–5% APY. For the full emergency fund strategy, read our guide on how to build an emergency fund.

Strategy 3 — Max Out Your 401(k) and Capture Every Dollar of Employer Match

To build wealth in your 30s aggressively, your 401(k) should be a top priority. The 2026 contribution limit is $24,500 for workers under 50. If maxing out the full limit is not yet achievable, at minimum contribute enough to capture every dollar of your employer match — that is a guaranteed 50%–100% return on your contribution that no investment can match.

For everything you need to know about this account, read our guide on what a 401(k) is.

Strategy 4 — Open and Max Your Roth IRA Every Year

The Roth IRA is one of the most powerful tools to build wealth in your 30s — all growth is completely tax-free, and qualified withdrawals in retirement are tax-free. Contributing $7,500/year from age 30 to 65 at a 7% average return produces approximately $1,150,000 — entirely tax-free. Every year you skip a Roth IRA contribution in your 30s is a compounding year permanently lost.

Read our complete guide on what a Roth IRA is to open one today. Use low-cost index funds like an S&P 500 ETF as your primary investment inside the account.

Strategy 5 — Invest Consistently in a Taxable Brokerage Account

Once your Roth IRA is maxed, open a taxable brokerage account and invest additional savings into low-cost index funds. There is no contribution limit on a taxable brokerage account — allowing you to accelerate wealth building in your 30s beyond what retirement accounts allow. Use dollar-cost averaging — investing a fixed amount every month regardless of market conditions — to build this account consistently over time.

Strategy 6 — Increase Your Income Intentionally

Your income is the single most powerful lever to build wealth in your 30s. A 10% raise invested consistently produces far more wealth than a 10% increase in investment returns. Strategies to increase income in your 30s:

- Ask for a raise at your annual review with market data in hand

- Develop high-value skills — certifications, languages, specialized software

- Consider a higher-paying role at a different company — job switching typically produces 15–25% salary increases

- Build a side income stream that can be scaled — freelancing, consulting, digital products

- Direct 100% of every income increase to wealth-building, not lifestyle inflation

Strategy 7 — Buy a Home Strategically

Homeownership is one of the most effective ways to build wealth in your 30s — but only when done strategically. Buying too much house, with too little down payment, in an overpriced market can destroy wealth rather than build it. Guidelines for smart home buying in your 30s:

- Keep housing costs below 28% of gross monthly income

- Put at least 10%–20% down to avoid PMI and build equity faster

- Buy in a market with growing employment and population — not just where prices seem cheap

- Plan to stay at least 5–7 years — transaction costs mean short-term ownership rarely builds wealth

For the down payment savings strategy, read our guide on how to save for a house down payment.

Strategy 8 — Avoid Lifestyle Inflation

Lifestyle inflation is the wealth killer of the 30s. As income rises, most people automatically increase their spending on cars, housing, dining, and vacations — consuming every income gain before it can build wealth. The secret to building wealth in your 30s is maintaining a relatively stable lifestyle while income grows, and directing the difference to investments and retirement accounts.

A practical rule: when you receive a raise, save at least 50% of the increase and allow yourself to spend the other 50%. This approach creates growing savings without feeling like deprivation.

Strategy 9 — Protect Your Wealth with Adequate Insurance

One of the most overlooked ways to build wealth in your 30s is protecting the wealth you are already building. In your 30s, adequate insurance coverage is essential:

- Term life insurance — if you have dependents, a 20–30 year term policy replaces your income if you die prematurely

- Disability insurance — your greatest financial asset is your ability to earn income. Long-term disability insurance replaces 60%–70% of income if you cannot work.

- Health insurance — a serious illness without insurance can wipe out a decade of savings

- Umbrella liability insurance — protects your growing assets from lawsuits

Strategy 10 — Track Your Net Worth Every Quarter

You cannot build wealth in your 30s consistently without measuring it. Calculate your net worth every 3 months — add up all assets, subtract all liabilities. Tracking your net worth quarterly keeps you accountable, shows you what is working, and motivates continued progress. Most people who track their net worth consistently make better financial decisions simply because they see the impact of every choice.

The Wealth Building Roadmap for Your 30s

| Priority | Action | Target |

|---|---|---|

| 1 | Eliminate high-interest debt | All credit cards and high-rate loans gone |

| 2 | Build emergency fund | 3–6 months of expenses in HYSA |

| 3 | 401(k) to full employer match | Never leave free money on the table |

| 4 | Max Roth IRA | $7,500/year every year |

| 5 | Max 401(k) | $24,500/year |

| 6 | Taxable brokerage investing | No limit — invest every extra dollar |

| 7 | Home purchase (if appropriate) | 20% down, housing <28% income |

| 8 | Track net worth quarterly | 1x salary by 30, 3x by 40 |

Frequently Asked Questions

How to build wealth in your 30s starting from zero?

Starting from zero in your 30s is completely recoverable. The order of operations: eliminate high-interest debt, build a $10,000 emergency fund, capture your 401(k) employer match, open a Roth IRA and contribute monthly, then invest in index funds. Increasing your income simultaneously accelerates every step. You still have 30+ years of compounding ahead.

How much should I have saved by 35?

A common benchmark is to have approximately 1.5–2 times your annual salary saved by age 35. On a $75,000 salary, that is $112,000–$150,000. This includes all savings, retirement accounts, and investments combined — but not home equity. If you are behind, focus on increasing your savings rate and income rather than comparing to benchmarks.

Is it too late to build wealth in your 30s?

Absolutely not. Starting to build wealth in your 30s still gives you 30+ years of compound growth before retirement. A 35-year-old investing $1,000/month at 7% annual return will have over $1.2 million by age 65. The best time to start was in your 20s — the second best time is right now.

What is the fastest way to build wealth in your 30s?

The fastest way to build wealth in your 30s combines three actions simultaneously: increase your income (job switch, negotiate raises, side income), aggressively save and invest every income increase (avoid lifestyle inflation), and invest in low-cost index funds consistently through a Roth IRA and 401(k). All three together create compounding wealth at maximum speed.

Should I pay off my mortgage or invest in my 30s?

For most people in their 30s with a mortgage rate below 5%, investing produces better long-term results than paying down the mortgage aggressively. The stock market has historically returned 7–10% annually — above most 30s mortgage rates. Always max your Roth IRA and 401(k) before making extra mortgage payments. Exception: if your mortgage rate is above 6%–7%, extra payments become more competitive with expected investment returns.

Final Thoughts: Build Wealth in Your 30s One Decision at a Time

How to build wealth in your 30s is not a single dramatic decision — it is the accumulation of hundreds of smaller, consistent choices made month after month. Pay off debt. Save the employer match. Max the Roth IRA. Invest the raise. Skip the lifestyle upgrade. Track the net worth. Each action alone seems small. Together over a decade, they produce financial freedom.

Start with the first unchecked item on the roadmap above and do it this week. Building wealth in your 30s does not require a perfect plan — it requires consistent action on the right priorities. Your 40s and 50s self will live the life your 30s decisions created.

Copy tout