📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is a 529 plan? A 529 plan is a tax-advantaged savings account specifically designed to save for education expenses — and it is one of the most powerful tools available for parents who want to help their children avoid student loan debt. Understanding what is a 529 plan is essential for any family thinking about future college costs, because the tax-free growth and tax-free withdrawals make a 529 plan far more efficient than a regular savings account. This complete guide on what is a 529 plan covers how it works, contribution limits for 2026, what expenses qualify, and how to open one today.

What Is a 529 Plan — The Simple Definition

A 529 plan is a state-sponsored, tax-advantaged investment account designed to save for education costs. The name “529” comes from Section 529 of the Internal Revenue Code. When you contribute to a 529 plan, your money grows tax-free — and when you withdraw it for qualified education expenses, you pay no federal income tax on the gains. In many states, contributions also qualify for a state tax deduction.

Think of a 529 plan as a Roth IRA specifically for education. You contribute after-tax dollars, the money grows tax-free, and qualified withdrawals are completely tax-free. To understand how tax-free growth compounds over 18 years, read our guide on what is compound interest.

How Does a 529 Plan Work?

Here is the step-by-step process of how a 529 plan works:

- You open a 529 plan account — either through your state’s plan or a private plan from a brokerage

- You name a beneficiary — the child or person who will use the funds for education

- You contribute money — there is no annual contribution limit, but gift tax rules apply above $19,000/year (2026)

- The money is invested — in age-based portfolios or funds you select, similar to a 401(k)

- The money grows tax-free — all gains are sheltered from federal income tax while in the account

- You withdraw for qualified expenses — tuition, fees, books, room and board, and more. No federal tax on the withdrawal.

What Expenses Qualify for a 529 Plan?

To withdraw from a 529 plan tax-free, the funds must be used for qualified education expenses. In 2026, qualified expenses include:

- Tuition and fees at accredited colleges, universities, and vocational schools

- Room and board (up to the school’s published cost of attendance)

- Required textbooks, supplies, and equipment

- Computers and technology required for enrollment

- Special needs services for students with disabilities

- K–12 tuition — up to $10,000 per year per child at private, public, or religious schools

- Student loan repayment — up to $10,000 lifetime per beneficiary (SECURE Act)

- Apprenticeship program costs — registered with the Department of Labor

Non-qualified withdrawals are subject to income tax on the gains plus a 10% penalty — so using 529 funds for non-education expenses is expensive. Plan contributions carefully.

529 Plan Contribution Limits in 2026

What is a 529 plan’s contribution limit? There is no annual contribution limit set by the IRS for 529 plans. However, contributions above the annual gift tax exclusion ($19,000 per person in 2026) may trigger a gift tax filing requirement. 529 plans do have lifetime balance limits — typically $300,000 to $550,000 depending on the state.

| 529 Plan Rule | 2026 Details |

|---|---|

| Annual gift tax exclusion | $19,000 per contributor per beneficiary |

| 5-year superfunding option | Up to $95,000 ($190,000 per couple) contributed at once |

| Lifetime balance limit | $300,000–$550,000 (varies by state) |

| Federal income tax deduction | None — contributions are after-tax |

| State tax deduction | Available in most states (varies by plan) |

| Rollover to Roth IRA (SECURE 2.0) | Up to $35,000 lifetime after 15 years in the account |

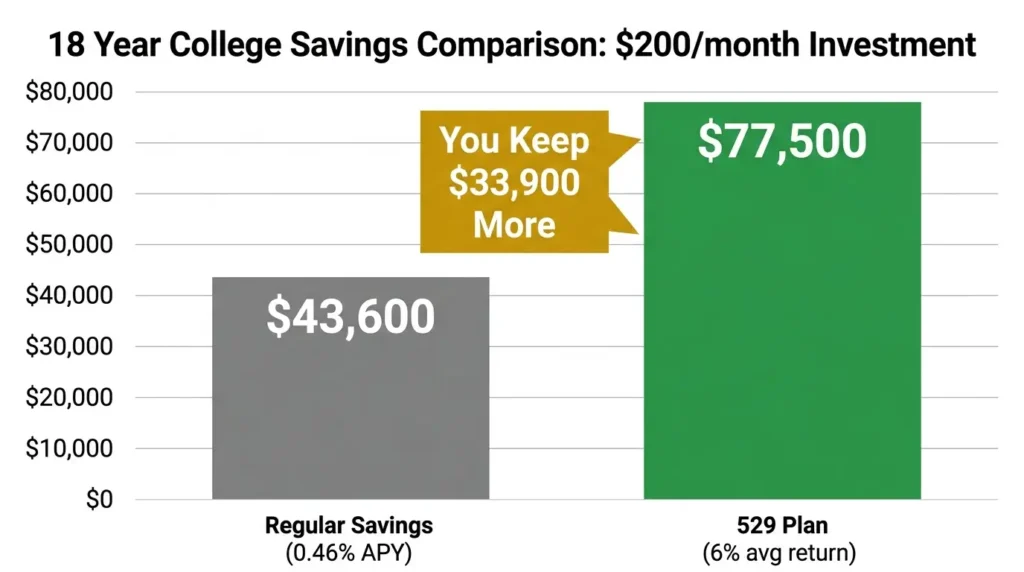

529 Plan vs Regular Savings Account

Why use a 529 plan instead of just saving in a high-yield savings account? The tax-free growth advantage is dramatic over 18 years:

| Account Type | $200/month for 18 years | Average Return | Final Balance | Tax Owed on Withdrawal |

|---|---|---|---|---|

| Regular Savings (HYSA) | $43,200 contributed | ~4.75% | ~$63,000 | Taxes on all gains |

| 529 Plan (invested) | $43,200 contributed | ~6–7% | ~$77,500–$87,000 | $0 (tax-free for education) |

The 529 plan produces $14,000–$24,000 more — entirely tax-free — compared to a regular savings account on the same monthly contribution. The combination of higher investment returns and zero tax on gains is the core advantage of what is a 529 plan.

529 Plan vs Roth IRA for College Savings

Some parents consider using a Roth IRA for college savings instead of a 529 plan. Here is how they compare:

| Feature | 529 Plan | Roth IRA |

|---|---|---|

| Purpose | Education only | Retirement first, education possible |

| Contribution limit | No annual limit (gift tax applies) | $7,500/year (2026) |

| Tax-free growth | Yes | Yes |

| Tax-free withdrawal | Yes (for education) | Yes (for retirement, contributions anytime) |

| Penalty for non-education use | 10% + income tax on gains | No (contributions); 10% + tax on early earnings |

| Impact on financial aid | Parent asset — lower impact | Not counted as asset (better for aid) |

For most parents, the 529 plan is the better choice for college savings — higher contribution limits and no restriction on the amount invested. The Roth IRA is better preserved for retirement. Read our guide on what a Roth IRA is for the full retirement savings strategy.

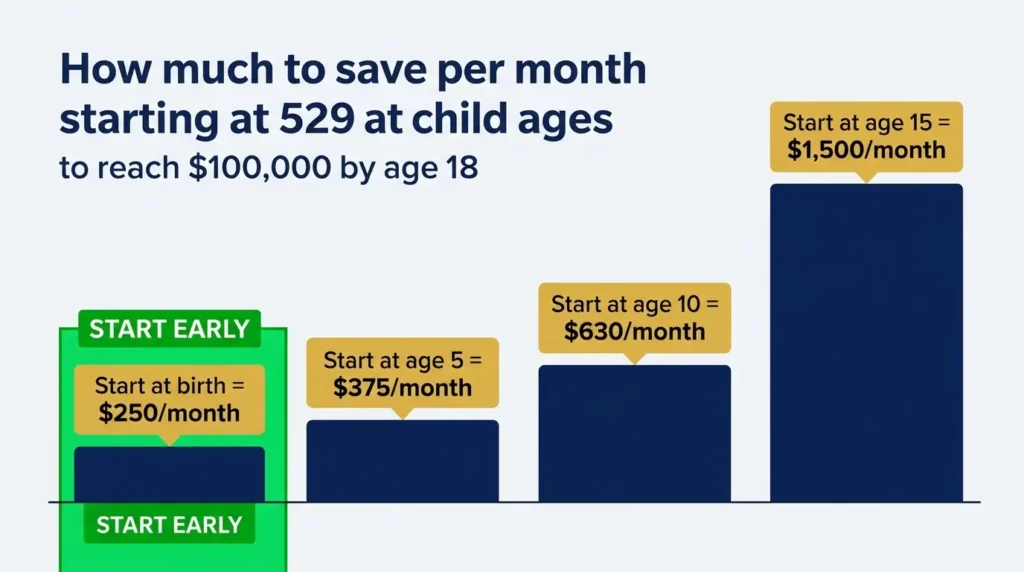

How Much Should You Save in a 529 Plan?

The right monthly contribution to a 529 plan depends on when you start and what your college cost target is. Here is a guide based on reaching approximately $100,000 by age 18 (a reasonable estimate for 4 years at a public university in 2026), assuming a 6% average annual return:

| Child’s Age When You Start | Monthly Contribution Needed | Total Contributed | 529 Balance at 18 |

|---|---|---|---|

| Birth (0) | $250/month | $54,000 | ~$97,000 |

| Age 3 | $315/month | $56,700 | ~$100,000 |

| Age 5 | $380/month | $59,280 | ~$100,000 |

| Age 10 | $635/month | $57,150 | ~$100,000 |

| Age 15 | $1,540/month | $55,440 | ~$100,000 |

Starting at birth versus age 10 cuts the required monthly contribution by nearly 60%. This is the power of compound interest applied to college savings — every year of early investing dramatically reduces the monthly burden. Use dollar-cost averaging to invest consistently every month regardless of market conditions.

How to Open a 529 Plan

- Choose a plan — you can open any state’s 529 plan, not just your own state’s. Compare fees and investment options. Look for low-cost plans with index fund options.

- Go to the plan’s website — most 529 plans can be opened entirely online in 15–20 minutes

- Provide personal information — your name, address, Social Security number, and the beneficiary’s information

- Fund the account — link your bank account and make an initial contribution (many plans accept $25–$50 to start)

- Choose investments — select an age-based portfolio (automatically adjusts as your child ages) or choose your own index fund options

- Set up automatic contributions — a monthly automatic transfer is the most effective approach

The most highly rated 529 plans in 2026 for low costs and investment options include Utah’s my529, Nevada’s Vanguard 529, and New York’s Direct Plan. Any of these can be opened by residents of any state. For the same disciplined approach applied to general investing, read our guide on how to start investing with $100.

What Happens If Your Child Does Not Go to College?

This is one of the most common concerns about what is a 529 plan — and the fear is largely outdated in 2026:

- Change the beneficiary — you can change the beneficiary to any family member at any time, including siblings, cousins, even yourself

- Use for K–12 or vocational training — up to $10,000/year can be used for private K–12 tuition; vocational schools and apprenticeships also qualify

- Roll over to a Roth IRA — under SECURE 2.0 (2024), after 15 years in the account, up to $35,000 can be rolled into a Roth IRA for the beneficiary

- Use for student loan repayment — up to $10,000 lifetime per beneficiary

- Withdraw non-qualified — you pay income tax plus a 10% penalty only on the gains portion, not the contributions

Frequently Asked Questions

What is a 529 plan and how does it work?

A 529 plan is a tax-advantaged savings account designed for education expenses. You contribute after-tax dollars, the money grows tax-free in investments, and withdrawals for qualified education expenses (tuition, books, room and board) are completely tax-free at the federal level. Many states also offer a state income tax deduction for contributions.

How much can I contribute to a 529 plan in 2026?

There is no annual IRS contribution limit for 529 plans, but contributions above $19,000 per year per beneficiary (2026 gift tax exclusion) may require a gift tax filing. You can also superfund up to $95,000 ($190,000 per couple) at once using 5-year gift tax averaging. State-specific lifetime balance limits range from $300,000 to $550,000.

What happens to a 529 plan if my child doesn’t go to college?

You have several options: change the beneficiary to another family member, use the funds for K–12 tuition, vocational school, or student loan repayment (up to $10,000), or roll up to $35,000 into a Roth IRA for the beneficiary after 15 years (SECURE 2.0). Non-qualified withdrawals incur income tax plus a 10% penalty only on the gains — not the contributions.

Is a 529 plan worth it?

Yes, for most families — especially those who start early. The combination of tax-free growth and tax-free withdrawals produces significantly more college savings than a regular savings account over 10–18 years. State tax deductions on contributions add further value. The flexibility added by SECURE 2.0 (Roth IRA rollover option) also reduces the risk of overfunding.

Can grandparents contribute to a 529 plan?

Yes — grandparents, aunts, uncles, family friends, or anyone can contribute to a 529 plan. Each contributor can give up to $19,000 per beneficiary per year (2026 gift tax exclusion) without gift tax implications. Under the new FAFSA rules effective 2024, grandparent-owned 529 plans no longer negatively impact a student’s financial aid eligibility.

Final Thoughts: What Is a 529 Plan and Why Start Today

What is a 529 plan? It is the most tax-efficient way to save for your child’s education — and the earlier you start, the more powerful it becomes. A 529 plan transforms the burden of college costs from a crisis into a manageable, planned expense — and with the SECURE 2.0 Roth IRA rollover option, the risk of overfunding is lower than ever.

Open a 529 plan today, contribute whatever you can, and set up a monthly automatic contribution. Even $50 or $100 per month started at birth grows into a meaningful college fund by age 18. The families who struggle most with college costs are those who waited to start — or never started at all. Do not let that be you. Once your 529 plan is running, make sure your own retirement savings are also on track by reading our guide on saving for retirement at 25 — always fund your retirement before or alongside your child’s 529 plan.