📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

If you’ve heard the words “Roth IRA” but aren’t sure what they mean — or whether you need one — you’re in the right place. A Roth IRA is one of the most powerful retirement tools available to Americans, yet millions of people either don’t have one or don’t fully understand how to use it.

In this complete guide, you’ll learn exactly what a Roth IRA is, how it works, who qualifies, the 2026 contribution limits, and how to open one in 15 minutes — even if you’re a complete beginner. If you’re just starting out, read our guide on what is a credit score first to build your personal finance foundation.

What Is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a special type of retirement savings account that offers a unique tax advantage: you pay taxes on the money before you put it in — and then everything grows tax-free forever.

That means when you withdraw your money in retirement, you pay zero taxes on both your contributions and all the investment gains you’ve accumulated over the years.

Compare that to a traditional IRA or 401(k), where you get a tax break now but pay taxes when you withdraw in retirement. With a Roth IRA, you do the opposite: pay taxes now, enjoy tax-free money later. According to the SEC investor education portal, IRAs are one of the most effective tax-advantaged tools for long-term wealth building available to American investors.

How Does a Roth IRA Work?

Here is a simple breakdown of how a Roth IRA operates:

- You open an account at a brokerage like Fidelity, Charles Schwab, or Vanguard.

- You contribute after-tax dollars — money you’ve already paid income tax on.

- Your money grows tax-free inside the account through investments in stocks, ETFs, mutual funds, or bonds.

- In retirement (age 59½+), you withdraw your money completely tax-free — both contributions and all the gains.

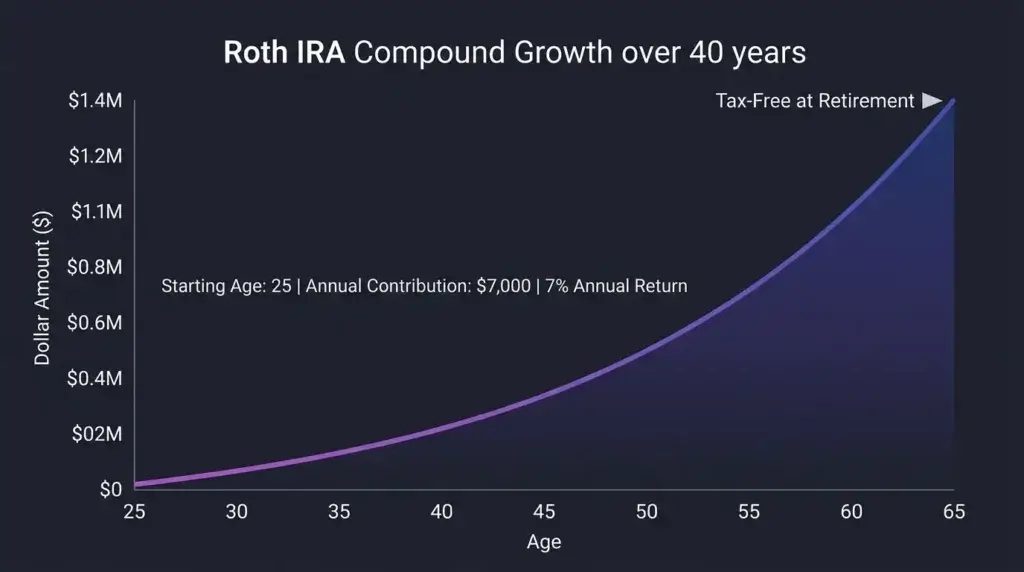

The magic of a Roth IRA is compound growth. If you invest $7,000 per year starting at age 25, and your investments grow at an average of 7% per year, you could have over $1.4 million by age 65 — and pay zero taxes on that entire amount. If you want to start even smaller, read our guide on how to start investing with $100.

Roth IRA Contribution Limits for 2026

The IRS sets annual limits on how much you can contribute. According to the IRS official Roth IRA page, the 2026 limits are:

| Age | 2026 Contribution Limit |

|---|---|

| Under 50 | $7,500 per year |

| Age 50 or older | $8,600 per year (includes $1,100 catch-up) |

These limits apply per person, not per account. Important: You can only contribute earned income — money from a job, freelancing, or self-employment.

Who Qualifies for a Roth IRA? (2026 Income Limits)

Not everyone can contribute to a Roth IRA. Here is who qualifies for 2026:

| Filing Status | Full Contribution | Reduced | No Contribution |

|---|---|---|---|

| Single / Head of Household | Under $153,000 | $153,000–$168,000 | Over $168,000 |

| Married Filing Jointly | Under $242,000 | $242,000–$252,000 | Over $252,000 |

| Married Filing Separately | $0 | $0–$10,000 | Over $10,000 |

If your income exceeds the limit, a “Backdoor Roth IRA” strategy may still allow you to contribute. Consult a financial advisor for this option.

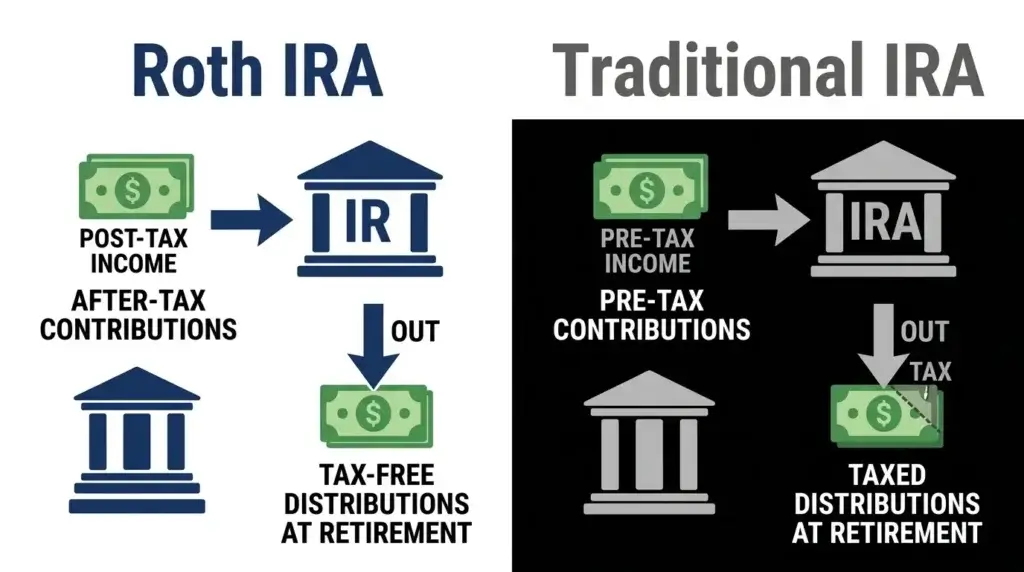

Roth IRA vs Traditional IRA: Key Differences

The two main types of IRAs work in opposite ways. For a detailed comparison, read our complete guide on Roth IRA vs Traditional IRA. Here is a quick summary:

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax on contributions | After-tax | Pre-tax (deductible) |

| Tax on withdrawals | Tax-free ✅ | Taxed as income |

| Required distributions | None required ✅ | Required at age 73 |

| Early withdrawal of contributions | Penalty-free ✅ | 10% penalty + taxes |

| Best for | Young earners, lower bracket now | Higher earners expecting lower taxes later |

Roth IRA Withdrawal Rules

Withdrawing Your Contributions (Anytime)

You can withdraw your original contributions (not the gains) at any time, at any age, with no taxes or penalties. This makes a Roth IRA surprisingly flexible compared to other retirement accounts.

Withdrawing Your Earnings (The 5-Year Rule)

To withdraw your investment gains tax-free and penalty-free, two conditions must both be met: you must be at least 59½ years old, AND your Roth IRA must have been open for at least 5 years. If you withdraw gains before meeting these conditions, you’ll owe income taxes plus a 10% penalty.

Where to Open a Roth IRA in 2026

You can open a Roth IRA at any major brokerage. For a full comparison, check our guide on the best investment apps for beginners. Here are the top options:

- Fidelity — No minimums, no account fees. Best overall for beginners.

- Charles Schwab — No minimums, 24/7 customer support, user-friendly app.

- Vanguard — Best for long-term, hands-off investors. Creator of the index fund.

- Betterment — Robo-advisor that automatically manages your investments.

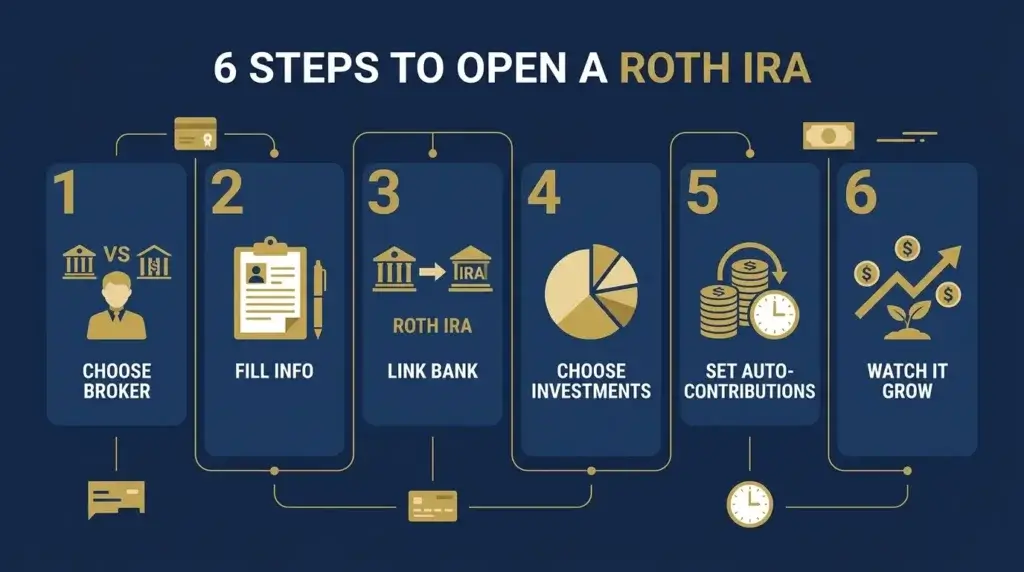

How to Open a Roth IRA: Step by Step

- Choose a brokerage (Fidelity recommended for most beginners)

- Go to their website and click “Open an Account” then “Roth IRA”

- Fill in your personal information: name, Social Security number, employment info

- Link your bank account to make your first deposit

- Choose your investments (or let the robo-advisor choose for you)

- Set up automatic monthly contributions — even $50 per month makes a difference

The entire process takes about 15 to 20 minutes. If you want to understand why starting early matters, read our guide on saving for retirement at 25.

Frequently Asked Questions About Roth IRAs

Can I have both a Roth IRA and a 401(k)?

Yes. Contribute enough to your 401(k) to get the full employer match (free money), then max out your Roth IRA, then put any extra back into your 401(k).

What if I contribute too much to my Roth IRA?

The IRS charges a 6% excise tax on excess contributions. Contact your brokerage immediately to remove the excess before the tax filing deadline.

Can I open a Roth IRA for my child?

Yes. A custodial Roth IRA allows minors with earned income to start investing early — one of the most powerful financial gifts you can give a child.

Is a Roth IRA safe?

The investments inside can go up or down with the market. However, accounts at SIPC-covered brokerages are protected against institutional failure. The longer your time horizon, the more risk you can typically afford.

Can I withdraw Roth IRA contributions without penalty?

Yes. Your original contributions (not earnings) can be withdrawn at any time, at any age, with no taxes or penalties. This is one of the most valuable and misunderstood features of the Roth IRA.

The Bottom Line

A Roth IRA is one of the best financial decisions you can make — especially when you start young. The combination of tax-free growth, flexible withdrawal rules, and no required distributions makes it uniquely powerful. Start now, even with a small amount — time is your greatest asset.

Ready to open your Roth IRA? Start with Fidelity — free, 15 minutes, zero minimums. Then read our comparison: Roth IRA vs Traditional IRA: Which Is Better for You?

Disclaimer: This article is for informational and educational purposes only. It does not constitute tax or financial advice. Consult a qualified tax professional for personalized guidance. Contribution limits are based on IRS guidelines for 2026 and are subject to change.