📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

If you’ve ever applied for a credit card, a car loan, or an apartment, someone checked your credit score. But what exactly is a credit score — and why does this three-digit number have so much power over your financial life?

In this complete guide, you’ll learn exactly what a credit score is, how it’s calculated, what counts as a good score, and how to check yours for free today — no credit card required.

What Is a Credit Score?

A credit score is a three-digit number — typically between 300 and 850 — that tells lenders how likely you are to repay your debts on time. The higher your score, the more trustworthy you appear to banks, landlords, and lenders.

The most widely used credit score is the FICO Score, developed by the official FICO website. Another common model is the VantageScore, created by the three major credit bureaus: Experian, Equifax, and TransUnion.

Think of your credit score like a financial GPA. A high score opens doors — a low score closes them.

Why Does Your Credit Score Matter?

Your credit score affects more areas of your life than most people realize:

- Credit cards — A higher score means access to better rewards and lower interest rates

- Car loans — A score above 700 can save you thousands in interest

- Mortgages — The difference between a 620 and 760 score could mean $100+ more per month

- Renting an apartment — Most landlords run a credit check before approving a tenant

- Insurance premiums — In most states, insurers use your credit score to set rates

- Job applications — Some employers in finance review credit history during background checks

In short, a good credit score opens doors — and a poor one closes them.

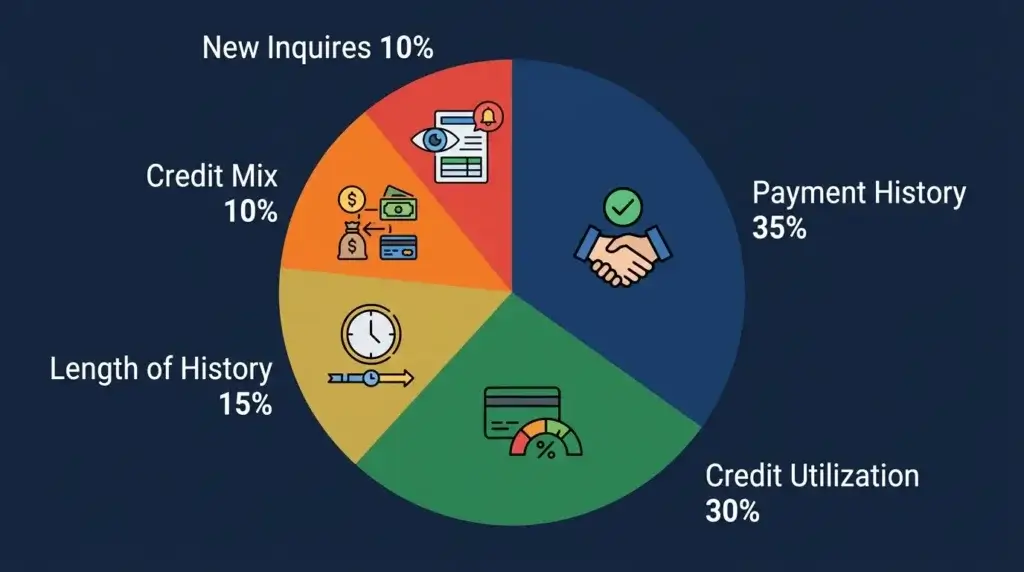

How Is a Credit Score Calculated? The 5 Key Factors

Your FICO credit score is calculated using five factors:

1. Payment History — 35%

This is the most important factor. It simply measures whether you pay your bills on time. A single late payment can drop your score by 50 to 100 points. Consistent on-time payments are the fastest way to build a strong score.

2. Credit Utilization — 30%

This measures how much of your available credit you’re currently using. If your credit card limit is $1,000 and your balance is $300, your utilization is 30%. Experts recommend keeping this below 30% — and ideally below 10% — for the best scores.

3. Length of Credit History — 15%

The longer your credit history, the better. This includes the age of your oldest account, your newest account, and the average age of all accounts. This is why it’s generally not a good idea to close old credit cards.

4. Credit Mix — 10%

Lenders like to see that you can handle different types of credit — credit cards, car loans, mortgages. Having a healthy mix gives your score a small boost.

5. New Credit Inquiries — 10%

Every time you apply for new credit, lenders do a hard inquiry on your report, which can temporarily lower your score by 5 to 10 points. Note: checking your own score is a soft inquiry and does NOT affect your score.

What Are the Credit Score Ranges?

Here is how FICO scores are typically categorized:

- 800–850 — Exceptional: You’ll qualify for the best rates on any financial product

- 740–799 — Very Good: You’ll get excellent rates and terms

- 670–739 — Good: Most lenders will approve you

- 580–669 — Fair: You may qualify but with higher rates

- 300–579 — Poor: Getting approved is difficult

The average American credit score in 2026 is approximately 715 — solidly in the Good range.

How to Check Your Credit Score for Free

You have several options to check your score at no cost:

- Credit Karma — Completely free, no credit card required. Updates weekly.

- Experian — Offers a free FICO Score 8, the most widely used score by lenders.

- Your bank or credit card issuer — Many banks now offer free score access through their apps.

- AnnualCreditReport.com — The official government-authorized site to get your full credit report free once per year.

Pro tip: Your credit score and your credit report are different things. Your score is the three-digit number. Your report is the detailed history behind it. Check both regularly.

How Long Does It Take to Build a Good Credit Score?

If you’re starting from scratch, here is a realistic timeline:

- 0–3 months — Open your first credit card. You won’t have a score yet.

- 3–6 months — Your first FICO score is generated after at least one account has been open for 6 months.

- 6–12 months — With responsible use, you can reach 650–680.

- 1–2 years — Consistently doing the right things can bring you to the 700+ range.

- 3–5 years — Excellent scores of 750+ become reachable with a clean track record.

Frequently Asked Questions

Does checking my credit score hurt it?

No. Checking your own score is a soft inquiry and has zero impact on your score. Only hard inquiries — when a lender checks your score as part of a credit application — can temporarily lower it.

What is the minimum credit score to buy a car?

Most lenders prefer a score of at least 661 for an auto loan. Some dealers offer financing for scores as low as 500, but the interest rate will be significantly higher.

Can I have a good credit score with no credit card?

Yes, but it’s harder. Credit cards are the easiest tool for building credit quickly. Alternatives include credit-builder loans, becoming an authorized user on someone else’s account, or reporting rent payments through services like Experian Boost.

How often does my credit score update?

Your credit score updates whenever your lenders report new information to the bureaus — usually once per month.

The Bottom Line

Your credit score is one of the most important numbers in your financial life. Understanding how it works — and what drives it — puts you in control of your financial future.

The key takeaways: pay every bill on time, keep your credit utilization low, and be patient. Building excellent credit is a marathon, not a sprint.

Ready to take the next step? Check your credit score for free today, then read our guide on How to Build Credit from Scratch to start your journey toward financial freedom.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making financial decisions.