📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

One of the biggest reasons people avoid investing is the fear of choosing the wrong time to buy. What if you invest all your money right before the market crashes? What if you miss the perfect entry point? Dollar-cost averaging (DCA) is a simple strategy that eliminates these worries entirely — and decades of data show it works remarkably well for everyday investors.

In this complete guide, you’ll learn exactly what dollar-cost averaging is, how it works, when to use it, its advantages and limitations, and how to implement it today — even with a small amount of money. If you’re just getting started with investing, also read our guide on what is a Roth IRA to understand the best account to use for your DCA strategy.

What Is Dollar-Cost Averaging?

Dollar-cost averaging (DCA) is an investment strategy where you invest a fixed amount of money at regular intervals — regardless of whether the market is up or down. Instead of trying to invest a lump sum at the “perfect” time, you spread your investments over time.

For example: instead of investing $12,000 all at once in January, you invest $1,000 every month for 12 months. Some months you’ll buy when prices are high, some months when prices are low — and your average cost per share will land somewhere in between.

This approach is already used automatically by millions of Americans — every time you contribute to your 401(k) from each paycheck, you’re practicing dollar-cost averaging without even realizing it.

How Does Dollar-Cost Averaging Work?

The mechanics are simple: you choose an investment (such as an S&P 500 index fund), decide on a fixed amount to invest (such as $200 per month), and set up automatic contributions on a regular schedule.

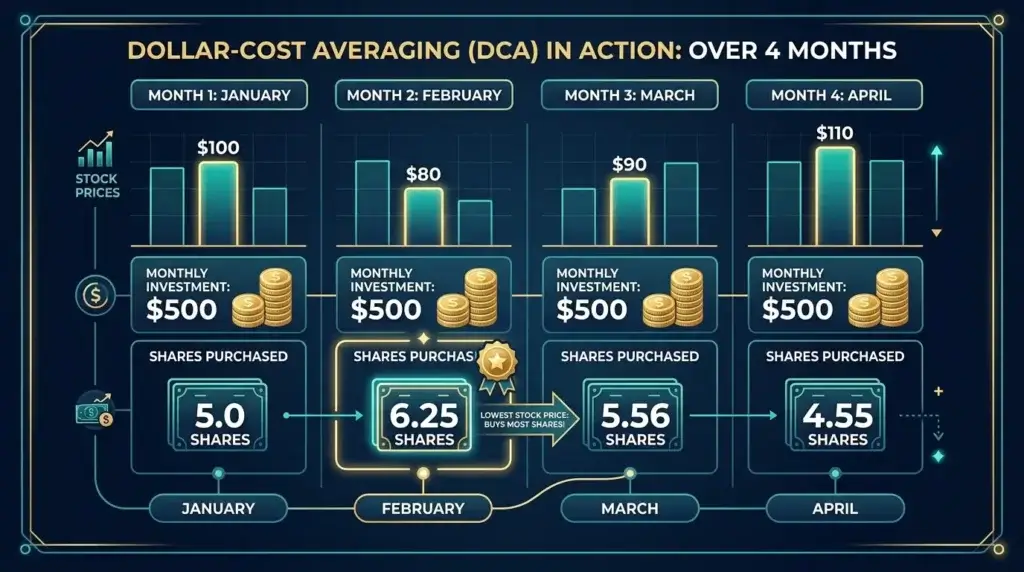

Dollar-Cost Averaging Example

Let’s say you invest $500 per month in an S&P 500 index fund over 4 months:

| Month | Amount Invested | Share Price | Shares Purchased |

|---|---|---|---|

| January | $500 | $100 | 5.0 shares |

| February | $500 | $80 | 6.25 shares |

| March | $500 | $90 | 5.56 shares |

| April | $500 | $110 | 4.55 shares |

| Total | $2,000 | Avg: $94.18 | 21.36 shares |

Notice what happened: by investing the same amount each month, you automatically bought more shares when prices were low (February at $80) and fewer when prices were high (April at $110). Your average cost per share ($94.18) is lower than the simple average of the four prices ($95), even though prices were volatile throughout.

This is the core benefit of dollar-cost averaging: you don’t need to predict the market. The strategy works with the market’s natural volatility to your advantage.

Dollar-Cost Averaging vs Lump Sum Investing

A common question: is it better to invest a large sum all at once (lump sum) or spread it out over time (DCA)? Here is what the research shows:

| Strategy | Best When | Risk Level | Psychological Ease |

|---|---|---|---|

| Lump Sum | Markets are rising long-term | Higher short-term | Difficult — fear of timing |

| Dollar-Cost Averaging | Markets are volatile or falling | Lower short-term | Easy — removes emotion |

Studies by Vanguard and others show that lump sum investing outperforms DCA about two-thirds of the time in rising markets — because more money is invested earlier and has more time to grow. However, DCA significantly outperforms lump sum during market downturns and periods of high volatility.

The practical conclusion: If you have a large sum to invest, lump sum is statistically slightly better in the long run. But for most people who invest from their regular paycheck — which is almost everyone — DCA is not just acceptable, it’s the ideal strategy. The behavioral benefits (removing emotional decision-making) often make DCA the superior real-world choice.

The 5 Key Benefits of Dollar-Cost Averaging

1. Eliminates the Need to Time the Market

Professional fund managers with teams of analysts consistently fail to time the market reliably. DCA removes this pressure entirely. You invest on schedule regardless of market conditions — and your results will closely mirror the market’s long-term performance.

2. Reduces the Impact of Market Volatility

When markets fall, DCA means you’re buying more shares for the same fixed amount. Market dips actually become opportunities rather than sources of anxiety. Over time, this lowers your average cost per share compared to investing everything at a market peak.

3. Removes Emotional Decision-Making

The biggest enemy of successful investing is emotion. Investors who try to time the market often panic-sell during downturns (locking in losses) and FOMO-buy during peaks (overpaying). DCA automates your investing decisions and removes emotion from the equation entirely.

4. Works for Any Budget

You don’t need a large sum to start. DCA works with any amount — $25 per week, $100 per month, or $500 per paycheck. The key is consistency, not the size of each contribution. Read our guide on how to start investing with $100 to see exactly how to begin.

5. Builds the Habit of Consistent Investing

By automating your investments on a schedule, DCA turns investing into a habit rather than a decision. Automatic contributions to your 401(k), Roth IRA, or brokerage account mean you invest without thinking about it — and consistency is the most important factor in long-term wealth building.

The Limitations of Dollar-Cost Averaging

DCA is not perfect. Here are its main limitations:

It Can Underperform in Consistently Rising Markets

If the market rises steadily throughout the year, a lump sum invested in January would have had 12 months of growth, while money invested in December would have had only 1 month. In a bull market, holding cash while waiting to invest each month has an opportunity cost.

Transaction Costs Can Add Up

If you’re paying a commission on each trade, making 12 monthly purchases costs 12 times more in fees than making one annual purchase. However, this is largely irrelevant today since most major brokerages (Fidelity, Schwab, Vanguard, Robinhood) offer commission-free trading.

Requires Discipline and Consistency

DCA only works if you actually stick to it — including during market downturns when it feels psychologically difficult to keep investing. The solution: automate your contributions so you never have to make the decision manually.

How to Implement Dollar-Cost Averaging: Step by Step

Step 1: Choose Your Investment Account

The best accounts for DCA are:

- 401(k) — Automatic DCA with every paycheck. This is already happening if you’re enrolled.

- Roth IRA — Ideal for long-term, tax-free growth. Set up monthly automatic contributions.

- Taxable brokerage account — For investing beyond retirement account limits. Fidelity, Schwab, or Vanguard offer free accounts with no minimums.

Step 2: Choose Your Investment

For most DCA investors, a broad market index fund is the ideal choice:

- S&P 500 index fund — Tracks the 500 largest US companies (e.g., Fidelity ZERO S&P 500 Index Fund, Vanguard VOO)

- Total stock market index fund — Even broader diversification across all US companies

- Target-date fund — Automatically adjusts risk as you approach retirement. Ideal for hands-off investors.

Avoid individual stocks for DCA — diversified index funds reduce single-stock risk and require no research.

Step 3: Set Your Fixed Amount and Schedule

Decide how much you’ll invest and how often. Common schedules:

- Weekly: $50–$100 per week (great if you’re paid weekly)

- Bi-weekly: Aligned with your paycheck schedule

- Monthly: $100–$500 per month (most common)

The amount matters less than the consistency. Starting with $50 per month today is infinitely better than waiting until you can invest $500 per month.

Step 4: Automate Everything

Set up automatic investments so contributions happen without any action from you. Most brokerages and retirement accounts allow you to set recurring investments. Once automated, the only thing you need to do is not interfere — resist the urge to stop contributions when markets fall.

Step 5: Review Annually (Not Monthly)

Check your portfolio once or twice a year to rebalance if needed. Do not check it every day — frequent monitoring leads to emotional decision-making, which is exactly what DCA is designed to prevent.

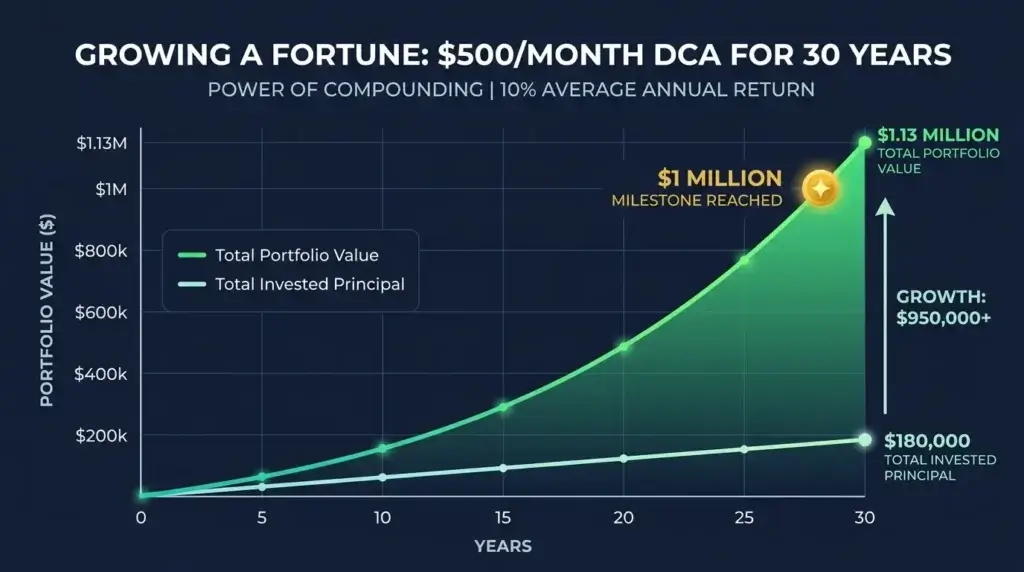

Dollar-Cost Averaging Real-World Results

Here is what DCA looks like in practice over a 10-year period, investing $500 per month in an S&P 500 index fund with an average annual return of 10%:

| Years | Total Invested | Portfolio Value (10% avg return) | Total Gain |

|---|---|---|---|

| 5 years | $30,000 | $38,820 | +$8,820 |

| 10 years | $60,000 | $102,422 | +$42,422 |

| 20 years | $120,000 | $381,750 | +$261,750 |

| 30 years | $180,000 | $1,130,243 | +$950,243 |

Investing just $500 per month consistently for 30 years turns $180,000 of contributions into over $1.1 million — with no market timing, no stock picking, and no financial expertise required. This is the power of DCA combined with compound interest.

Frequently Asked Questions About Dollar-Cost Averaging

Is dollar-cost averaging good for beginners?

Yes — it is arguably the best strategy for beginners. It requires no market knowledge, no timing decisions, and no emotional discipline beyond setting up the automation. It’s how Warren Buffett recommends most people invest their money.

How often should I invest with DCA?

Monthly is the most common and practical frequency for most investors. Weekly works well if you prefer smaller, more frequent contributions. The most important factor is consistency — pick a frequency you can maintain long-term.

Should I stop DCA investing during a market crash?

No — this is actually the worst time to stop. During a market crash, your fixed contribution buys more shares at lower prices, dramatically lowering your average cost. Investors who stopped DCA during the 2020 COVID crash and the 2022 bear market missed some of the best buying opportunities in recent history.

Can I use DCA with individual stocks?

Technically yes, but it’s not recommended for most beginners. Individual stocks carry company-specific risk that index funds eliminate through diversification. If a company goes bankrupt, your DCA investment goes to zero — that can’t happen with a broad market index fund.

What is the minimum amount to start DCA?

With most modern brokerages (Fidelity, Schwab, Robinhood), you can start with as little as $1 using fractional shares. There is no practical minimum. Start with whatever you can afford consistently — even $25 per month builds meaningful wealth over time.

Is DCA the same as automatic investing?

Essentially yes. When you set up automatic monthly contributions to your Roth IRA or 401(k), you are implementing dollar-cost averaging automatically. The strategy and the automation go hand in hand.

The Bottom Line

Dollar-cost averaging is one of the most effective, stress-free investment strategies available — especially for beginners. It doesn’t require you to predict the market, pick the right stock, or invest a large sum all at once. All it requires is consistency.

The best way to implement DCA: open a Roth IRA or contribute to your 401(k), choose a low-cost S&P 500 index fund, set up automatic monthly contributions, and don’t touch it. Time and consistency will do the rest.

Ready to start? Read our guide on how to start investing with $100 to take your first step today. You can also explore the best investment apps for beginners to find the right platform for your DCA journey.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making investment decisions.