📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

If you’re juggling multiple debts — credit cards, personal loans, medical bills — with different interest rates and due dates, debt consolidation might sound like a lifesaver. The idea of combining everything into one manageable monthly payment is appealing. But is it actually worth it?

In this complete guide, you’ll learn exactly what debt consolidation is, how it works, the different types available, the pros and cons, and how to decide if it’s the right move for your financial situation. Understanding your options is also connected to your credit score — consolidation can both help and hurt it depending on how it’s done.

What Is Debt Consolidation?

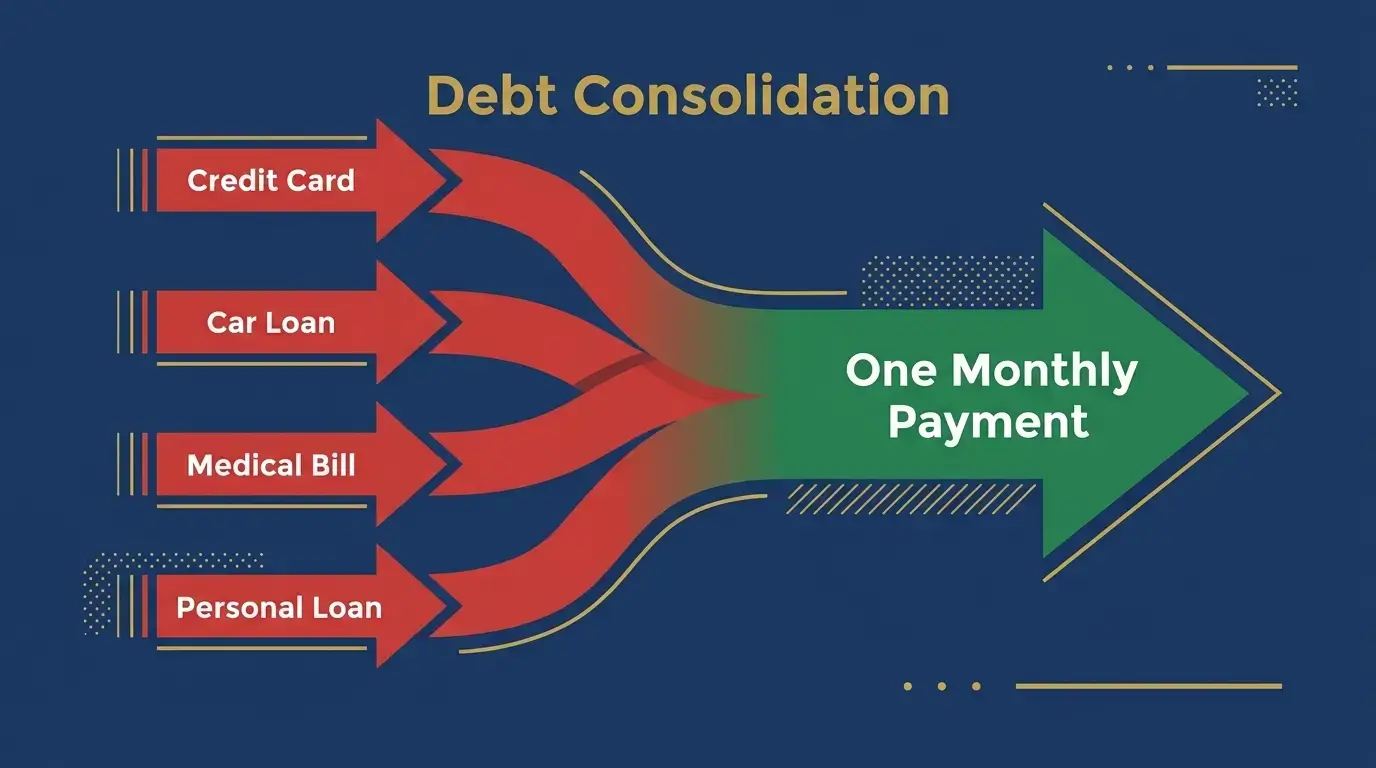

Debt consolidation is the process of combining multiple debts into a single loan or payment — ideally at a lower interest rate than you’re currently paying. Instead of managing five different minimum payments to five different creditors, you make one payment to one lender.

The goal is to simplify your debt management and — when done correctly — reduce the total interest you pay over time, potentially saving you thousands of dollars.

Debt consolidation is not debt elimination. You still owe the same amount — you’re simply restructuring how you pay it back. According to the Consumer Financial Protection Bureau, consolidation can be a smart financial tool when used correctly, but it requires careful consideration of the terms and your spending habits.

How Does Debt Consolidation Work?

The basic mechanics are straightforward:

- You apply for a new loan or credit product (a consolidation loan, balance transfer card, or home equity loan).

- You use the funds from the new loan to pay off all your existing debts.

- You now have a single debt — the consolidation loan — with one monthly payment, one interest rate, and one due date.

- You make consistent monthly payments until the consolidated debt is fully paid off.

The key to success: the new consolidated loan must have a lower interest rate than your existing debts. If it doesn’t, consolidation may cost you more in the long run.

Types of Debt Consolidation

1. Personal Debt Consolidation Loan

A personal loan from a bank, credit union, or online lender that you use to pay off multiple debts. Personal consolidation loans typically offer fixed interest rates ranging from 6% to 36%, depending on your credit score.

- Best for: People with good credit (700+) who qualify for rates below their current debt interest rates

- Loan amounts: $1,000 to $50,000 typically

- Terms: 2 to 7 years

- Secured or unsecured: Usually unsecured (no collateral required)

2. Balance Transfer Credit Card

A credit card that offers a 0% introductory APR for a promotional period (typically 12 to 21 months). You transfer your existing high-interest credit card balances to the new card and pay them off during the 0% period.

- Best for: People with good credit who can pay off the balance within the promotional period

- Typical 0% period: 12 to 21 months

- Balance transfer fee: Usually 3% to 5% of transferred amount

- After promotional period: Standard APR applies (often 20%+)

3. Home Equity Loan or HELOC

If you own a home, you can borrow against your home equity to consolidate debt. These loans offer very low interest rates (often 6% to 9%) because your home serves as collateral.

- Best for: Homeowners with significant equity and large amounts of high-interest debt

- Interest rates: Typically much lower than personal loans or credit cards

- Major risk: Your home is collateral — failure to repay could result in foreclosure

4. Debt Management Plan (DMP)

A structured repayment plan arranged through a nonprofit credit counseling agency. The agency negotiates with your creditors to reduce interest rates and consolidates your payments into one monthly amount that you pay to the agency.

- Best for: People with significant credit card debt who don’t qualify for a good consolidation loan

- Typical duration: 3 to 5 years

- Fees: Low or none through nonprofit agencies

- Credit impact: Minimal negative impact, often positive long-term

5. Student Loan Consolidation

Federal student loans can be consolidated through the U.S. Department of Education’s Direct Consolidation Loan program. This combines multiple federal loans into one, but the interest rate is the weighted average of your existing loans — so it doesn’t necessarily save money on interest.

Debt Consolidation: Pros and Cons

| ✅ Pros | ❌ Cons |

|---|---|

| One monthly payment instead of many | May extend your repayment period |

| Potentially lower interest rate | Upfront fees (origination, balance transfer) |

| Fixed monthly payment (predictable) | Risk of accumulating new debt on paid-off cards |

| Can lower your monthly payment | Home equity options risk your home |

| May reduce financial stress | Requires good credit for best rates |

| Can improve credit score long-term | Short-term credit score dip from hard inquiry |

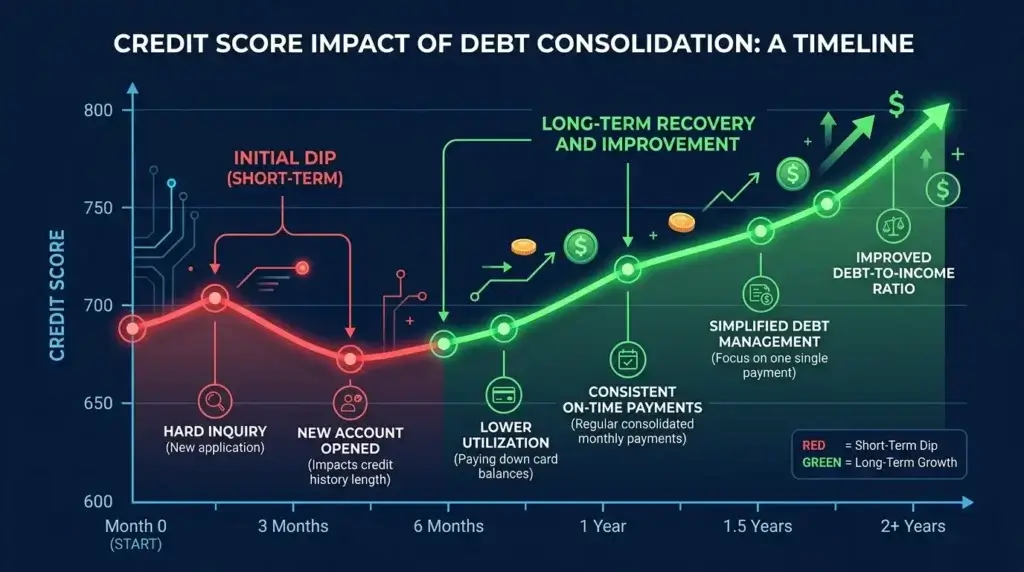

Does Debt Consolidation Hurt Your Credit Score?

The short-term and long-term effects on your credit score depend on how you consolidate:

Short-Term Impact (Usually Negative)

- Hard inquiry: Applying for a new loan or credit card causes a hard inquiry, which can temporarily lower your score by 5 to 10 points.

- New account: Opening a new account lowers the average age of your credit accounts, which can slightly reduce your score.

- Credit utilization spike: If you open a new credit card and transfer balances, your utilization on that card will be high initially.

Long-Term Impact (Usually Positive)

- Lower utilization: If you pay off credit card balances and don’t accumulate new debt, your overall credit utilization drops significantly — boosting your score.

- On-time payments: Making consistent on-time payments on your consolidation loan builds a positive payment history.

- Reduced debt burden: Lower debt levels generally improve your credit profile over time.

Key warning: The biggest credit risk with debt consolidation is paying off your credit cards and then running them back up. If you consolidate $15,000 in credit card debt and then spend $15,000 more on those cards, you now have $30,000 in debt and a wrecked credit score.

Is Debt Consolidation Worth It? How to Decide

Debt consolidation makes financial sense when:

- ✅ You can qualify for a significantly lower interest rate than your current debts

- ✅ You have multiple high-interest debts (especially credit cards at 20%+)

- ✅ You have a stable income to make consistent monthly payments

- ✅ You’re committed to not accumulating new debt on paid-off accounts

- ✅ The consolidation reduces your total interest paid, not just your monthly payment

Debt consolidation is NOT worth it when:

- ❌ The new interest rate is equal to or higher than your current rates

- ❌ You would extend repayment so long that you pay more total interest

- ❌ You plan to use the freed-up credit on paid-off cards to spend more

- ❌ The fees are too high to make the consolidation beneficial

- ❌ Your debt amount is small enough to pay off quickly with the debt snowball or avalanche method

Debt Consolidation vs Debt Settlement: What’s the Difference?

These two terms are often confused, but they are very different strategies:

| Feature | Debt Consolidation | Debt Settlement |

|---|---|---|

| What happens | Combine debts into one new loan | Negotiate to pay less than you owe |

| Credit score impact | Minor short-term dip | Severe long-term damage |

| You pay | Full amount + interest (lower rate) | Reduced amount (but fees + taxes) |

| Risk level | Low to moderate | High |

| Best for | Good credit, manageable debt | Severe hardship, near bankruptcy |

Debt settlement companies often charge high fees (15% to 25% of enrolled debt), and the forgiven debt may be taxable as income. It should only be considered as a last resort before bankruptcy.

How to Consolidate Debt: Step by Step

Step 1: List All Your Debts

Write down every debt you have: the lender, balance, interest rate, and monthly minimum payment. This gives you a clear picture of what you’re working with and helps you calculate whether consolidation makes financial sense.

Step 2: Check Your Credit Score

Your credit score determines what interest rates you’ll qualify for. Check your score for free at Credit Karma or Experian before applying for any consolidation product. Generally, you need a score of at least 670 for a personal consolidation loan with a reasonable rate.

Step 3: Calculate the Math

Use a debt consolidation calculator to compare:

- Total interest paid on current debts at current rates

- Total interest paid on the consolidated loan at the new rate

- Any fees associated with consolidation

If the consolidation saves you money in total — not just monthly — it’s worth pursuing.

Step 4: Shop and Compare Lenders

Get pre-qualified offers from multiple lenders before applying. Pre-qualification uses a soft credit inquiry (no impact on your score) and lets you compare rates without commitment. Good places to start: your current bank or credit union, LightStream, SoFi, or Marcus by Goldman Sachs.

Step 5: Apply and Execute

Once you’ve found the best offer, apply formally. If approved, use the funds to pay off your existing debts immediately. Then set up automatic payments on your new consolidation loan to ensure you never miss a payment.

Step 6: Stop Using the Paid-Off Accounts

This is the most critical step. Once you’ve paid off your credit cards through consolidation, do not run them back up. Consider removing the cards from your wallet or freezing them (literally — put them in a glass of water in the freezer) to remove the temptation. Keep the accounts open for your credit score, but don’t use them.

Frequently Asked Questions About Debt Consolidation

Will debt consolidation stop collection calls?

If your debts are current (not in collections), consolidation won’t affect collection activity since there is none. If your debts are already in collections, consolidation may not apply — you’d need to negotiate directly with collectors or consider a debt management plan.

Can I consolidate debt with bad credit?

It’s difficult but not impossible. Options for bad credit include: secured personal loans, credit unions (which often have more flexible lending criteria), debt management plans through nonprofit agencies, or asking a creditworthy co-signer to help you qualify for better rates.

How long does debt consolidation take?

A personal loan consolidation can be completed in as little as a few days. A debt management plan typically takes 3 to 5 years to complete. A balance transfer strategy depends on how quickly you can pay off the balance before the 0% promotional period ends.

Is debt consolidation the same as bankruptcy?

No — they are very different. Debt consolidation is a voluntary restructuring of your debt that you repay in full. Bankruptcy is a legal process where some or all debts may be discharged. Consolidation has a minor impact on your credit; bankruptcy has a severe impact for 7 to 10 years.

Should I close my credit cards after consolidating?

Generally no. Closing credit cards reduces your available credit, which can increase your credit utilization ratio and lower your score. Keep the accounts open but don’t use them — or use them for very small purchases that you pay off immediately each month.

The Bottom Line

Debt consolidation can be a powerful tool for simplifying your finances and reducing the interest you pay — but only if the numbers actually work in your favor. Before consolidating, do the math carefully, understand the fees involved, and have a concrete plan to avoid accumulating new debt.

The most important factor in debt consolidation success is not the loan — it’s changing the behavior that created the debt in the first place. Pair your consolidation plan with a solid budget using the 50/30/20 rule to ensure you stay debt-free going forward.

Want to explore other debt payoff strategies? Read our comparison of the debt snowball vs debt avalanche methods to find the approach that works best for your personality and financial situation. And if you’re working on rebuilding your credit while paying off debt, our guide on how to improve your credit score will help you track your progress.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Debt consolidation options vary based on individual circumstances and creditworthiness. Always consult a qualified financial advisor or nonprofit credit counselor before making debt consolidation decisions.