📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

If you’ve just started a new job and your employer mentioned a “401(k),” you might be wondering what it actually is — and whether you need to sign up. The short answer: yes, you absolutely should. A 401(k) is one of the most powerful retirement savings tools available to American workers, and not taking advantage of it could cost you hundreds of thousands of dollars over your lifetime.

In this complete guide, you’ll learn exactly what a 401(k) is, how it works, the 2026 contribution limits, how employer matching works, and how to make the most of your plan — even if you’re just starting out. If you’re already familiar with retirement accounts, you may also want to read our guide on what is a Roth IRA to understand how these two accounts work together.

What Is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to contribute a portion of their paycheck — before taxes — into a tax-advantaged investment account. The name comes from Section 401(k) of the Internal Revenue Code, which created this type of plan in 1978.

Here is the core benefit: the money you contribute to a traditional 401(k) is deducted from your paycheck before income taxes are calculated. This means you pay less in taxes today, and your money grows tax-deferred until you withdraw it in retirement.

For example, if you earn $60,000 per year and contribute $6,000 to your 401(k), you’ll only pay income taxes on $54,000 — immediately reducing your tax bill.

How Does a 401(k) Work?

Here is a step-by-step breakdown of how a 401(k) operates:

- You enroll in your employer’s 401(k) plan — usually during onboarding or open enrollment.

- You choose a contribution percentage — how much of each paycheck you want to set aside (e.g., 6% of your salary).

- Your contributions are automatically deducted from your paycheck before taxes and deposited into your 401(k) account.

- You choose how to invest your contributions from a menu of options provided by your employer (typically mutual funds, index funds, and target-date funds).

- Your money grows tax-deferred — you won’t pay taxes on investment gains until you withdraw the money in retirement.

- In retirement (age 59½+), you can withdraw your money and pay ordinary income tax on the amount withdrawn.

401(k) Contribution Limits for 2026

The IRS sets annual limits on how much you can contribute to a 401(k). For 2026, the limits are:

| Who | 2026 Contribution Limit |

|---|---|

| Employees under age 50 | $24,500 per year |

| Employees age 50–59 and 64+ | $32,500 per year (includes $8,000 catch-up) |

| Employees age 60–63 (SECURE 2.0) | $35,750 per year (super catch-up $11,250) |

These are the employee contribution limits. The total combined limit (employee + employer contributions) for 2026 is $70,000 per year. Most financial advisors recommend contributing at least enough to get the full employer match — more on that below.

What Is 401(k) Employer Matching?

Employer matching is the most valuable benefit of a 401(k) — and one of the most overlooked. Here is how it works:

Your employer agrees to match a percentage of your 401(k) contributions, up to a certain limit. For example, a common match is “50% of your contributions, up to 6% of your salary.”

Employer Match Example

Let’s say you earn $60,000 per year and your employer offers a 50% match on up to 6% of your salary:

- 6% of your salary = $3,600 per year

- You contribute $3,600

- Your employer adds 50% = $1,800

- Total invested: $5,400 per year

That $1,800 from your employer is essentially free money — a guaranteed 50% return on your investment before the market does anything. Not contributing enough to get the full employer match is one of the most common — and costly — financial mistakes.

Vesting Schedule

Employer match contributions often come with a vesting schedule — meaning you may not fully “own” your employer’s contributions until you’ve worked there for a certain number of years. Common vesting schedules include:

- Cliff vesting: You own 0% until year 3, then 100% immediately

- Graded vesting: You gradually earn ownership (e.g., 20% per year for 5 years)

- Immediate vesting: You own 100% of employer contributions right away

Always check your plan’s vesting schedule before leaving a job — you may want to stay until you’re fully vested to keep your employer’s contributions.

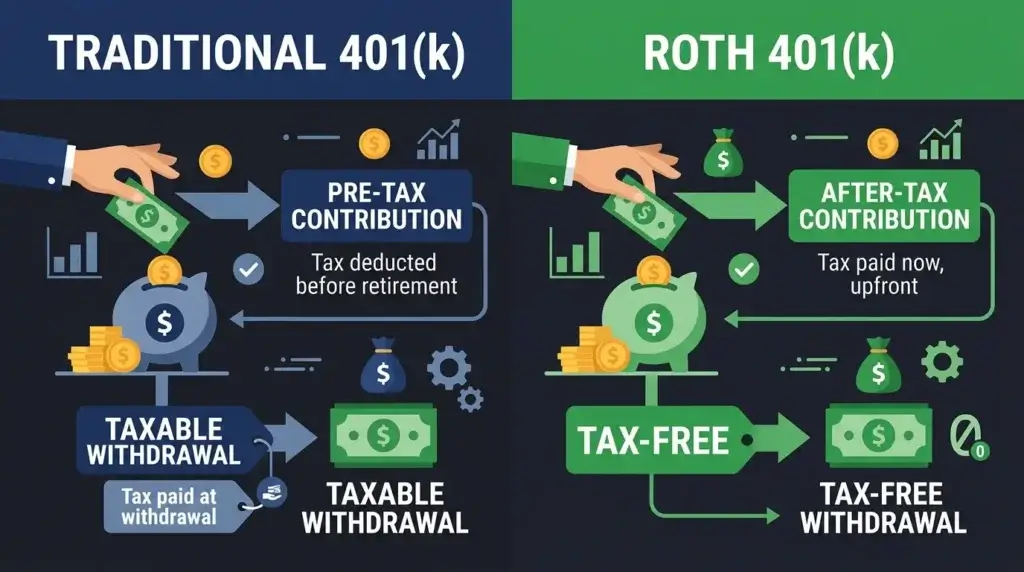

Traditional 401(k) vs Roth 401(k)

Many employers now offer both a traditional and a Roth version of the 401(k). Here is the key difference:

| Feature | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| Contributions | Pre-tax (reduces taxable income now) | After-tax (no upfront tax break) |

| Investment growth | Tax-deferred | Tax-free |

| Withdrawals in retirement | Taxed as ordinary income | Tax-free ✅ |

| Best for | Higher earners today, lower bracket in retirement | Lower earners today, higher bracket in retirement |

| Required distributions | Yes, starting at age 73 | No longer required (SECURE 2.0) |

General rule: If you expect to be in a higher tax bracket in retirement, the Roth 401(k) is usually better. If you’re in your peak earning years, the traditional 401(k) tax deduction is more valuable now. Many experts recommend contributing to both if your employer offers both options. For a deeper comparison of Roth accounts, read our guide on what is a Roth IRA.

What Can You Invest In with a 401(k)?

Unlike an IRA, a 401(k) does not give you unlimited investment choices. You can only invest in the options provided by your employer’s plan. Most plans offer:

- Target-date funds — The simplest option. Automatically adjusts risk as you approach retirement (e.g., “Target Date 2055 Fund”). Best for hands-off investors.

- Index funds — Low-cost funds that track a market index like the S&P 500. Excellent choice for most investors.

- Actively managed mutual funds — Higher fees, and most fail to outperform index funds over the long term.

- Stable value funds / money market funds — Very low risk, very low returns. Only appropriate for near-retirees.

- Company stock — Risky to have too much of your retirement savings in one company’s stock.

For most people: Choose a low-cost index fund (look for a fund with an expense ratio below 0.20%) or a target-date fund matching your expected retirement year. Avoid high-fee actively managed funds.

401(k) Withdrawal Rules

Normal Withdrawals (Age 59½+)

You can withdraw from your 401(k) without penalty starting at age 59½. Withdrawals from a traditional 401(k) are taxed as ordinary income at your current tax rate.

Early Withdrawals (Before Age 59½)

Withdrawing before age 59½ typically results in:

- A 10% early withdrawal penalty

- The amount being taxed as ordinary income

There are some exceptions — including permanent disability, certain medical expenses, and separation from service at age 55 or older — but early withdrawals should be avoided in almost all circumstances.

Required Minimum Distributions (RMDs)

For traditional 401(k)s, you must begin taking Required Minimum Distributions (RMDs) starting at age 73 (under SECURE 2.0 Act rules). The IRS calculates the minimum amount you must withdraw each year based on your account balance and life expectancy.

401(k) Loans

Many 401(k) plans allow you to borrow from your account — typically up to 50% of your vested balance or $50,000, whichever is less. While this avoids early withdrawal penalties, it comes with significant risks: you miss out on investment growth, and if you leave your job, the loan may become immediately due. Use 401(k) loans only as a last resort.

What Happens to Your 401(k) When You Change Jobs?

When you leave an employer, you have four options for your 401(k):

- Roll it over to your new employer’s 401(k) — Simple, keeps everything consolidated.

- Roll it over to an IRA — Gives you more investment options and potentially lower fees. Often the best choice.

- Leave it with your former employer — Usually fine if the plan has good investment options, but can be easy to forget.

- Cash it out — Almost always the worst option. You’ll owe income taxes plus the 10% early withdrawal penalty if you’re under 59½.

Best practice: Roll your old 401(k) into an IRA at Fidelity, Vanguard, or Schwab for maximum flexibility and investment options. This is called a direct rollover — the money transfers directly from your old 401(k) to your new IRA without triggering taxes.

How Much Should You Contribute to Your 401(k)?

Here is a simple framework that most financial advisors recommend:

- First: Contribute at least enough to get the full employer match — this is a 50–100% guaranteed return.

- Second: Max out a Roth IRA ($7,500 for 2026) for more flexibility and tax-free growth.

- Third: If you have money left over, go back and contribute more to your 401(k) up to the annual limit.

If you’re not sure how much to invest, start with just 1% of your salary. Even that small amount will grow significantly over decades. Gradually increase your contribution by 1% each year — you’ll barely notice the difference in your paycheck, but the long-term impact is enormous. Our guide on saving for retirement at 25 explains exactly why starting early matters so much.

Frequently Asked Questions About 401(k) Plans

Can I have a 401(k) and a Roth IRA at the same time?

Yes — and this is actually the recommended strategy for most people. Contribute enough to your 401(k) to get the full employer match, then max out your Roth IRA for tax-free growth. These accounts complement each other perfectly.

What if my employer doesn’t offer a 401(k)?

If your employer doesn’t offer a 401(k), you can still save for retirement tax-advantaged through an IRA (up to $7,500 for 2026). If you’re self-employed, you may be eligible for a Solo 401(k) or SEP-IRA, which have significantly higher contribution limits.

Is a 401(k) worth it even without employer matching?

Yes. The tax deferral benefit alone makes a 401(k) extremely valuable. Every dollar you contribute reduces your taxable income today, and your investments grow tax-free until retirement. For high earners especially, the tax savings can be substantial.

What happens to my 401(k) if my company goes bankrupt?

Your 401(k) is protected. By law, 401(k) assets are held separately from company assets and are not available to creditors if your employer goes bankrupt. Your retirement savings are safe.

What is the difference between a 401(k) and a pension?

A pension (defined benefit plan) pays you a guaranteed monthly income in retirement based on your salary and years of service. A 401(k) (defined contribution plan) depends on how much you contribute and how your investments perform. Pensions are rare today — most workers only have access to 401(k)-style plans.

Can I withdraw from my 401(k) to buy a house?

You can, but it’s generally not recommended. A 401(k) withdrawal before age 59½ incurs a 10% penalty plus income taxes. A better option is a first-time homebuyer withdrawal from a Roth IRA (up to $10,000 penalty-free) or a 401(k) loan if your plan allows it.

The Bottom Line

A 401(k) is one of the most powerful wealth-building tools available to American workers. The combination of pre-tax contributions, tax-deferred growth, and employer matching makes it nearly impossible to beat for retirement savings.

The single most important thing you can do right now: enroll in your employer’s 401(k) plan and contribute at least enough to get the full employer match. That free money from your employer is the highest guaranteed return you will ever find.

Once you’re maximizing your employer match, read our guide on what is a Roth IRA to understand how to combine these two accounts for maximum tax efficiency. You can also explore Roth IRA vs Traditional IRA to decide which type of additional retirement account makes the most sense for your situation.

Disclaimer: This article is for informational and educational purposes only. It does not constitute tax or financial advice. 401(k) contribution limits are based on IRS guidelines for 2026 and are subject to change. Consult a qualified financial advisor for personalized guidance.