📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

You’ve probably seen the letters “APY” on a bank account advertisement — usually next to a number like 4.50% or 5.00%. But what exactly does APY mean, and why does it matter so much for your savings?

In this complete guide, you’ll learn exactly what APY is, how it’s calculated, the difference between APY and APR, and how to use APY to make smarter decisions about where to keep your money. Understanding APY is one of the simplest ways to earn significantly more on your savings — with zero extra effort.

What Is APY?

APY stands for Annual Percentage Yield. It is the real rate of return you earn on a savings account, certificate of deposit (CD), or other interest-bearing account over the course of one year — including the effect of compound interest.

In simple terms: APY tells you exactly how much your money will grow in one year if you leave it untouched. The higher the APY, the more money you earn.

For example, if you deposit $10,000 in a high-yield savings account with a 5.00% APY, you will earn approximately $500 in interest over the course of one year — without doing anything at all.

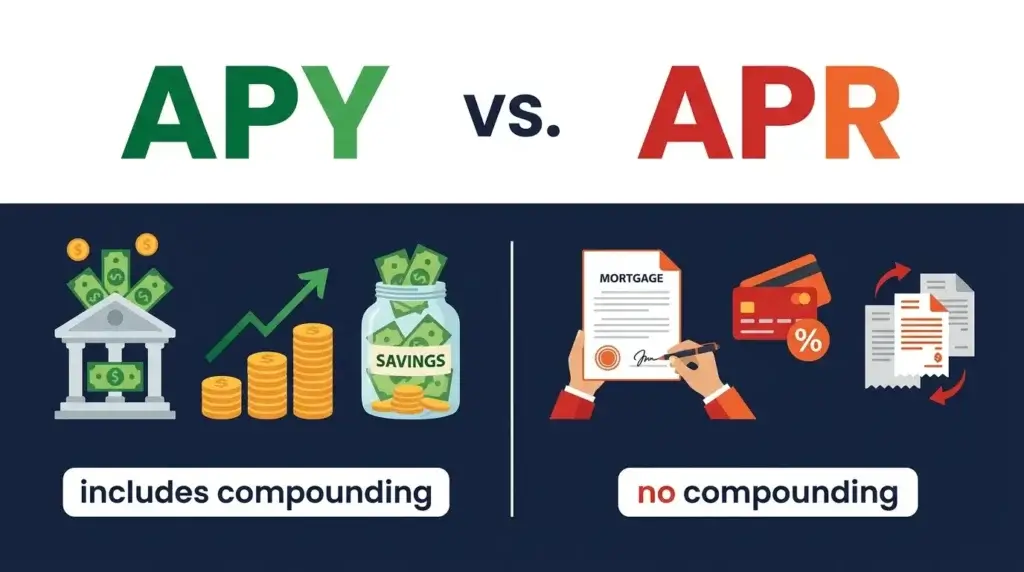

APY vs APR: What Is the Difference?

APY and APR are two terms that confuse many people, but they serve very different purposes:

| Term | Stands For | Used For | Includes Compounding? |

|---|---|---|---|

| APY | Annual Percentage Yield | Savings accounts, CDs, investments | ✅ Yes |

| APR | Annual Percentage Rate | Loans, credit cards, mortgages | ❌ No |

The key difference: APY includes compounding, which means it reflects how your interest earns more interest over time. APR does not include compounding, which is why it is used for loans where you are paying interest rather than earning it.

Rule of thumb: When you are saving money, look for a high APY. When you are borrowing money, look for a low APR.

How Is APY Calculated?

APY is calculated using this formula:

APY = (1 + r/n)^n – 1

Where:

- r = the stated interest rate (as a decimal)

- n = the number of times interest is compounded per year

Don’t worry about the math — the important thing to understand is that the more frequently interest compounds, the higher the APY compared to the stated rate.

APY Calculation Example

Let’s say a bank offers a 5% interest rate, compounded monthly (12 times per year):

- Stated rate: 5.00%

- Compounding: Monthly (12x per year)

- APY: approximately 5.12%

That extra 0.12% may seem small, but on a $50,000 balance, it means an extra $60 per year — just from compounding frequency.

How Does Compounding Work?

Compounding is what makes APY so powerful. Here is how it works:

When your bank pays you interest, that interest gets added to your balance. Then, in the next compounding period, you earn interest on your original deposit plus the interest you already earned. Over time, this snowball effect can significantly boost your earnings.

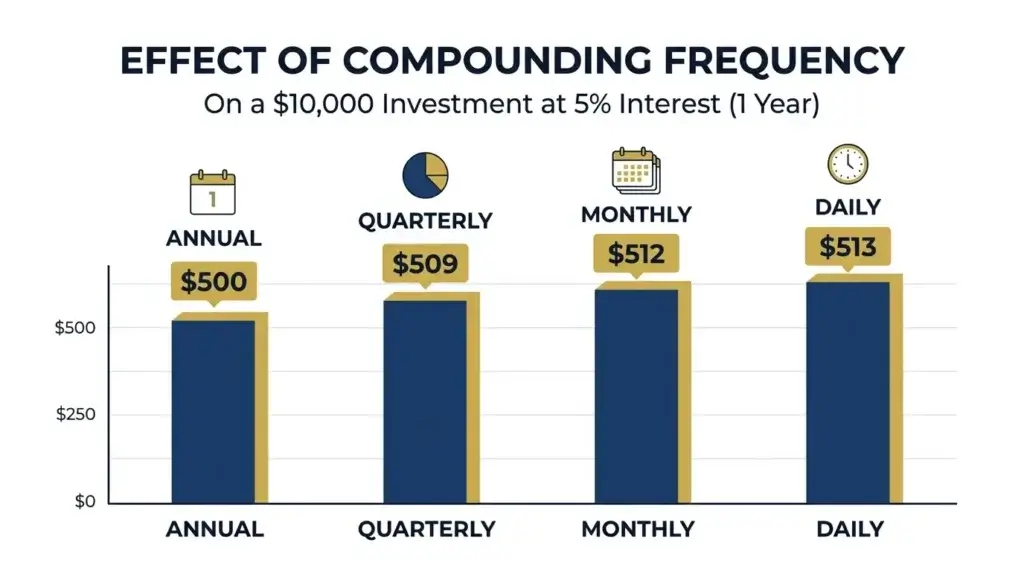

Compounding Frequency Matters

Banks can compound interest at different frequencies. Here is how compounding frequency affects your earnings on a $10,000 deposit at 5% interest rate for one year:

| Compounding Frequency | APY | Earnings on $10,000 |

|---|---|---|

| Annually (1x/year) | 5.00% | $500.00 |

| Quarterly (4x/year) | 5.09% | $509.45 |

| Monthly (12x/year) | 5.12% | $511.62 |

| Daily (365x/year) | 5.13% | $512.67 |

Most high-yield savings accounts compound interest daily — which means you earn the maximum possible return on your deposit. Always look for daily compounding when comparing savings accounts.

What Is a Good APY for a Savings Account in 2026?

APY rates fluctuate based on the Federal Reserve’s interest rate decisions. As of 2026, here is a breakdown of what you can expect:

| Account Type | Typical APY Range (2026) | Good or Bad? |

|---|---|---|

| Traditional bank savings account | 0.01% – 0.50% | ❌ Very poor |

| Credit union savings account | 0.50% – 2.00% | ⚠️ Below average |

| Online high-yield savings account | 4.00% – 5.50% | ✅ Excellent |

| Money market account | 3.50% – 5.00% | ✅ Good |

| Certificate of Deposit (CD) | 4.00% – 5.50% | ✅ Excellent (fixed term) |

Key takeaway: Traditional big banks like Chase, Bank of America, and Wells Fargo typically offer APYs of 0.01% or less on standard savings accounts. Online banks and credit unions often offer APYs that are 10 to 50 times higher. This is one of the biggest missed opportunities in personal finance.

If you are still keeping your emergency fund or savings in a traditional big bank account, you are leaving hundreds — or even thousands — of dollars on the table every year. Check our guide on the best high-yield savings accounts to find the top options available right now.

APY and the Federal Reserve: Why Rates Change

APY on savings accounts is directly influenced by the Federal Reserve’s federal funds rate. When the Fed raises interest rates, banks typically increase the APY they offer on savings accounts. When the Fed lowers rates, savings APYs usually drop.

This is why APY rates have been historically high in recent years — the Fed raised rates aggressively to combat inflation. Understanding this relationship helps you time your savings decisions and choose the right type of account for the current rate environment.

Should You Lock In a High APY with a CD?

If you believe interest rates may fall, locking in a high APY with a Certificate of Deposit (CD) can be a smart strategy. A CD offers a fixed APY for a set period (typically 6 months to 5 years), so your rate won’t drop even if the Fed cuts rates.

The tradeoff: your money is locked up for the CD term, and withdrawing early usually means paying a penalty. CDs are best for money you won’t need for a while.

How Much More Can You Earn with a High APY?

Let’s look at a real example. Suppose you have $20,000 in savings:

| Account | APY | Earnings After 1 Year | Earnings After 5 Years |

|---|---|---|---|

| Traditional bank | 0.01% | $2.00 | $10.00 |

| Average savings account | 0.50% | $100.00 | $506.00 |

| High-yield savings account | 5.00% | $1,000.00 | $5,526.00 |

That is the difference between earning $10 vs $5,526 over five years on the same $20,000 — just by choosing a higher APY account. The money is equally safe in both cases (FDIC insured up to $250,000).

How to Choose the Best APY for Your Savings

Step 1: Compare APYs Before Opening Any Account

Never accept the default APY at your current bank without shopping around. Online banks consistently offer significantly higher APYs because they have lower overhead costs than traditional brick-and-mortar banks.

Step 2: Check for Minimum Balance Requirements

Some high-APY accounts require a minimum balance to earn the advertised rate. Always read the fine print — a 5.00% APY that requires a $25,000 minimum balance may not be accessible to everyone.

Step 3: Verify FDIC or NCUA Insurance

Always make sure your savings account is insured. FDIC insurance (for banks) and NCUA insurance (for credit unions) protect your deposits up to $250,000 per depositor, per institution. This applies to both traditional and online banks.

Step 4: Look for Daily Compounding

As shown in the table above, daily compounding gives you slightly more than monthly or quarterly compounding. Most online high-yield savings accounts compound daily — this is another reason they outperform traditional banks.

Step 5: Watch for Introductory vs. Ongoing APY

Some banks advertise a very high “introductory” APY that drops significantly after 3 to 6 months. Always check what the ongoing APY will be after the promotional period ends.

APY on Different Types of Accounts

High-Yield Savings Accounts

High-yield savings accounts (HYSAs) are the most popular way to earn a high APY while keeping your money accessible. They work exactly like regular savings accounts, but the APY is dramatically higher. Most are offered by online banks. Learn more in our guide on the best online banks in the USA.

Money Market Accounts

Money market accounts typically offer APYs similar to high-yield savings accounts, but they often come with check-writing privileges and debit card access. They may have higher minimum balance requirements.

Certificates of Deposit (CDs)

CDs offer a fixed APY for a specific term. They are ideal if you want to lock in a high rate and don’t need immediate access to your funds. The APY on CDs is often slightly higher than HYSAs because you are committing to leave your money untouched.

Checking Accounts

Most traditional checking accounts pay little to no APY (0.01% or less). However, some online banks now offer high-yield checking accounts with APYs of 2% to 4%, making them worth considering for your everyday banking needs.

Frequently Asked Questions About APY

Is APY the same as interest rate?

No. The interest rate (also called the “nominal rate”) is the base rate before compounding. APY includes the effect of compounding, so it is always slightly higher than or equal to the stated interest rate. APY gives you the true picture of what you will earn.

Is a higher APY always better?

For savings accounts, yes — a higher APY means more money earned. However, always consider other factors: minimum balance requirements, account fees, ease of access, and whether the rate is introductory or permanent.

Does APY change over time?

For most savings accounts and money market accounts, yes — APY is variable and can change at any time based on Federal Reserve decisions and market conditions. CDs are the exception: once you open a CD, your APY is locked in for the entire term.

Is my money safe in a high-yield savings account?

Yes, as long as the account is FDIC-insured (for banks) or NCUA-insured (for credit unions). Your deposits are protected up to $250,000 per depositor, per institution — regardless of whether the bank is online or traditional.

How do I know if an APY is competitive?

Compare the APY to the national average savings rate, which is published monthly by the FDIC. If a savings account offers an APY significantly higher than the national average, it is competitive. As of 2026, any APY above 4.00% is considered excellent for a savings account.

Do I pay taxes on APY earnings?

Yes. Interest earned from savings accounts is considered taxable income by the IRS. Your bank will send you a 1099-INT form if you earn more than $10 in interest in a year. The interest is taxed at your ordinary income tax rate.

The Bottom Line

APY is one of the most important numbers in personal finance — yet most people ignore it. The difference between a 0.01% APY at a traditional bank and a 5.00% APY at an online bank can mean thousands of dollars over just a few years, with absolutely no extra risk.

The action step is simple: if your savings are currently sitting in a low-APY traditional bank account, open a high-yield savings account today. It takes about 10 minutes, and your money will start working harder for you immediately.

Ready to maximize your savings? Read our complete guide on the best online banks in the USA for 2026 and start earning more on every dollar you save. You can also explore checking vs savings accounts to understand which type of account is right for your financial goals.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. APY rates mentioned are approximate and subject to change. Always verify current rates directly with financial institutions before opening an account.