📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to save for a house down payment is one of the most searched home buying questions in America — and for good reason. Learning how to save for a house down payment requires a clear goal, the right savings strategy, and consistent monthly habits. Whether you are targeting 3%, 10%, or 20% down, this complete guide on how to save for a house down payment walks you through every step from calculating your goal to reaching it as fast as possible in 2026.

How Much Do You Need for a Down Payment?

Before you can save for a house down payment, you need to know your target. The amount you need depends on the home price and the loan type you plan to use. Here are the most common down payment requirements in 2026:

- 3% down — Conventional loan (first-time buyer programs like Fannie Mae HomeReady)

- 3.5% down — FHA loan (requires credit score of 580 or higher)

- 5% to 10% down — Standard conventional loan

- 20% down — Avoids private mortgage insurance (PMI), best long-term rate

- 0% down — VA loans (veterans) and USDA loans (rural areas)

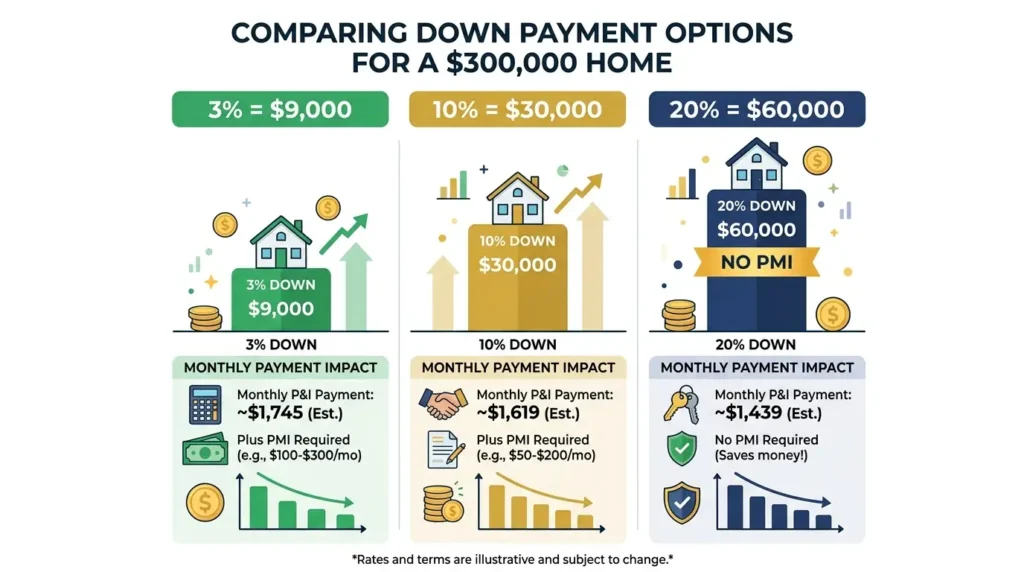

On a $300,000 home, here is what each down payment percentage means in dollars:

| Down Payment % | Amount on $300K Home | Amount on $400K Home | PMI Required? |

|---|---|---|---|

| 3% | $9,000 | $12,000 | Yes |

| 5% | $15,000 | $20,000 | Yes |

| 10% | $30,000 | $40,000 | Yes |

| 20% | $60,000 | $80,000 | No |

Private Mortgage Insurance (PMI) typically costs 0.5%–1.5% of the loan amount per year — roughly $100–$250/month on a $300,000 loan. Putting 20% down eliminates this cost entirely. However, waiting to save 20% is not always the right move — especially in a rising market where home prices may outpace your savings rate.

Step 1 — Set a Specific Down Payment Goal

The first step to save for a house down payment is turning a vague dream into a specific, measurable number. Research home prices in your target area, decide on a realistic down payment percentage, then calculate your exact savings target.

Example: You want to buy a $350,000 home with 10% down. Your down payment goal is $35,000. Add 2%–3% for closing costs ($7,000–$10,500) and your total savings target is approximately $42,000–$45,500.

Always include closing costs in your savings goal. Closing costs typically run 2%–5% of the loan amount and are paid upfront at the time of purchase — most first-time buyers are surprised by this additional expense.

Step 2 — Open a Dedicated High-Yield Savings Account

To save for a house down payment effectively, keep this money completely separate from your everyday checking account and emergency fund. A dedicated account serves two purposes: it keeps you from accidentally spending the money, and it earns meaningful interest while you save.

A high-yield savings account (HYSA) is the best place to save for a house down payment. In 2026, the top HYSAs are paying 4.5%–5.25% APY — meaning a $30,000 down payment fund earns $1,350–$1,575 per year just in interest. See our guide on the best high-yield savings accounts 2026 for the top options. To understand how APY works, read our guide on what APY means in savings accounts.

Name the account “House Down Payment” to keep your goal front and center every time you log in.

Step 3 — Calculate Your Monthly Savings Requirement

Once you know your goal and timeline, calculate the monthly savings amount you need. Divide your total down payment target by the number of months until your target purchase date.

| Down Payment Goal | 2-Year Timeline | 3-Year Timeline | 5-Year Timeline |

|---|---|---|---|

| $15,000 | $625/month | $417/month | $250/month |

| $30,000 | $1,250/month | $833/month | $500/month |

| $45,000 | $1,875/month | $1,250/month | $750/month |

| $60,000 | $2,500/month | $1,667/month | $1,000/month |

If the monthly amount feels too high, you have three options: extend your timeline, lower your down payment target, or increase your income. Most people find a combination of all three works best.

Step 4 — Build a Budget That Supports Your Goal

To save for a house down payment consistently, your monthly budget needs to explicitly include your down payment contribution as a fixed line item — not an afterthought. Two budgeting methods work especially well for this goal:

The 50/30/20 rule allocates 20% of after-tax income to savings and financial goals — your down payment contribution fits perfectly here. Read our full guide on the 50/30/20 budget rule. For even more control, zero-based budgeting assigns every dollar a specific job — including a fixed monthly amount toward your down payment. See our zero-based budgeting guide for the full method.

Step 5 — Automate Your Down Payment Savings

Automation is the most reliable way to save for a house down payment. Set up an automatic transfer from your checking account to your dedicated HYSA on every payday — before you have a chance to spend the money. Even if the amount feels small at first, the habit of consistent monthly saving is what builds the account over time.

Treat your down payment savings transfer like a bill that is due on payday. Pay it first, then live on what remains. This “pay yourself first” principle is the same strategy used to build an emergency fund — read our guide on how to build an emergency fund for the exact system.

Step 6 — Accelerate Your Savings with These Strategies

Cut Your Biggest Expenses

The fastest way to save for a house down payment is to temporarily reduce your largest monthly expenses. Housing is often the most impactful lever — if you can move somewhere cheaper, get a roommate, or negotiate rent, the savings can be redirected entirely to your down payment fund. Even $300–$500/month in reduced expenses cuts a 3-year timeline to under 2 years.

Use Every Windfall Strategically

Every tax refund, work bonus, birthday gift, or overtime payment is an opportunity to make a large one-time contribution to your house down payment fund. A single $3,000 tax refund deposited directly into your HYSA can cut 3–6 months off your savings timeline.

Increase Your Income

Saving for a house down payment is faster when you have more income coming in. Consider freelancing, a part-time job, selling unused items, or asking for a raise. An extra $500/month of income directed entirely to your down payment fund adds $6,000 per year — enough to cut a 4-year plan to under 3 years.

Reduce Subscription and Dining Spending

A temporary freeze on non-essential subscriptions, dining out, and entertainment can free up $200–$500/month. This is not forever — it is a focused sacrifice for a defined period to reach a specific goal. Set a timeline (12–18 months), cut aggressively, then restore spending once you close on your home.

How Long Does It Take to Save for a House Down Payment?

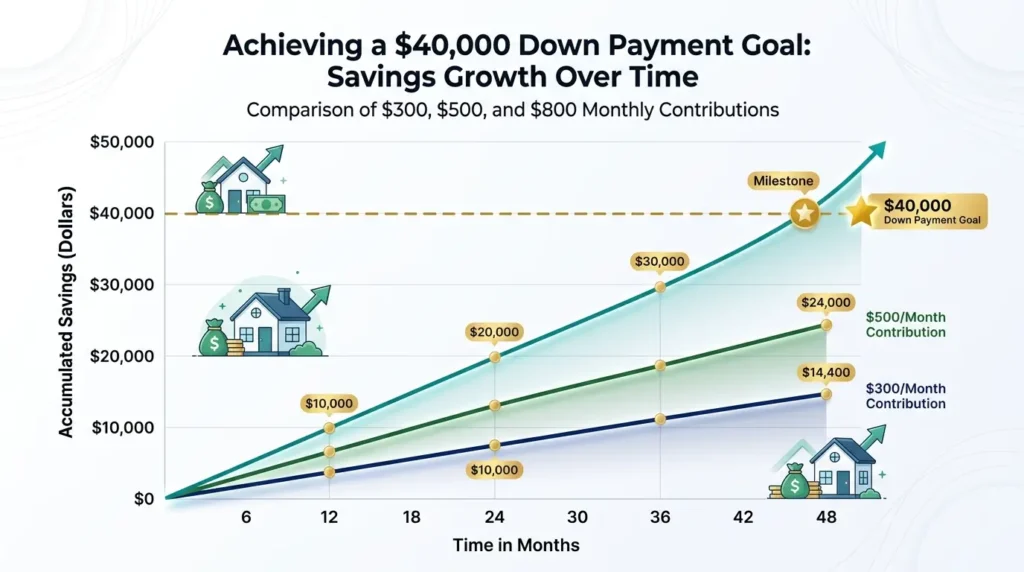

The timeline to save for a house down payment depends on your goal amount, monthly savings rate, and interest earned. Here is a realistic timeline at different savings rates, assuming a 4.75% APY high-yield savings account:

| Monthly Savings | Time to $20,000 | Time to $40,000 | Time to $60,000 |

|---|---|---|---|

| $300/month | 5.3 years | 10.5 years | 15+ years |

| $500/month | 3.1 years | 6.1 years | 9 years |

| $800/month | 1.9 years | 3.7 years | 5.4 years |

| $1,200/month | 1.3 years | 2.5 years | 3.6 years |

| $1,500/month | 1.1 years | 2.1 years | 3 years |

The interest earned in a high-yield savings account meaningfully shortens your timeline. At $800/month in a HYSA earning 4.75% APY, you reach a $40,000 down payment in approximately 3.7 years — versus 4.2 years in a traditional savings account at 0.46% APY. That is a 6-month difference from the same monthly savings amount.

Your Credit Score and the Down Payment Connection

While you save for a house down payment, simultaneously work on your credit score. Your credit score determines the mortgage interest rate you qualify for — and even a 0.5% difference in mortgage rate on a $300,000 loan means $30,000–$50,000 in extra interest paid over 30 years.

Use the months and years you spend saving for a house down payment to also build excellent credit. Pay all bills on time, keep credit card utilization below 30%, and avoid opening new accounts unnecessarily. For the full strategy, read our guide on what a credit score is and how it affects your mortgage options.

Frequently Asked Questions

How much should I save for a house down payment?

It depends on the loan type and home price. FHA loans require 3.5% down. Conventional loans start at 3%. Putting 20% down eliminates private mortgage insurance (PMI). Most first-time buyers put down between 5% and 10%. Always add 2%–5% of the purchase price for closing costs to your savings target.

Where is the best place to save for a house down payment?

A high-yield savings account (HYSA) is the best place to save for a house down payment. It is FDIC-insured, earns 4.5%–5.25% APY in 2026, and keeps your money accessible without market risk. Never put your down payment savings in the stock market — a market drop right before you buy could wipe out years of savings.

How long does it take to save for a house down payment?

At $500/month, it takes approximately 3 years to save $20,000 and 6 years to save $40,000. At $1,000/month, you can save $40,000 in about 3 years. The timeline depends on your savings rate, starting balance, and the interest earned in your savings account.

Should I put 20% down or buy sooner with less?

It depends on your market and financial situation. In a rising market, buying sooner with 5%–10% down may make more financial sense than waiting years to save 20% while home prices increase. PMI adds cost but can be removed once you reach 20% equity. Run the numbers for your specific market before deciding.

Can I use a Roth IRA to save for a house down payment?

Yes — first-time home buyers can withdraw up to $10,000 in Roth IRA earnings penalty-free for a home purchase. You can also withdraw your contributions (not earnings) at any time without penalty or taxes. However, using retirement savings for a home purchase reduces your long-term compound growth and should be considered carefully.

Final Thoughts: How to Save for a House Down Payment Starts Today

Knowing how to save for a house down payment is the first step — starting is the second. Open a dedicated high-yield savings account today, set up an automatic transfer for whatever amount fits your current budget, and increase it every time your income grows or an expense disappears. The key to how to save for a house down payment successfully is treating it like a non-negotiable monthly bill rather than an optional savings goal.

Every dollar you save now brings you one step closer to the keys in your hand. Start today, stay consistent, and let time and compound interest work in your favor.