📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is a personal loan? A personal loan is a fixed amount of money you borrow from a bank, credit union, or online lender and repay in equal monthly installments over a set period — typically 2 to 7 years. Understanding what a personal loan is and how it works helps you decide whether it’s the right financial tool for your situation. Personal loans can be a smart, cost-effective solution for certain goals — or an expensive mistake if used incorrectly. This guide breaks down everything you need to know.

What Is a Personal Loan — The Basics

A personal loan is an installment loan — meaning you receive a lump sum upfront and repay it in fixed monthly payments over a predetermined term. Unlike a credit card, which is revolving debt, a personal loan has a clear payoff date. When the term ends and all payments are made, the loan is fully repaid and closed.

Key characteristics of a personal loan:

- Loan amounts: Typically $1,000 to $100,000 depending on the lender and your credit profile

- Interest rates (APR): Usually 6%–36% in 2026, depending on your credit score and income

- Repayment terms: 12 to 84 months (1 to 7 years)

- Fixed monthly payment: The same amount every month — no surprises

- No collateral required: Most personal loans are unsecured — you don’t put up your home or car

- Funds deposited directly: Money typically arrives in your bank account within 1–5 business days

How Does a Personal Loan Work?

Here’s how a personal loan works from start to finish:

- You apply — online, at a bank, or at a credit union. You provide income, employment, and credit information.

- The lender checks your credit — a hard inquiry is placed on your credit report. Your credit score, income, and debt-to-income ratio determine your approval and interest rate.

- You receive an offer — the lender tells you the loan amount, APR, monthly payment, and total cost. You can accept or decline.

- Funds are disbursed — if you accept, the lump sum is deposited into your bank account, typically within 1–5 business days.

- You make monthly payments — fixed payments on the same date each month until the loan is fully repaid.

The total cost of a personal loan depends heavily on the interest rate and term. A $10,000 loan at 8% APR over 3 years costs approximately $11,258 total. The same loan at 20% APR costs approximately $13,340 total — nearly $2,100 more. Your credit score is the biggest factor in determining which rate you receive. To understand how to qualify for better rates, read our guide on how to improve your credit score.

Types of Personal Loans

Unsecured Personal Loan

The most common type. No collateral required — the lender approves you based on your creditworthiness alone. Higher risk for the lender means slightly higher interest rates, but you don’t risk losing an asset if you can’t repay.

Secured Personal Loan

Requires collateral — a savings account, car, or other asset — that the lender can seize if you default. Because the lender has less risk, secured loans typically offer lower interest rates. Best for borrowers with poor credit who need a lower rate.

Debt Consolidation Loan

A personal loan used specifically to pay off multiple high-interest debts — typically credit cards — and replace them with a single, lower-rate monthly payment. This is one of the most common and financially sound uses of a personal loan. For a deep dive, read our guide on debt consolidation explained.

Co-Signed Personal Loan

A loan where a second person (the co-signer) guarantees repayment if you default. Useful when your credit score isn’t strong enough to qualify alone. The co-signer takes on full responsibility for the debt if you fail to pay.

Personal Loan Interest Rates in 2026

| Credit Score | Rating | Typical APR Range (2026) |

|---|---|---|

| 720–850 | Excellent | 6%–12% |

| 690–719 | Good | 12%–18% |

| 630–689 | Fair | 18%–28% |

| 580–629 | Poor | 28%–36% |

| Below 580 | Very Poor | 36%+ or denied |

Your credit score is the single most important factor in determining your personal loan interest rate. A 100-point difference in credit score can mean the difference between 8% and 28% APR — which on a $10,000 loan over 3 years adds up to over $3,000 in extra interest.

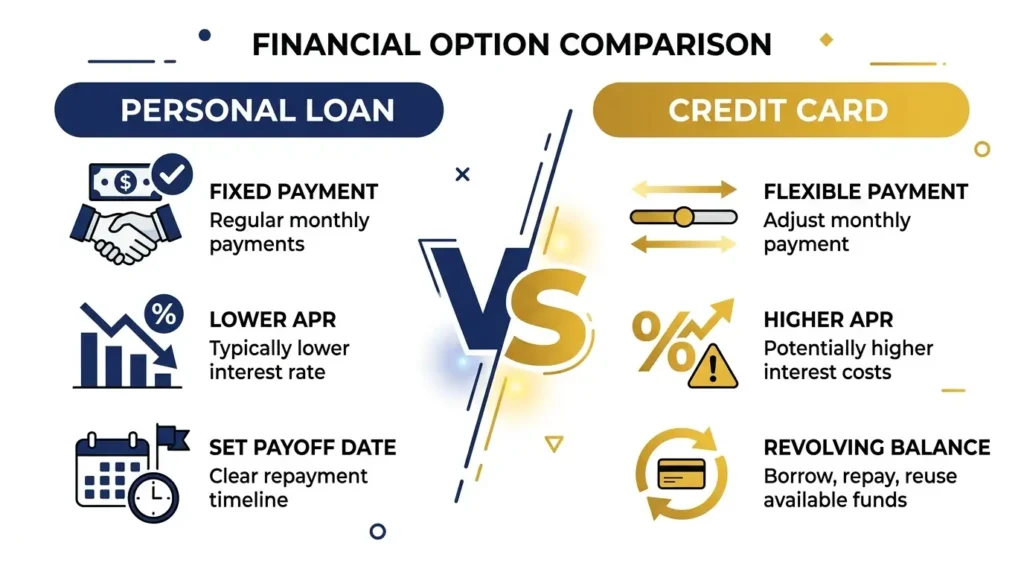

Personal Loan vs Credit Card

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Interest rate | 6%–36% (fixed) | 18%–30%+ (variable) |

| Payment structure | Fixed monthly payment | Variable minimum payment |

| Payoff date | Fixed — clear end date | Open-ended (revolving) |

| Access to funds | Lump sum upfront | Revolving line of credit |

| Best for | Large one-time expenses, debt consolidation | Everyday purchases, short-term spending |

| Credit score impact | Hard inquiry + adds installment account | Hard inquiry + adds revolving account |

A personal loan is typically better than a credit card when you need a large lump sum, want a fixed payoff date, or are consolidating high-rate credit card debt at a lower APR. A credit card is better for everyday purchases you can pay off monthly. For more on how credit cards work, read our guide on credit card vs debit card.

When Does a Personal Loan Make Sense?

A personal loan is a smart financial move in these situations:

- Debt consolidation — replacing multiple high-interest credit card balances with one lower-rate personal loan payment

- Home improvement — funding a renovation that increases home value without touching home equity

- Medical expenses — covering large unexpected medical bills at a lower rate than a credit card

- Emergency expenses — when your emergency fund isn’t sufficient and you need funds quickly

- Major purchase — financing a necessary large purchase (appliance, vehicle repair) with predictable payments

When a Personal Loan Is a Bad Idea

A personal loan is the wrong tool in these situations:

- Discretionary spending — vacations, luxury purchases, or lifestyle upgrades you can’t afford are not worth taking on debt

- When your rate is high — if your credit score puts you in the 28%–36% APR range, a personal loan is nearly as expensive as a credit card

- When you haven’t addressed the root cause — consolidating credit card debt only to run up the cards again leaves you in worse shape

- When you can’t afford the payments — missing personal loan payments damages your credit score and may result in collections

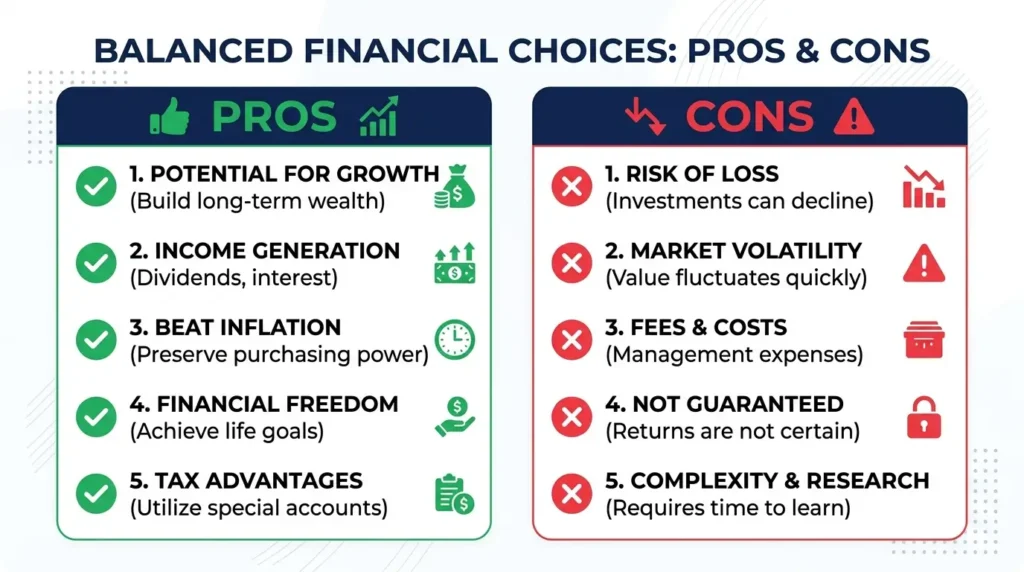

Pros and Cons of a Personal Loan

Pros

- Fixed interest rate — no surprises, same payment every month

- Lower rate than most credit cards for qualified borrowers

- Fixed payoff date — you know exactly when you’ll be debt-free

- No collateral required for most personal loans

- Can be used for almost any purpose

- Can improve your credit mix (adds an installment account)

Cons

- Interest costs money — even at 10% APR, you’re paying more than the original amount

- Origination fees — some lenders charge 1%–8% of the loan amount upfront

- Hard inquiry on your credit report temporarily lowers your score

- High rates for poor credit — borrowers below 580 may not qualify or face very high APRs

- Fixed payments can strain cash flow if your income changes

- Prepayment penalties — some lenders charge a fee if you pay off the loan early

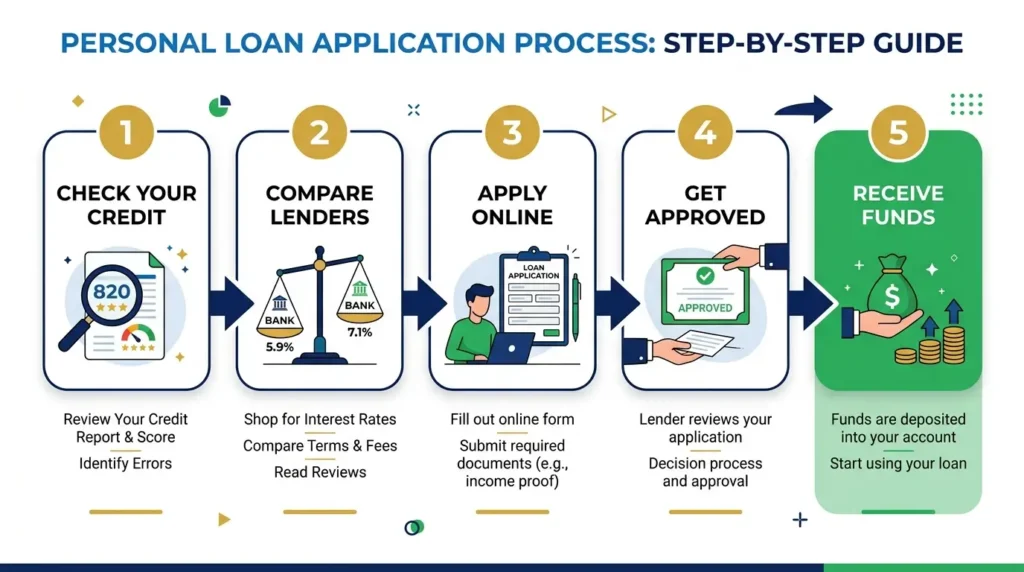

How to Apply for a Personal Loan

- Check your credit score — know where you stand before applying. Your score determines your rate. Read our guide on what a credit score is to understand what lenders see.

- Determine how much you need — borrow only what you need. More debt = more interest cost.

- Compare lenders — check rates from banks, credit unions, and online lenders. Many offer prequalification with a soft credit check so you can compare without hurting your score.

- Review the total cost — look at the APR (not just the interest rate), any origination fees, and the total repayment amount over the full loan term.

- Submit your application — provide income verification, employment details, and ID. Most online lenders give a decision within minutes.

- Receive your funds — typically deposited to your bank account within 1–5 business days.

Frequently Asked Questions

What is a personal loan used for?

A personal loan can be used for almost any purpose — most commonly debt consolidation, home improvement, medical expenses, emergency costs, or major purchases. Unlike a car loan or mortgage, a personal loan is not tied to a specific asset and can be used flexibly.

What credit score do I need for a personal loan?

Most lenders prefer a credit score of 670 or higher for competitive rates. Borrowers with scores of 720+ typically qualify for the best rates (6%–12% APR). Borrowers with scores below 580 may struggle to qualify or face very high rates. Improving your credit score before applying can save thousands in interest.

Does a personal loan hurt your credit score?

Applying for a personal loan causes a hard inquiry, which may temporarily lower your score by 5–10 points. However, making on-time payments on a personal loan actually helps your score over time by adding a positive payment history and improving your credit mix. The long-term impact is typically positive if you manage the loan responsibly.

How long does it take to get a personal loan?

Online lenders can approve and fund a personal loan within 1–3 business days. Traditional banks and credit unions may take 3–7 business days. The speed depends on how quickly you can provide required documentation and the lender’s internal processing time.

Is a personal loan better than a credit card for debt consolidation?

Often yes — if you qualify for a rate lower than your credit cards. A personal loan gives you a fixed rate, fixed monthly payment, and a clear payoff date. This structure is more disciplined than minimum credit card payments and can save significant money in interest. Read our full guide on debt consolidation for more detail.

Final Thoughts: Is a Personal Loan Right for You?

Now that you understand what a personal loan is and how it works, the question is whether it makes sense for your specific situation. A personal loan is a powerful tool when used strategically — particularly for debt consolidation or covering large necessary expenses at a lower rate than a credit card. But it adds debt, costs money in interest, and requires disciplined repayment.

Before taking out a personal loan, make sure you understand the total cost, have a clear repayment plan, and have addressed any underlying spending habits that led to the need for the loan. If overspending is the root issue, read our guide on how to stop living paycheck to paycheck first. And if you’re consolidating debt, our guide on debt consolidation explained gives you the complete strategy.