📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

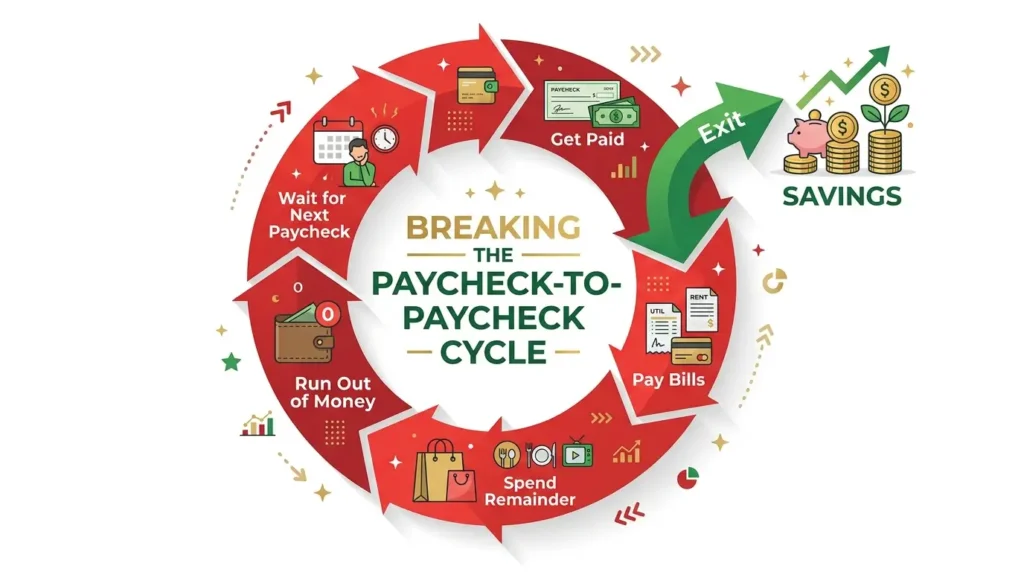

If you feel like your money disappears the moment it hits your bank account, you’re not alone. Learning how to stop living paycheck to paycheck is one of the most searched financial topics in America — and for good reason. Nearly 4 in 10 Americans couldn’t cover a $400 emergency without borrowing money. But the paycheck-to-paycheck cycle is not a life sentence. With the right steps, you can break it — regardless of your income.

Why Are You Living Paycheck to Paycheck?

Before you can fix the problem, you need to understand it. Living paycheck to paycheck is rarely just about not earning enough — it’s often a combination of factors working against you at the same time:

- No budget — spending without a plan means money disappears to low-priority purchases

- Lifestyle inflation — expenses grow in step with every raise, leaving nothing left over

- High fixed costs — rent, car payments, or debt minimums consuming too much income

- No emergency fund — every unexpected expense goes on a credit card, adding debt

- Debt payments — minimum payments eating into your monthly cash flow

- No savings habit — saving whatever is “left over” at month-end (which is usually nothing)

The good news: every one of these causes has a solution. Here are 10 proven steps to break the cycle for good.

Step 1 — Know Your Exact Numbers

You cannot fix what you cannot see. The very first step is getting complete clarity on your financial situation. For one full week, track every dollar you spend — every coffee, every subscription, every impulse buy. Most people are shocked by what they find.

- Your exact monthly take-home income (after taxes)

- Every fixed expense: rent, car, insurance, subscriptions, loan payments

- Every variable expense: groceries, gas, dining out, entertainment, clothing

- Your current savings balance and any debts owed

This exercise alone often reveals $200–$500/month in spending that could be redirected to savings. Awareness is the foundation of every financial turnaround.

Step 2 — Find Your Spending Leaks

Once you know your numbers, identify the leaks — recurring expenses you’ve forgotten about or accepted as normal. Common culprits include:

- Multiple streaming subscriptions ($50–$80/month combined)

- Gym memberships you rarely use ($30–$60/month)

- Food delivery apps with fees and tips ($100–$300/month)

- Premium phone plans when a basic plan would do ($30–$50/month savings)

- Unused app subscriptions and annual renewals

- Daily coffee shop visits ($60–$120/month)

You don’t have to eliminate everything — just be intentional. Cut what you don’t truly value and redirect that money toward your financial goals.

Step 3 — Separate Needs from Wants

One of the clearest frameworks for stopping the paycheck-to-paycheck cycle is learning to distinguish needs from wants.

- Needs: rent, groceries, utilities, transportation to work, insurance, minimum debt payments

- Wants: dining out, entertainment, vacations, premium brands, new gadgets, subscriptions

This doesn’t mean eliminating all wants — that’s unsustainable. It means being deliberate about them. The 50/30/20 budget rule is a great starting point: 50% to needs, 30% to wants, and 20% to savings and debt repayment.

Step 4 — Build a Budget That Actually Works

A budget is not a punishment — it’s a spending plan that tells your money where to go instead of wondering where it went. The key is picking a system that works for your lifestyle and sticking to it.

Zero-Based Budgeting

Every dollar of income gets assigned a job — bills, groceries, savings, fun. Income minus all assigned spending equals zero. Nothing is left “floating.” This is one of the most effective methods for people who tend to overspend. See our full guide on zero-based budgeting.

The 50/30/20 Rule

A simpler framework: 50% of take-home pay to needs, 30% to wants, and 20% to savings and debt. If you’re new to budgeting, this method is an easy starting point. Read our full breakdown in the 50/30/20 budget rule guide.

Step 5 — Pay Yourself First

The single biggest shift most people need to make is this: save before you spend, not after. The traditional approach — spending first and saving whatever’s left — almost always results in nothing saved. Instead, treat savings like a bill that’s due on payday.

Set up an automatic transfer from your checking account to a separate savings account on the same day you get paid. Even $50 or $100 per paycheck changes the dynamic entirely. Over time, you’ll adjust your lifestyle to whatever remains — and your savings will grow. For the best place to keep this money earning interest, check our guide on what APY means in savings accounts.

Step 6 — Cut Your Biggest Expenses First

Cutting $5 here and there feels good but rarely moves the needle. The fastest way to break the paycheck-to-paycheck cycle is to reduce your largest expenses. For most Americans, the top three are housing, transportation, and food.

- Housing: Consider getting a roommate, negotiating rent, or moving somewhere slightly cheaper. Rent should ideally be no more than 30% of gross income.

- Transportation: Refinance a high-rate auto loan, switch to a more fuel-efficient vehicle, or explore whether one car is possible for your household.

- Food: Meal planning, cooking at home, and reducing food delivery orders can cut $200–$400/month from a typical budget.

Step 7 — Tackle High-Interest Debt Aggressively

If credit card debt is draining your cash flow every month, it’s one of the biggest barriers to breaking the paycheck cycle. A $5,000 credit card balance at 24% APR costs over $100/month in interest alone — money that could be going toward savings.

- Debt Avalanche: Pay minimums on everything, throw every extra dollar at the highest-interest debt first. Saves the most money overall.

- Debt Snowball: Pay off the smallest balance first for quick wins and motivation. Then roll that payment to the next debt.

If your debt feels unmanageable across multiple accounts, read our guide on debt consolidation explained — combining debts into one lower-rate payment can free up significant monthly cash flow.

Step 8 — Increase Your Income

Sometimes budgeting and cutting expenses isn’t enough — especially if your income is genuinely too low to cover essentials and save. In those cases, increasing income is the most powerful lever you can pull.

- Ask for a raise: Research market salaries for your role and make a data-backed case to your employer

- Freelance or consult: Use your existing skills (writing, design, accounting, coding) to earn additional income on the side

- Sell unused items: Facebook Marketplace, eBay, and Craigslist can generate $200–$1,000 in quick cash

- Take on part-time work: Even 8–10 hours per week at $15–$20/hour adds $500–$800/month

- Upskill: Invest time learning a skill that commands higher pay within 6–12 months

Step 9 — Build an Emergency Fund

One of the biggest reasons people stay stuck in the paycheck-to-paycheck cycle is the absence of an emergency fund. Every time an unexpected expense appears — a car repair, a medical bill, a broken appliance — it goes on a credit card, adding to debt and making the cycle harder to escape.

Your goal: build a $1,000 starter emergency fund as fast as possible, then grow it to 3 months of expenses. Even $500 in a dedicated savings account changes how you respond to financial surprises. For a complete step-by-step plan, read our guide on how to build an emergency fund. Keep this money in a separate high-yield savings account — our guide on how to open a bank account online walks you through opening one in minutes.

Step 10 — Make It Automatic and Be Patient

Breaking the paycheck-to-paycheck cycle doesn’t happen overnight — it happens through consistent, automated habits over weeks and months.

- Automate savings transfers on payday so money moves before you can spend it

- Set up automatic minimum payments on all debts to avoid late fees

- Use a budgeting app to track spending in real time

- Review your budget once per week — just 10 minutes is enough

- Celebrate small milestones: first $500 saved, first debt paid off, first month with no overdraft

Progress compounds. Each small win makes the next step easier. Within 3–6 months of consistent effort, most people see a dramatic shift — from constant financial stress to real confidence.

What to Do With Your First Extra $500

| Priority | Action | Why |

|---|---|---|

| 1st | Build $1,000 emergency fund | Prevents new debt from unexpected expenses |

| 2nd | Capture 401(k) employer match | Free 50%–100% return on investment |

| 3rd | Pay off high-interest debt | Frees up monthly cash flow |

| 4th | Grow emergency fund to 3 months | Full financial safety net |

| 5th | Invest in Roth IRA or index funds | Long-term wealth building |

Once you reach Step 5, you’re no longer living paycheck to paycheck — you’re building wealth. From there, explore our guide on what a Roth IRA is as a next step in your financial journey.

Frequently Asked Questions

How long does it take to stop living paycheck to paycheck?

For most people, noticeable progress comes within 1–3 months of consistently following a budget and automating savings. Breaking the cycle completely — with an emergency fund and no high-interest debt — typically takes 6–18 months depending on income and debt levels.

Can I stop living paycheck to paycheck on a low income?

Yes, but it requires a combination of cutting expenses AND increasing income. Start by tracking spending to find leaks, build even a $500 emergency fund, and look for ways to add income — freelancing, part-time work, or selling unused items.

What is the fastest way to break the paycheck-to-paycheck cycle?

The fastest combination: (1) identify and cut your biggest spending leaks immediately, (2) automate a savings transfer on payday before you can spend, and (3) build a $1,000 emergency fund as fast as possible.

Should I pay off debt or save first?

Both. Build a $1,000 emergency fund first — without it, any unexpected expense sends you back into debt. Then aggressively pay off high-interest debt. Once done, grow your emergency fund to 3–6 months of expenses and start investing.

Is living paycheck to paycheck normal?

It’s common but not inevitable. The cycle is driven more by habits and systems than income level — which means it can be broken with the right approach, regardless of how much you earn.

Final Thoughts: Breaking the Cycle Starts Today

Knowing how to stop living paycheck to paycheck is the first step — but action is what changes everything. You don’t need a perfect plan or a higher salary to start. You need awareness, a simple budget, and one automated savings transfer set up this week.

Start with Step 1 today: write down your income and every expense. Then set up a $50 automatic transfer to savings on your next payday. That single action puts you on a different trajectory. Build from there.