📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is a money market account? A money market account is a type of bank account that combines features of both a savings account and a checking account — offering higher interest rates than a standard savings account while also providing check-writing and debit card access that savings accounts typically do not offer. Understanding what is a money market account helps you decide whether it is the right place for your emergency fund, short-term savings, or large cash reserves in 2026. This complete guide on what is a money market account explains how it works, how it compares to other accounts, and exactly when it makes sense to use one.

What Is a Money Market Account — The Simple Definition

A money market account (MMA) is an interest-bearing deposit account at a bank or credit union that is FDIC-insured up to $250,000. What distinguishes a money market account from a regular savings account is the combination of a competitive interest rate with more access options — specifically, the ability to write checks and use a debit card directly from the account.

Banks are able to offer higher rates on money market accounts because they invest the deposits in short-term, low-risk securities — government bonds, Treasury bills, and certificates of deposit. The returns from these investments allow the bank to pay a higher APY to depositors than a standard checking or savings account. All of this happens behind the scenes — from your perspective, a money market account looks and feels like a bank account with a better interest rate.

How Does a Money Market Account Work?

Here is how a money market account works in practice:

- You deposit money into the account — either online, by check, or by transfer from a linked account

- The bank pays you interest on your balance, typically at a rate between 4.00% and 5.00% APY in 2026

- Interest compounds daily or monthly and is credited to your account each month

- You can access your money via check, debit card, or electronic transfer

- Most money market accounts limit certain types of withdrawals to 6 per month — excessive withdrawals may incur fees

- Your deposits are FDIC-insured up to $250,000

To understand exactly how APY compounds over time in a money market account, read our guide on what APY means in savings accounts.

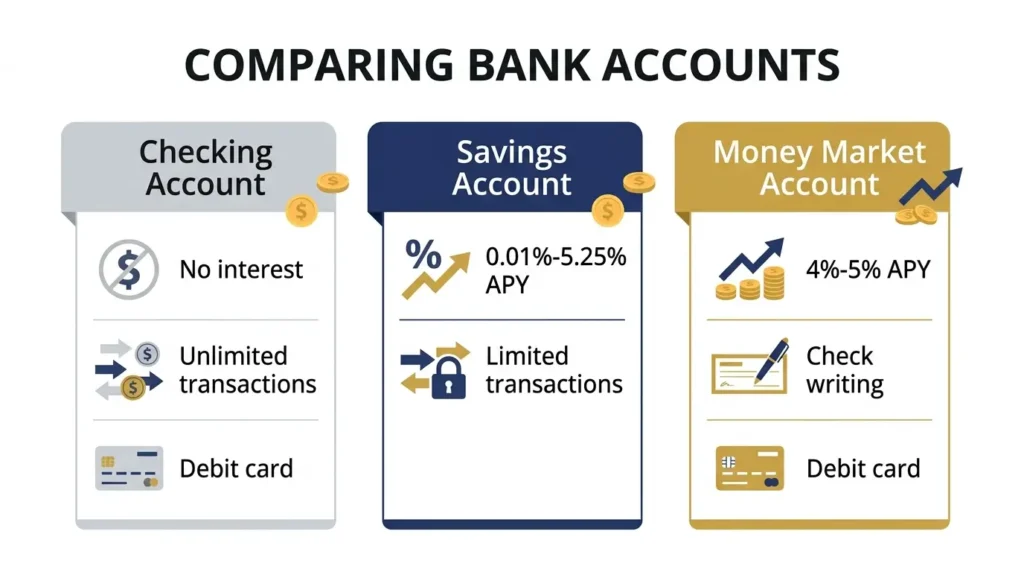

Money Market Account vs Savings Account vs Checking Account

Understanding what is a money market account is easier when you see how it sits between a checking account and a savings account:

| Feature | Checking Account | Savings Account | Money Market Account |

|---|---|---|---|

| Interest rate (APY) | 0%–0.01% | 0.01%–5.25% | 4.00%–5.00% |

| Transaction limits | Unlimited | Often limited to 6/month | Often limited to 6/month |

| Debit card access | Yes | Rarely | Often yes |

| Check writing | Yes | No | Often yes |

| Minimum balance | Usually $0 | Usually $0 | Often $1,000–$2,500 |

| FDIC insured | Yes | Yes | Yes |

| Best for | Daily spending | Emergency fund, goals | Large cash reserves, emergency fund with check access |

A money market account occupies a unique middle position — it earns competitive interest like a high-yield savings account but provides checking and debit access that most savings accounts do not. For a full comparison of savings vs checking accounts, read our guide on checking vs savings account.

Money Market Account vs High-Yield Savings Account

In 2026, high-yield savings accounts (HYSAs) and money market accounts offer very similar interest rates. The key differences:

| Feature | Money Market Account | High-Yield Savings Account |

|---|---|---|

| Typical APY (2026) | 4.00%–5.00% | 4.50%–5.25% |

| Minimum balance | Often $1,000–$2,500 | Often $0 |

| Check writing | Yes | No |

| Debit card | Often yes | Rarely |

| FDIC insured | Yes | Yes |

| Best for | Large cash reserves needing occasional check access | Emergency fund, savings goals — highest rate |

For most everyday savers in 2026, a high-yield savings account offers a slightly higher rate with no minimum balance — making it the better choice for an emergency fund. A money market account is valuable when you need occasional check-writing access to large cash reserves. See our guide on the best high-yield savings accounts 2026 for the top HYSA options.

Money Market Account Interest Rates in 2026

| Account Type | Typical APY in 2026 | Interest on $10,000 | Interest on $25,000 |

|---|---|---|---|

| Traditional bank savings | 0.01%–0.46% | $1–$46 | $2.50–$115 |

| Money market account (online bank) | 4.00%–5.00% | $400–$500 | $1,000–$1,250 |

| High-yield savings account | 4.50%–5.25% | $450–$525 | $1,125–$1,312 |

The difference between a traditional savings account at 0.46% and a money market account at 4.75% on a $25,000 balance is over $1,000 per year in additional interest — simply by moving the money to the right account. Every dollar sitting in a low-rate traditional account is leaving real money on the table.

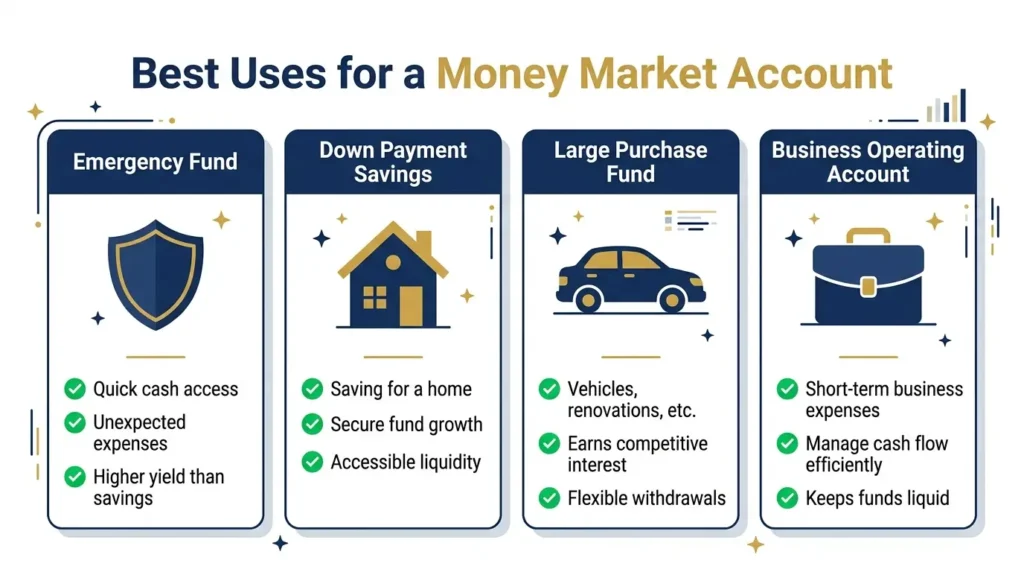

When to Use a Money Market Account

A money market account is the right choice in these specific situations:

Emergency Fund with Check Access

If you want your emergency fund to earn competitive interest but occasionally need to write a check directly from it — for a contractor, a medical bill, or a landlord — a money market account provides that flexibility. Most HYSAs require a transfer to checking first, which adds 1–3 business days. For the full emergency fund strategy, read our guide on how to build an emergency fund.

Large Short-Term Cash Reserves

If you are holding $25,000+ for a down payment, a major renovation, or a business expense within the next 6–18 months, a money market account is ideal — it earns meaningful interest while keeping the money safe, FDIC-insured, and accessible without market risk.

Business Operating Account

Small business owners often use money market accounts as operating accounts because they earn interest on idle business cash while providing check-writing ability for vendor payments and expenses.

What to Watch Out for in a Money Market Account

- Minimum balance requirements — many money market accounts require $1,000–$2,500 to open and maintain. Falling below the minimum often triggers a monthly fee.

- Transaction limits — most accounts limit certain transfers or withdrawals to 6 per month. Exceeding this may result in fees or account conversion.

- Variable rates — money market account APYs are variable and move with Federal Reserve rate decisions. The rate you open with may decrease.

- Monthly fees — always check whether the account has a monthly maintenance fee and what is required to waive it.

How to Open a Money Market Account

- Compare money market accounts at online banks, credit unions, and traditional banks — look for the highest APY with the lowest minimum balance and no monthly fee

- Go to the bank’s website and click “Open Account”

- Provide personal information — name, address, Social Security number, date of birth

- Link your existing bank account for the initial deposit

- Fund the account with at least the required minimum balance

- Set up automatic monthly transfers to keep the balance growing

For a complete walkthrough of opening any bank account online, read our guide on how to open a bank account online. And to understand how the three main account types work together in a complete banking system, read our guide on checking vs savings account.

Frequently Asked Questions

What is a money market account and how does it work?

A money market account is a bank account that pays a higher interest rate than a standard savings account while offering check-writing and often debit card access. It is FDIC-insured up to $250,000, earns 4%–5% APY at most online banks in 2026, and typically requires a minimum balance of $1,000–$2,500 to avoid fees.

Is a money market account better than a savings account?

It depends on your needs. In 2026, high-yield savings accounts often offer slightly higher APYs than money market accounts with no minimum balance requirement. A money market account is better if you need check-writing access to your funds. For most people building an emergency fund, a high-yield savings account is the simpler and often higher-rate choice.

Is a money market account safe?

Yes — money market accounts at FDIC-insured banks are protected up to $250,000 per depositor, per institution. Even if the bank fails, your deposits are guaranteed by the federal government. Always verify FDIC insurance before opening any bank account.

What is the difference between a money market account and a money market fund?

A money market account is a bank deposit account — FDIC-insured, guaranteed principal, offered at banks and credit unions. A money market fund is an investment product offered by brokerages — not FDIC-insured, invested in short-term securities, with a small risk of losing value. For safety, always use a money market account at an FDIC-insured bank for cash savings.

What is a good money market account rate in 2026?

A good money market account rate in 2026 is 4.00% APY or higher. The national average for money market accounts is significantly lower — around 0.60%–0.80%. Online banks consistently offer the highest rates, often 4.50%–5.00% APY, because they have lower overhead than traditional brick-and-mortar banks. Always compare current rates before opening an account.

Final Thoughts: What Is a Money Market Account and Is It Right for You?

What is a money market account? It is a flexible, high-yielding, FDIC-insured account that earns significantly more than a traditional savings account while offering check-writing access that most savings accounts lack. For savers holding large cash reserves — $10,000 or more — who want competitive interest and occasional check access, a money market account is an excellent choice in 2026.

For most everyday savers building an emergency fund with smaller balances, a high-yield savings account at 4.50%–5.25% APY with no minimum balance remains the simpler and often higher-rate option. The decision between the two comes down to whether you need check-writing access and can meet the minimum balance requirement. Read our guide on the best high-yield savings accounts 2026 to compare the top options side by side — and use the 50/30/20 budget rule to ensure your 20% savings allocation is going to the right account.