📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to get out of credit card debt is one of the most important financial questions millions of Americans are asking right now. If you are carrying a balance, you are not alone — and learning how to get out of credit card debt is completely achievable with the right strategy and consistent action. This step-by-step guide on how to get out of credit card debt covers every proven method available in 2026, from the debt avalanche to debt consolidation, so you can choose the approach that works best for your situation and start making real progress today.

How Much Is Your Credit Card Debt Really Costing You?

Before you can effectively get out of credit card debt, you need to understand the true cost of carrying a balance. Most people dramatically underestimate how expensive credit card interest is.

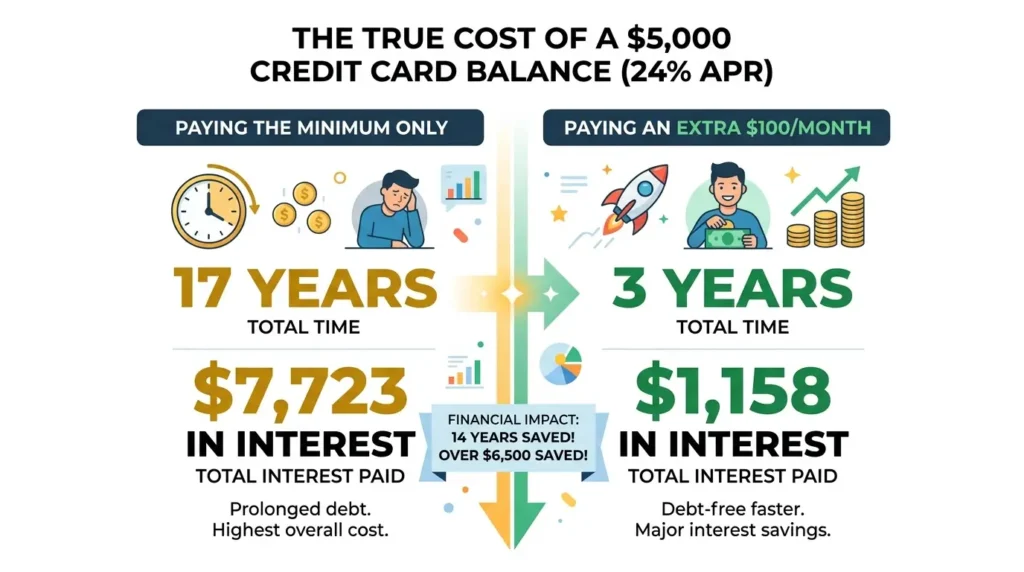

The average credit card APR in 2026 is approximately 21%–24%. Here is what that means in real dollars on a $5,000 balance:

| Payment Strategy | Monthly Payment | Time to Pay Off | Total Interest Paid |

|---|---|---|---|

| Minimum payment only (~2%) | ~$100 declining | 17+ years | $7,723 |

| Fixed $150/month | $150 | 4.5 years | $3,042 |

| Fixed $200/month | $200 | 3 years | $1,922 |

| Fixed $300/month | $300 | 1.9 years | $1,158 |

Paying only the minimum on a $5,000 credit card balance costs you $7,723 in interest over 17 years. The same $5,000 paid off aggressively at $300/month costs only $1,158 in interest over less than 2 years. That is a $6,565 difference — money that could go toward savings, investing, or your emergency fund. Understanding this reality is the motivation you need to get out of credit card debt as fast as possible.

Step 1 — List Every Credit Card Debt You Owe

The first step to get out of credit card debt is complete financial clarity. Write down every credit card you owe money on with the following information:

- Card name and issuer

- Current balance

- Interest rate (APR)

- Minimum monthly payment

- Payment due date

Most people are surprised when they add up all their balances. Seeing the total in one place is uncomfortable — but it is necessary. You cannot create a plan to get out of credit card debt without knowing exactly what you owe.

Step 2 — Stop Adding to Your Credit Card Debt

You cannot get out of credit card debt if you keep adding to it. The second step is stopping the bleeding — committing to not charging anything new to credit cards while you are paying them off. This does not mean cutting up your cards or closing accounts (which can hurt your credit score). It means making a firm decision not to add new charges while you are working to eliminate existing ones.

Switch to a debit card or cash for everyday purchases during your debt payoff period. Track every expense so you know exactly where your money is going. If overspending is the root cause of your credit card debt, read our guide on how to stop living paycheck to paycheck for a complete spending reset strategy.

Step 3 — Build a Minimum $1,000 Emergency Fund First

This step surprises many people, but it is critical: before aggressively paying down credit card debt, build a $1,000 starter emergency fund first. Without any cash cushion, every unexpected expense — a car repair, a medical bill, a broken appliance — goes right back onto a credit card. You end up running in place.

A $1,000 emergency fund breaks this cycle. It gives you the buffer to handle life’s surprises without reaching for a credit card. Read our complete guide on how to build an emergency fund for the full system.

Two Proven Strategies to Get Out of Credit Card Debt

Once you have your list and your starter emergency fund, it is time to choose a debt payoff strategy. There are two proven methods to get out of credit card debt — both work, and the best one for you depends on your personality and financial situation.

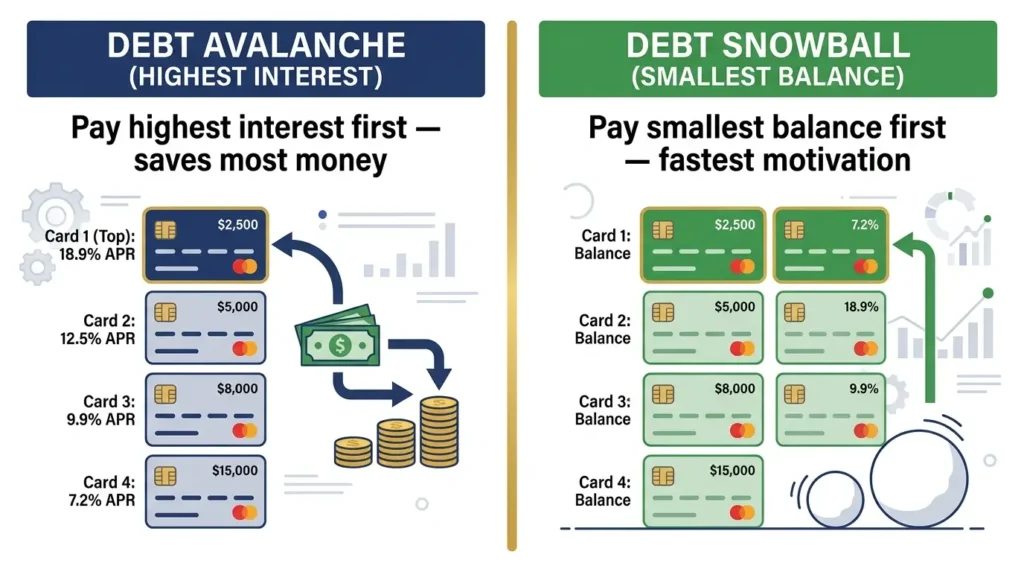

Strategy 1 — The Debt Avalanche Method

The debt avalanche is the mathematically optimal way to get out of credit card debt. Here is how it works:

- Pay the minimum payment on every credit card every month — no exceptions

- Throw every extra dollar you can find at the card with the highest interest rate

- When that card is paid off, roll its entire payment to the next highest-rate card

- Repeat until all credit card debt is eliminated

The debt avalanche saves the most money in interest over time. If you have a card at 28% APR and another at 19% APR, attacking the 28% card first minimizes the total interest you pay. This method requires patience because the highest-rate card may not be the smallest balance — but the financial savings are significant.

Strategy 2 — The Debt Snowball Method

The debt snowball is the psychologically powerful way to get out of credit card debt. Here is how it works:

- Pay the minimum payment on every credit card every month

- Throw every extra dollar at the card with the smallest balance — regardless of interest rate

- When that card is paid off, roll its payment to the next smallest balance

- Each payoff builds momentum — the snowball grows as it rolls

The debt snowball pays slightly more in interest than the avalanche method — but it produces faster early wins that keep you motivated. Research shows that many people who fail with the avalanche method succeed with the snowball because the quick wins make the process feel achievable. If motivation is your challenge, the snowball may be more effective for you personally.

Avalanche vs Snowball: Which Is Better?

| Method | Focus | Best For | Interest Saved |

|---|---|---|---|

| Debt Avalanche | Highest interest rate first | Disciplined, math-focused people | Most savings |

| Debt Snowball | Smallest balance first | People who need motivation and quick wins | Slightly less |

The best method to get out of credit card debt is the one you will actually stick with. Both methods work — the difference in total interest is often small compared to the impact of quitting midway.

Step 4 — Find Extra Money to Accelerate Payoff

The faster you throw money at your credit card debt, the less interest you pay and the sooner you get out of credit card debt. Here are proven ways to free up extra cash for debt payoff:

- Cancel subscriptions you do not actively use — streaming, gym memberships, apps ($50–$150/month)

- Cook at home instead of ordering food delivery ($100–$300/month)

- Sell unused items on Facebook Marketplace or eBay ($200–$1,000 one-time)

- Use your next tax refund entirely for debt payoff

- Take on freelance work or a part-time job and direct every dollar to your highest-rate card

- Negotiate a lower interest rate — call your card issuer and ask. Long-time customers often succeed.

A solid budget is essential for finding this extra money consistently. The 50/30/20 budget rule can help you identify exactly how much of your income should be going toward debt repayment each month.

Step 5 — Consider Debt Consolidation

If you have multiple credit cards with high interest rates, debt consolidation can be a powerful tool to get out of credit card debt faster and cheaper. Consolidation combines multiple high-rate balances into a single, lower-rate payment — reducing the interest you pay every month and simplifying your debt into one bill.

Two main consolidation options:

- Balance transfer credit card — move high-rate balances to a card with a 0% introductory APR (typically 12–21 months). Pay aggressively during the intro period to eliminate the balance before the rate rises.

- Personal loan — take out a fixed-rate personal loan at a lower APR than your credit cards and use the funds to pay off all cards at once. You then make one fixed monthly payment on the loan.

For a complete guide on how consolidation works and whether it is right for your situation, read our guide on debt consolidation explained.

Step 6 — Protect Your Credit While Paying Off Debt

Getting out of credit card debt and protecting your credit score go hand in hand. Here is what to do and what to avoid:

- Always pay at least the minimum on every card every month — a missed payment destroys your score

- Do not close paid-off cards — this increases your utilization ratio and shortens your credit history

- Keep utilization low as you pay down — every point your balance drops improves your credit score

- Do not open new credit cards while in payoff mode — hard inquiries lower your score temporarily

As you pay down credit card debt, your credit score will improve naturally. Lower balances mean lower utilization — the second biggest factor in your FICO score. Read our full guide on how to improve your credit score to maximize this benefit.

How Long Does It Take to Get Out of Credit Card Debt?

| Total Debt | Extra $100/month | Extra $200/month | Extra $400/month |

|---|---|---|---|

| $5,000 at 22% APR | 3.5 years | 2.1 years | 1.2 years |

| $10,000 at 22% APR | 6.5 years | 3.8 years | 2.1 years |

| $20,000 at 22% APR | 11+ years | 6.8 years | 3.6 years |

| $30,000 at 22% APR | 15+ years | 9.5 years | 4.9 years |

Every extra dollar you put toward credit card debt dramatically cuts the timeline. Going from $100 extra to $400 extra per month on a $10,000 balance cuts repayment from 6.5 years to 2.1 years — and saves thousands in interest. That extra $300/month is the difference between years of debt payments and financial freedom in about two years.

Frequently Asked Questions

How to get out of credit card debt fast?

The fastest way to get out of credit card debt is to stop adding new charges, use the debt avalanche method (paying the highest-rate card first), and throw every extra dollar you can find at your debt. Cut subscriptions, sell unused items, and consider a balance transfer card at 0% APR to stop interest from accumulating during payoff.

Is it better to pay off credit card debt or save?

Build a $1,000 emergency fund first, then focus aggressively on paying off credit card debt. Credit card interest rates (20%–30%) are far higher than any savings account rate. Every dollar of credit card debt you eliminate is a guaranteed 20%–30% return — no investment reliably beats that. Once high-interest debt is paid off, redirect those payments to savings and investing.

Does paying off credit card debt improve your credit score?

Yes, significantly. Paying down credit card balances reduces your credit utilization ratio — the second most important factor in your FICO score at 30%. As your balances drop, your score rises. Many people see score improvements of 20–50+ points within 30–45 days of paying down a large credit card balance.

What is the debt avalanche method?

The debt avalanche method involves paying the minimum on all credit cards while throwing every extra dollar at the card with the highest interest rate. Once that card is paid off, you roll the entire payment to the next highest-rate card. This method saves the most money in interest over time and is the mathematically optimal way to get out of credit card debt.

Should I consolidate my credit card debt?

Debt consolidation makes sense when you can qualify for a lower interest rate than what you currently pay on your credit cards. A 0% balance transfer card or a personal loan at 10%–15% APR can save significant money compared to carrying balances at 20%–28% APR. The key is to stop using the original credit cards after consolidating and commit to paying off the consolidated balance aggressively.

Final Thoughts: You Can Get Out of Credit Card Debt

Getting out of credit card debt is one of the most impactful financial decisions you can make. Every dollar you free from interest payments becomes a dollar you can direct toward savings, investing, and building the life you want. The path to get out of credit card debt is not complicated — it requires clarity about what you owe, a consistent payoff strategy, and the discipline to stick with it month after month.

Start with Step 1 today: write down every balance, interest rate, and minimum payment. Then pick your strategy — avalanche or snowball — and make your first extra payment this month. The sooner you start, the sooner you are free. Once you get out of credit card debt, redirect every payment toward building wealth through your credit score, emergency fund, and long-term investments.