📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is a balance transfer? A balance transfer is the process of moving credit card debt from one card — typically with a high interest rate — to a new card that offers a 0% introductory APR for a set period, usually 12 to 21 months. Understanding what is a balance transfer is valuable for anyone carrying credit card debt, because it can save hundreds or even thousands of dollars in interest by temporarily eliminating the interest charges that make debt so difficult to pay off. This complete guide on what is a balance transfer explains exactly how it works, what it costs, how much it can save, and when it makes sense to use one in 2026.

What Is a Balance Transfer — The Simple Definition

A balance transfer is moving an existing credit card balance from your current card to a new credit card that offers a promotional 0% APR for an introductory period. During this promotional period — typically 12 to 21 months — you pay zero interest on the transferred balance. Every dollar you pay goes directly toward reducing the principal rather than being partially consumed by interest charges.

The mechanics are simple: you apply for a balance transfer credit card, get approved, and request that the new card pay off the balance on your old card. The debt does not disappear — it moves from Card A (high APR) to Card B (0% intro APR). You then have the introductory period to pay off the transferred balance before the promotional rate expires and the regular rate applies.

How Does a Balance Transfer Work?

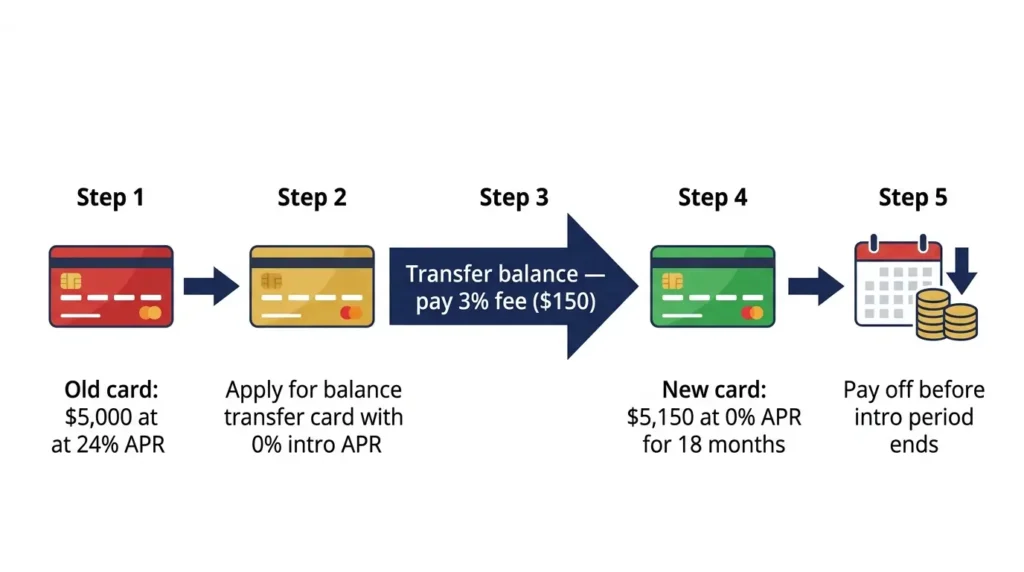

Here is the exact step-by-step process of how a balance transfer works:

- You apply for a balance transfer credit card — look for one with a 0% intro APR of 15–21 months and a low balance transfer fee (2%–5%)

- You are approved and given a credit limit — the amount you can transfer cannot exceed your new card’s credit limit

- You request the balance transfer — provide the account number and amount of the debt you want to move

- The new card pays off the old card — the process takes 5–14 business days to complete

- A balance transfer fee is charged — typically 3%–5% of the transferred amount, added to your new balance

- You pay down the transferred balance at 0% during the intro period — every payment reduces the principal

- If any balance remains when the promotional period ends — the remaining amount is charged the card’s regular APR, which may be 20%–29%

How Much Can a Balance Transfer Save You?

The potential savings from a balance transfer are significant. Here is a real comparison for a $5,000 credit card balance at 24% APR, paying $287/month:

| Scenario | Monthly Payment | Time to Pay Off | Total Interest | Transfer Fee | Total Cost |

|---|---|---|---|---|---|

| No balance transfer (24% APR) | $287 | 20 months | $1,740 | $0 | $1,740 |

| Balance transfer (0% for 18 mo, 3% fee) | $287 | 18 months | $0 | $150 | $150 |

| You Save | — | 2 months faster | $1,740 | — | $1,590 |

A balance transfer on a $5,000 debt saves approximately $1,590 in this example — from the same monthly payment, in less time. The only cost is the $150 transfer fee. At larger balances ($10,000–$20,000), the savings on a balance transfer become even more dramatic — potentially $3,000–$6,000 in interest avoided.

Balance Transfer Fees: What to Expect in 2026

Most balance transfer cards charge a one-time fee to move the debt — typically 3%–5% of the transferred amount. This fee is added to your new balance immediately. Here is what the fee costs at different debt levels:

| Balance Transferred | 3% Fee | 5% Fee | Worth It? (vs 24% APR for 18 months) |

|---|---|---|---|

| $2,000 | $60 | $100 | Yes — saves $600+ in interest |

| $5,000 | $150 | $250 | Yes — saves $1,500+ in interest |

| $10,000 | $300 | $500 | Yes — saves $3,000+ in interest |

| $15,000 | $450 | $750 | Yes — saves $4,500+ in interest |

In almost every scenario where you carry significant credit card debt, even a 5% balance transfer fee is worth paying — because the interest savings during the 0% period dramatically exceed the fee. The break-even calculation is simple: if the fee is less than the interest you would pay over the promotional period, the balance transfer saves you money.

What Credit Score Do You Need for a Balance Transfer?

Balance transfer cards with 0% introductory APRs typically require a credit score of 670 or above — Good credit or better. The best cards with 18–21 month 0% periods generally require a score of 700+. If your score is below 670, you may still qualify for some balance transfer options but with shorter promotional periods or lower credit limits.

Applying for a balance transfer card creates a hard inquiry on your credit report — a temporary decrease of 5–10 points. However, successfully reducing your credit card balance through a balance transfer improves your credit utilization, which can more than offset the hard inquiry impact over time. For more on how this works, read our guide on how to improve your credit score.

Pros and Cons of a Balance Transfer

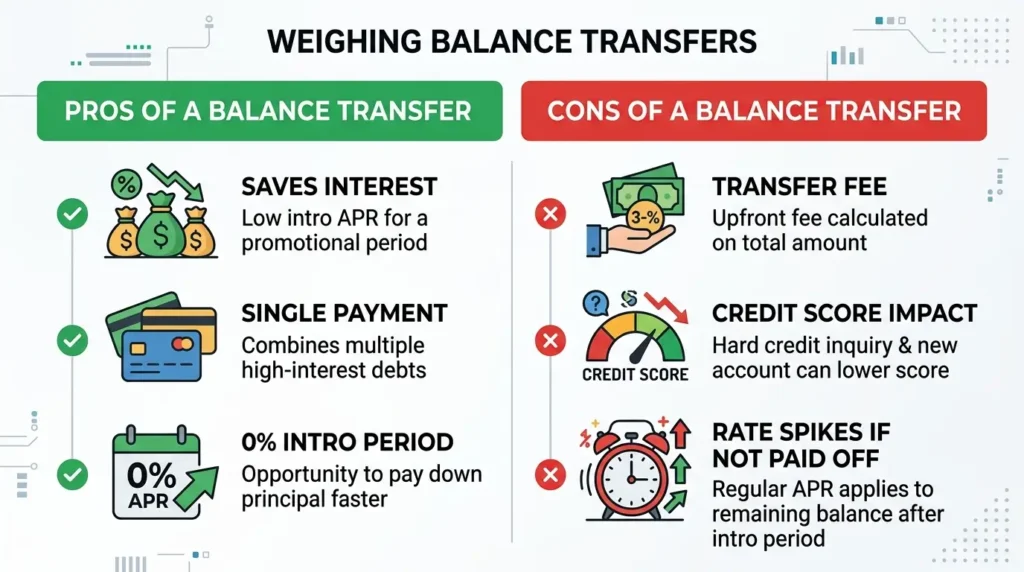

Pros of a Balance Transfer

- Saves significant money in interest — hundreds to thousands of dollars depending on balance size

- Every payment reduces principal during the 0% period — accelerates debt payoff dramatically

- Simplifies debt — consolidates one or more cards into a single payment

- Provides a clear payoff deadline — the end of the intro period creates urgency and a target date

- May improve credit utilization if you keep old cards open after transferring

Cons of a Balance Transfer

- Balance transfer fee (3%–5%) adds to the total debt immediately

- Hard inquiry temporarily lowers your credit score when you apply

- If you do not pay off the balance before the intro period ends, the remaining amount is charged the regular rate — often 24%–29% APR

- New purchases on the balance transfer card are typically not covered by the 0% rate — they accrue interest immediately

- Requires discipline — a balance transfer only helps if you stop adding to your existing card debt simultaneously

When a Balance Transfer Makes Sense

- You have $2,000 or more in high-interest credit card debt (above 18% APR)

- Your credit score is 670 or above — you can qualify for a competitive balance transfer card

- You can realistically pay off the transferred balance before the 0% period ends

- You are committed to not using the original card for new purchases during the payoff period

- The fee is less than the interest you would pay on the existing card during the same period

A balance transfer is one of several tools for eliminating credit card debt — alongside the debt avalanche and debt snowball. For the complete debt elimination strategy, read our guide on how to get out of credit card debt and our comparison of debt snowball vs debt avalanche.

When a Balance Transfer Is NOT the Right Choice

- Your credit score is below 670 — you likely will not qualify for the best cards

- You cannot pay off the transferred balance before the intro period ends — you will end up back at a high interest rate, possibly on a larger balance

- You plan to run up the original card again — this is the most common balance transfer mistake, leaving you with double the debt

- The balance is small ($500 or less) — the fee may represent a significant percentage and the interest savings are modest

Frequently Asked Questions

What is a balance transfer and how does it work?

A balance transfer is moving existing credit card debt to a new card with a 0% introductory APR, typically lasting 12–21 months. You apply for the balance transfer card, request the transfer of your existing balance, and pay a one-time fee of 3%–5%. During the 0% period, every payment reduces your principal with no interest — allowing you to pay off the debt faster and cheaper than keeping it on a high-rate card.

Is a balance transfer worth it?

Yes — in most situations where you carry significant credit card debt above 18% APR. A balance transfer is worth it when the interest savings during the 0% period exceed the transfer fee, and when you can realistically pay off the balance before the promotional period ends. On a $5,000 balance at 24% APR, a balance transfer typically saves $1,500+ in interest after the fee.

Does a balance transfer hurt your credit score?

Applying for a balance transfer card creates a hard inquiry, which may temporarily lower your score by 5–10 points. However, successfully paying down the transferred balance reduces your credit utilization — a positive factor worth 30% of your FICO score. Over time, a balance transfer that results in lower balances typically improves your credit score more than the hard inquiry hurts it.

What happens if I don’t pay off a balance transfer in time?

When the 0% introductory period ends, any remaining balance is charged the card’s regular APR — typically 20%–29%. Interest is not retroactively applied to the original balance (unless you had a deferred interest promotion, which is different from a 0% APR promotion). To avoid this, always calculate the monthly payment needed to pay off the full balance before the promotional period expires and automate that payment.

What credit score do I need for a balance transfer card?

Most balance transfer cards with 0% intro APR require a credit score of 670 or above. The best cards with the longest 0% periods (18–21 months) typically require a score of 700 or higher. If your score is below 670, work on improving it before applying, or consider alternative debt payoff strategies like a personal loan or the debt avalanche method.

Final Thoughts: A Balance Transfer Is a Tool — Use It Strategically

Now that you understand what is a balance transfer and how it works, the key question is whether it fits your specific situation. A balance transfer is not a debt solution — it is a debt acceleration tool. It gives you a window of time to pay off your debt without interest eating your payments. Used correctly, it can save thousands of dollars and get you out of debt months or years faster.

If you decide to use a balance transfer, commit to two non-negotiable rules: make the monthly payment that pays off the full balance before the intro period ends, and do not make new purchases on either the old card or the balance transfer card during the payoff period. For the full credit card debt elimination strategy alongside a balance transfer, read our guide on how to get out of credit card debt. And if a balance transfer is not available to you, read our guide on debt consolidation explained for alternative approaches.