📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to get out of debt is one of the most life-changing financial skills you can develop — because debt is not just a financial burden, it is a psychological one that affects every decision you make with money. Learning how to get out of debt requires a clear plan, consistent action, and the right strategies applied in the right order. Whether you carry credit card debt, student loans, a car loan, medical bills, or a combination of all of them, this complete step-by-step guide on how to get out of debt gives you everything you need to build your payoff plan and execute it successfully in 2026.

Why Getting Out of Debt Changes Everything

Before diving into how to get out of debt, it is worth understanding what you are actually fighting for. The average American household carries over $100,000 in total debt — mortgages, car loans, credit cards, and student loans combined. High-interest debt — particularly credit card debt at 20%–28% APR — is especially destructive because it compounds relentlessly against you.

A $10,000 credit card balance at 24% APR, paying only the minimum, takes over 25 years to pay off and costs more than $17,000 in interest alone. Getting out of debt eliminates that guaranteed negative return, frees up monthly cash flow for building wealth, and removes one of the biggest sources of financial stress in American life. Every dollar of debt you eliminate is a dollar that now works for you instead of against you.

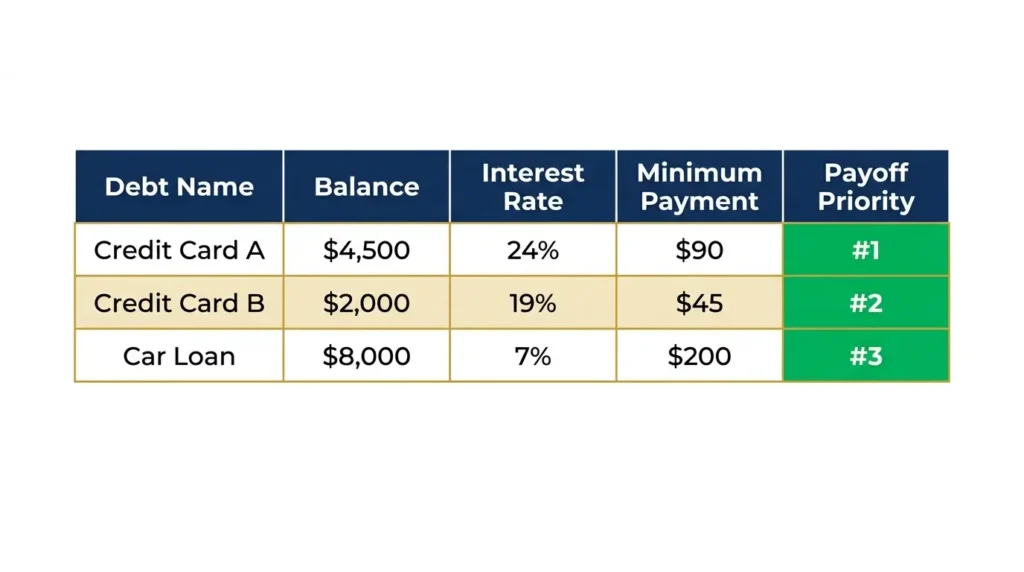

Step 1 — List Every Debt You Owe

The first step to get out of debt is total clarity — knowing exactly what you owe. Many people avoid this step because the number feels overwhelming. Do it anyway. You cannot plan a debt payoff without accurate data. For every debt you carry, write down:

- The lender name

- The current balance

- The interest rate (APR)

- The minimum monthly payment

- Whether the rate is fixed or variable

Total everything up. This is your debt number — the exact amount you are fighting to eliminate. Most people find this number both sobering and motivating. It gives the goal a shape and a size. A problem you can see clearly is a problem you can solve.

Step 2 — Stop Adding to Your Debt

You cannot get out of debt while simultaneously adding to it. Before any payoff strategy can work, you must stop the inflow. This means:

- Stop using credit cards for purchases you cannot pay off in full each month

- Do not take out new personal loans unless it is to consolidate at a lower rate

- Build a small $1,000 emergency fund first — so that unexpected expenses do not push you back to the credit card

- Cancel subscriptions and recurring charges you forgot about

The emergency fund is critical here. Most people who fail to get out of debt do so because one unexpected expense — a car repair, a medical bill — goes straight to the credit card, undoing weeks or months of progress. Even $1,000 in savings creates enough of a buffer to stop that cycle.

Step 3 — Build a Budget That Frees Up Cash for Debt Payoff

Getting out of debt requires cash — specifically, extra cash beyond your minimum payments that you can throw at your target debt every month. A budget is the tool that finds that cash. Read our guide on how to make a budget to build one from scratch.

When building your debt-payoff budget, look for cash in these categories:

- Dining out and takeout — often $200–$500/month that can be cut by 50%

- Subscriptions — streaming, apps, gym memberships — audit every automatic charge

- Grocery spending — meal planning alone saves $100–$200/month

- Entertainment — movies, events, impulse purchases

- Transportation — can you reduce driving, refinance a car loan, or carpool?

Goal: find at least $200–$400/month in extra cash beyond your minimum payments. Even $200/month extra accelerates debt payoff dramatically and saves thousands in interest.

Step 4 — Choose Your Payoff Method

With your debt list and budget in place, choose one of two proven methods to get out of debt:

The Debt Avalanche (Mathematically Optimal)

Pay minimums on all debts. Direct every extra dollar to the debt with the highest interest rate. When that debt is gone, roll the full payment to the next highest rate. The avalanche saves the most money in total interest — often hundreds to thousands of dollars compared to minimum payments.

The Debt Snowball (Psychologically Powerful)

Pay minimums on all debts. Direct every extra dollar to the debt with the smallest balance. Quick wins build momentum and motivation. When the smallest debt is gone, roll the full payment to the next smallest. Research shows the snowball helps more people actually complete their debt payoff. Read our full comparison in our guide on debt snowball vs debt avalanche.

| Method | Order | Best For | Interest Saved |

|---|---|---|---|

| Debt Avalanche | Highest rate first | Disciplined, math-motivated | Maximum savings |

| Debt Snowball | Smallest balance first | Motivation-driven, needs wins | Slightly less (but still significant) |

| Hybrid | One small win, then avalanche | Most people | Near-maximum with motivation boost |

Step 5 — Consider Tools That Accelerate Getting Out of Debt

Balance Transfer Cards

If you have credit card debt and a credit score of 670+, a 0% APR balance transfer card can eliminate interest for 12–21 months — meaning every payment goes directly to principal. Read our guide on what is a balance transfer to see if this tool fits your situation.

Debt Consolidation Loan

A personal loan at a lower rate than your current debt can consolidate multiple high-rate balances into one single payment at a lower rate. This simplifies your payoff and reduces total interest. Read our guide on debt consolidation explained to understand when it makes sense.

Increase Your Income

The fastest way to get out of debt is to increase the amount you can throw at it each month. A side hustle generating $400–$800/month directed entirely at your highest-rate debt can cut a 4-year payoff timeline in half. Options: freelancing, rideshare driving, tutoring, overtime, selling unused items.

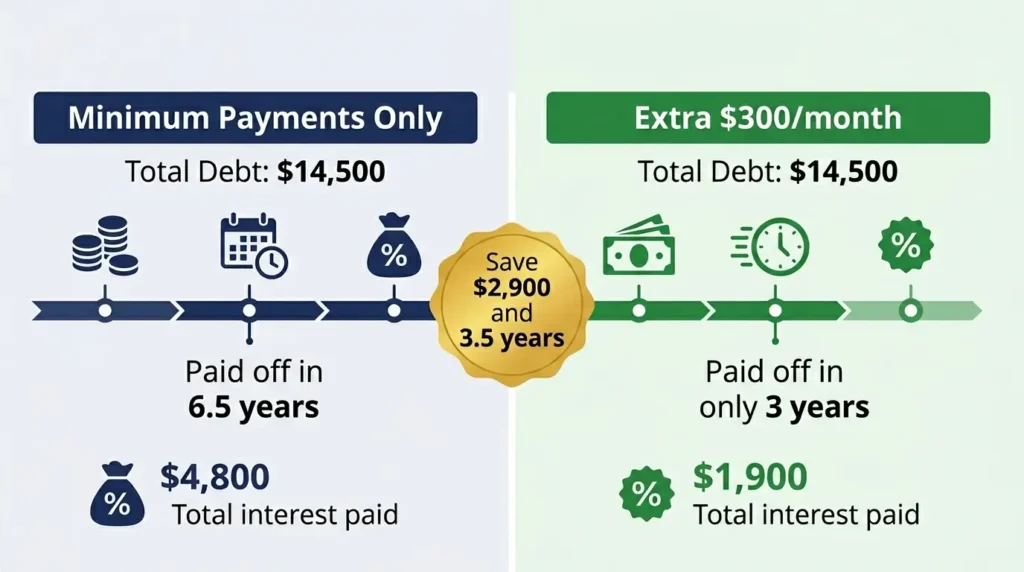

How Long Will It Take to Get Out of Debt?

| Total Debt | Extra Payment/Month | Approximate Payoff Time | Interest Saved vs Minimums |

|---|---|---|---|

| $10,000 at 20% APR | $200/month extra | ~3.5 years | ~$6,000 |

| $20,000 at 20% APR | $300/month extra | ~5 years | ~$10,000 |

| $30,000 at 18% APR | $400/month extra | ~5.5 years | ~$12,000 |

| $50,000 mixed debt | $600/month extra | ~6–7 years | ~$15,000+ |

These timelines assume consistent extra payments and no new debt added. The actual timeline varies based on your specific interest rates, minimum payments, and how aggressively you can increase the extra payment over time as other debts are paid off and their payments roll forward.

What to Do After You Get Out of Debt

Getting out of debt is the beginning of building wealth — not the finish line. Once your last debt is paid, immediately redirect every former debt payment to wealth building. Do not let lifestyle inflation absorb the cash flow you just freed up. The sequence:

- Complete your full 3–6 month emergency fund if not yet done

- Max your Roth IRA ($7,500/year in 2026)

- Increase your 401(k) contribution to the full $24,500 limit

- Open a taxable brokerage account for additional investing

- Track your net worth quarterly — watch it grow now that debt is gone

Frequently Asked Questions

What is the fastest way to get out of debt?

The fastest way to get out of debt combines three actions: maximize the extra payment you make each month (cut expenses and increase income), use the debt avalanche to eliminate your highest-rate debt first, and consider a balance transfer or debt consolidation loan to reduce your interest rate. All three together can cut a 5–7 year payoff down to 2–3 years on the same total debt.

How do I get out of debt on a low income?

On a low income, start small: cut every non-essential expense and put even $50–$100 extra per month toward your smallest debt. Build a $500–$1,000 emergency fund first to prevent debt cycling. Look for income increases — overtime, a small side hustle, or selling unused items. Every extra dollar you can direct to debt payoff accelerates the timeline significantly, even at small amounts.

Should I pay off debt or save first?

Save a $1,000 starter emergency fund first — before aggressively paying off debt. This prevents one unexpected expense from sending you back to the credit card and undoing your progress. After the $1,000 is in place, pay off all high-interest debt (above 7% APR) before building a larger emergency fund. Always capture your full employer 401(k) match simultaneously — it is a guaranteed return that beats even high-rate debt payoff.

Is debt consolidation a good way to get out of debt?

Debt consolidation can accelerate getting out of debt if it reduces your interest rate — combining multiple high-rate balances into one lower-rate personal loan or balance transfer card. It works best when you are disciplined enough not to run up new balances on the old cards. Consolidation is a tool, not a solution — you still need to pay off the consolidated balance aggressively.

How do I stay motivated while paying off debt?

To stay motivated while getting out of debt: track your progress visually (a debt payoff chart where you color in each $1,000 milestone), celebrate each debt elimination with a small non-financial reward, calculate and display the monthly cash flow you will gain when debt-free, and connect the goal to a specific life change it will enable — travel, homeownership, career flexibility. Joining an online debt-free community also provides powerful accountability.

Final Thoughts: Getting Out of Debt Is the Most Powerful Financial Move You Can Make

Learning how to get out of debt and following through on the plan is the single most transformative financial action most Americans can take. It eliminates guaranteed negative returns, frees up hundreds of dollars per month in cash flow, removes financial stress, and creates the foundation for building lasting wealth. Getting out of debt is not a one-time event — it is a daily commitment to a plan that compounds in your favor with every payment.

Start today: list your debts, build your budget, choose your method, and make your first extra payment this week. The debt-free life is not just a financial milestone — it is a feeling of freedom and control that changes how you live. For the complete picture of where debt payoff fits in your broader financial life, read our guide on how to stop living paycheck to paycheck.