📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to make a budget is the most fundamental personal finance skill you can learn — and it is far simpler than most people think. Learning how to make a budget does not require a spreadsheet degree, a financial advisor, or hours of preparation. In fact, how to make a budget can be broken down into six clear steps that anyone can follow in under an hour. This complete guide on how to make a budget walks you through every step, from calculating your income to choosing the right method and tracking your spending every month in 2026.

Why You Need to Know How to Make a Budget

A budget is not a restriction — it is a plan that tells your money where to go instead of wondering where it went. People who know how to make a budget and use one consistently spend 15–20% less than those who do not track their spending. They save more, carry less debt, and build wealth faster — not because they earn more, but because they are intentional about every dollar.

If you are living paycheck to paycheck, making a budget is the single most impactful first step. Read our guide on how to stop living paycheck to paycheck alongside this one for a complete financial reset.

Step 1 — Calculate Your Monthly Take-Home Income

The first step to make a budget is knowing exactly how much money you bring home each month. Use your net income — the amount deposited into your bank account after taxes, health insurance, and 401(k) contributions are deducted. Do not use your gross salary.

- Salaried employees: divide your annual net pay by 12

- Hourly workers: multiply your average hours per week by your hourly rate, then multiply by 4.33

- Freelancers or variable income: use your average income from the last 3 months as your baseline

- Include all income sources: side gigs, rental income, alimony, government benefits

This number is the foundation of your entire budget. Every other number in your budget must be smaller than this one.

Step 2 — List All Your Monthly Expenses

The second step to make a budget is capturing every expense — both fixed and variable. Go through your last 2–3 months of bank and credit card statements to make sure you catch everything, including annual expenses you may have forgotten.

Fixed Expenses

Fixed expenses are the same amount every month and must be paid regardless of circumstances:

- Rent or mortgage payment

- Car payment and auto insurance

- Health insurance premium

- Phone bill

- Internet service

- Minimum debt payments (student loans, credit cards)

- Streaming subscriptions and recurring memberships

Variable Expenses

Variable expenses change month to month — but they are predictable enough to budget for:

- Groceries

- Gas and transportation

- Dining out and food delivery

- Clothing and personal care

- Entertainment and hobbies

- Medical copays and prescriptions

- Home or car maintenance

Periodic Expenses

These are expenses that do not occur every month but are predictable and should be in your budget. Divide the annual amount by 12 and include it as a monthly line item:

- Car registration and annual insurance renewals

- Holiday and birthday gifts

- Vacations

- Annual software subscriptions

- Tax payments if self-employed

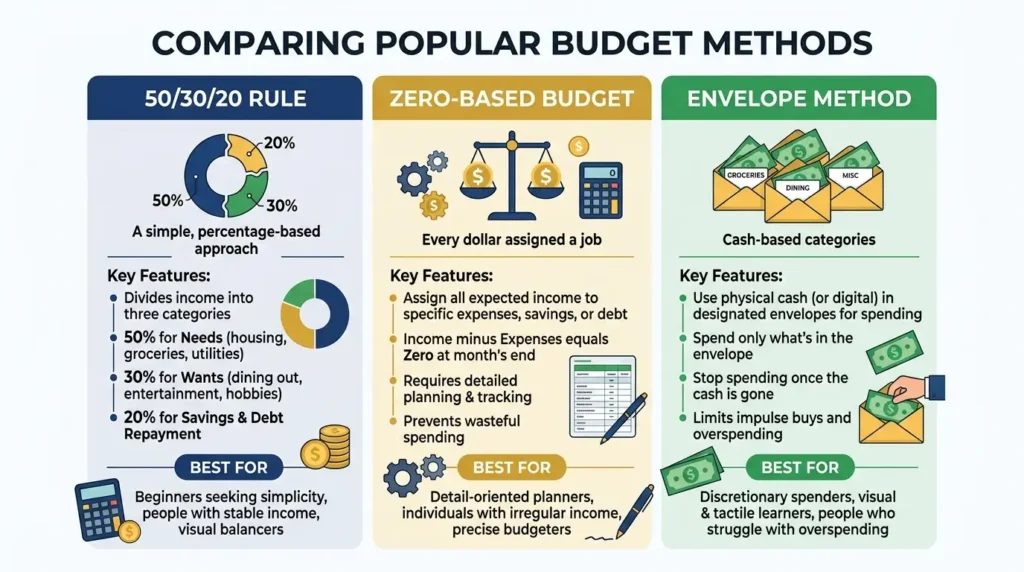

Step 3 — Choose Your Budgeting Method

The right budgeting method when you make a budget is the one you will actually use. Here are the three most popular methods for beginners:

The 50/30/20 Rule

Allocate 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. This is the easiest method to make a budget with — it requires no detailed tracking and works well for people who are new to budgeting. Read our full guide on the 50/30/20 budget rule for the complete breakdown.

Zero-Based Budgeting

Every dollar of income is assigned a specific job — bills, groceries, savings, fun. Income minus all assigned spending equals zero. Nothing is left unallocated. This method provides the most control and is especially effective for people who have struggled with overspending. Read our zero-based budgeting guide for the full system.

The Envelope Method

Allocate a fixed amount of cash to each spending category in a physical envelope. When the envelope is empty, spending in that category stops for the month. This method works extremely well for people who overspend on variable categories like groceries and dining out, because the physical cash creates a tangible limit.

Step 4 — Set Savings as a Non-Negotiable Line Item

When you make a budget, savings should appear as a fixed expense — not as whatever is left over after spending. Treat your savings contribution the same way you treat your rent payment: it is due on payday and non-negotiable.

List these savings categories in your budget before discretionary spending:

- Emergency fund contribution — until you reach 3–6 months of expenses. Read our guide on how to build an emergency fund.

- Retirement contribution — 401(k) and Roth IRA monthly amounts

- Specific savings goals — house down payment, car, vacation

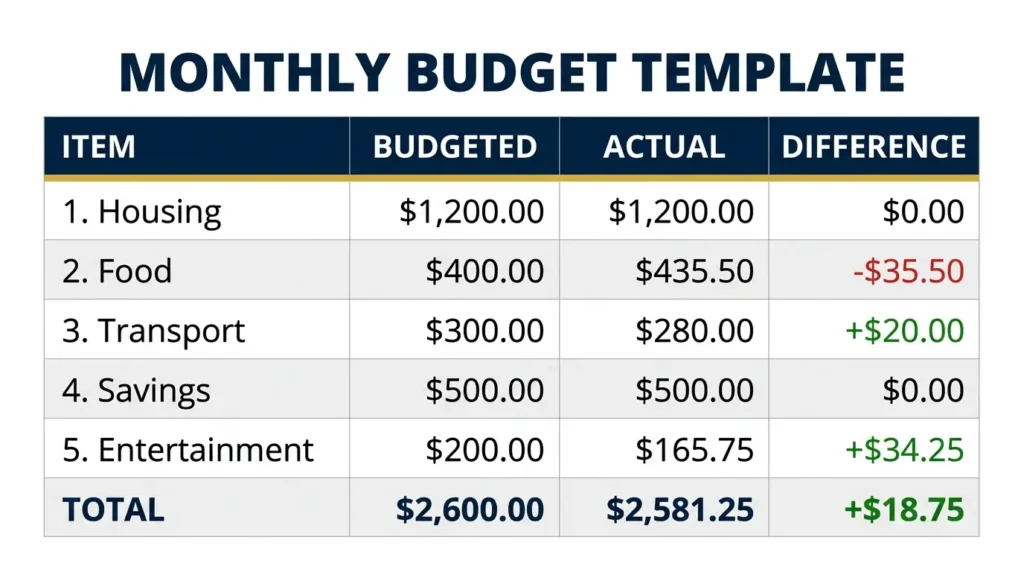

Step 5 — Build Your Monthly Budget

Now that you have your income, expenses, and method, it is time to actually make a budget. Here is a simple template to start with:

| Category | Budgeted Amount | Actual Amount | Difference |

|---|---|---|---|

| Monthly Income | $__________ | $__________ | — |

| Housing (rent/mortgage) | $__________ | $__________ | $__________ |

| Utilities + Internet + Phone | $__________ | $__________ | $__________ |

| Groceries | $__________ | $__________ | $__________ |

| Transportation | $__________ | $__________ | $__________ |

| Insurance payments | $__________ | $__________ | $__________ |

| Debt minimum payments | $__________ | $__________ | $__________ |

| Dining out / Entertainment | $__________ | $__________ | $__________ |

| Emergency fund savings | $__________ | $__________ | $__________ |

| Retirement savings | $__________ | $__________ | $__________ |

| Miscellaneous | $__________ | $__________ | $__________ |

| TOTAL EXPENSES | $__________ | $__________ | $__________ |

| NET (Income – Expenses) | $__________ | $__________ | — |

If your total expenses exceed your income, you need to reduce spending in variable categories until the budget balances. If you want to use Google Sheets to make a budget digitally, read our guide on how to use Google Sheets for budgeting — it includes formulas and a full template.

Step 6 — Track and Review Your Budget Monthly

Making a budget is only half the work — reviewing it consistently is what creates real financial change. Here is a simple weekly routine to make a budget work long-term:

- Every Sunday — spend 10 minutes updating actual spending in each category

- First of each month — review last month’s budget, identify overspending patterns, adjust next month

- After every paycheck — confirm that automatic savings transfers have gone through

- Quarterly — review your budget categories and update any that no longer reflect your life

How to Stick to Your Budget

Most people know how to make a budget — the challenge is following it. Here are the habits that make the difference:

- Automate savings transfers on payday — money that moves before you can spend it stays saved

- Use a budgeting app or Google Sheets to track spending in real time

- Give yourself a small discretionary “fun money” category — a budget with zero flexibility always fails

- Do not aim for perfection — if you overspend in one category, adjust the next month and move on

- Review your budget as a couple if you share finances — money disagreements are easier to resolve on paper than in argument

Frequently Asked Questions

How do I make a budget for beginners?

To make a budget as a beginner, follow these steps: calculate your monthly take-home income, list all fixed and variable expenses, choose a simple method like the 50/30/20 rule, set savings as a non-negotiable line item, build your budget template, and review it weekly. The 50/30/20 rule is the easiest starting point — 50% needs, 30% wants, 20% savings and debt.

How much should I budget for each category?

Common guidelines: housing 25%–35% of income, groceries 10%–15%, transportation 10%–15%, savings 15%–20%, entertainment 5%–10%. These are starting points — your budget should reflect your actual life and goals. The most important rule when you make a budget is that total expenses must not exceed total income.

What is the easiest budgeting method?

The 50/30/20 rule is the easiest method to make a budget with. It requires no detailed tracking — simply divide your after-tax income into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It works well for beginners who want structure without complexity.

How long does it take to make a budget?

Your first budget takes 45–60 minutes to set up — gathering income data, listing expenses from bank statements, and building the template. Once the structure exists, updating your budget each month takes 10–20 minutes. The weekly spending check takes just 5–10 minutes. The upfront time investment pays for itself many times over.

What should I include in my budget?

A complete budget includes: all income sources, fixed expenses (rent, loan payments, insurance), variable expenses (groceries, gas, dining), periodic expenses (annual renewals divided by 12), savings contributions (emergency fund, retirement), and debt repayment above minimums. Every dollar of income should be assigned a category.

Final Thoughts: How to Make a Budget That Actually Works

Now you know how to make a budget from scratch — the steps are simple, the tools are free, and the impact is real. The best budget is not the most detailed or complex one — it is the one you actually use every month. Start with your income, list your expenses honestly, choose a method that fits your personality, and review it every week. Within 30 days of consistently following a budget, most people find $200–$500/month they did not know they were wasting.

Making a budget is the foundation of every other financial goal — paying off debt, building an emergency fund, saving for a home, or retiring early. Once you know how to make a budget, every other financial skill becomes more achievable. Read our guide on debt consolidation explained if debt payments are consuming too much of your budget and limiting your ability to save.

Copy tout