📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is a CD account? A CD account, or certificate of deposit, is a type of savings account that pays a guaranteed fixed interest rate in exchange for leaving your money untouched for a set period — typically 3 months to 5 years. Understanding what is a CD account is valuable for anyone with savings they will not need access to in the near term, because CD accounts typically offer higher interest rates than standard savings accounts in exchange for the commitment to leave the funds locked in. This complete guide on what is a CD account explains how certificates of deposit work, current CD rates in 2026, how to compare them to other savings options, and exactly when a CD account makes sense for your money.

What Is a CD Account — The Simple Definition

A CD account is a federally insured bank deposit account that pays a fixed interest rate for a specific term — the period you agree to keep the money deposited. When the term ends (called the maturity date), you receive your original deposit back plus all the interest earned. CD accounts are offered by banks and credit unions and are insured by the FDIC or NCUA up to $250,000.

The key feature of a CD account is the tradeoff: you receive a higher guaranteed interest rate than a standard savings account, but you cannot access the money without paying an early withdrawal penalty — typically 60–150 days of interest depending on the term. A CD account is best understood as a savings commitment: you lock in a rate and let the money grow undisturbed until the term ends.

How Does a CD Account Work?

Here is the step-by-step process of how a CD account works:

- You open a CD account at a bank or credit union and deposit a lump sum — the minimum deposit is typically $500–$1,000 at most institutions

- You choose a term — the period ranges from 3 months to 5 years. Common terms are 6 months, 1 year, 2 years, and 5 years.

- The bank pays you a fixed interest rate for the entire term — this rate does not change even if market rates fall

- Interest compounds daily or monthly and accumulates in the CD account until maturity

- At the maturity date, you receive your original deposit plus all accrued interest

- You choose whether to withdraw the funds or roll them into a new CD account — most banks auto-renew at the current market rate unless you instruct otherwise

If you need to withdraw funds before the maturity date, you pay an early withdrawal penalty — typically 60–150 days of interest. For a 1-year CD at 5% APY, an early withdrawal penalty of 90 days of interest on $10,000 costs approximately $123. It is significant but rarely catastrophic — and it can be avoided by using a no-penalty CD for funds you might need early.

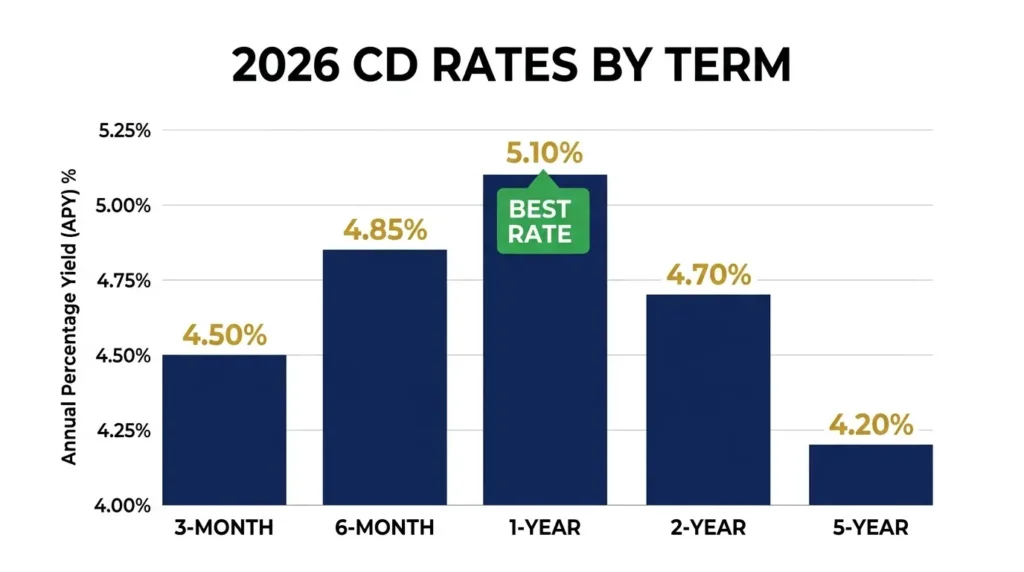

CD Account Rates in 2026

CD account rates in 2026 remain competitive as the Federal Reserve has kept rates elevated following the 2022–2024 inflation cycle. Online banks and credit unions consistently offer the highest CD rates — often significantly above the national average:

| CD Term | National Average APY | Best Online Bank Rate | Interest on $10,000 |

|---|---|---|---|

| 3-month CD | 1.60% | 4.50% | $112 |

| 6-month CD | 1.80% | 4.85% | $243 |

| 1-year CD | 1.85% | 5.10% | $510 |

| 2-year CD | 1.55% | 4.70% | $961 |

| 5-year CD | 1.40% | 4.20% | $2,289 |

The difference between the national average CD rate and the best available online bank rate is dramatic — on a $10,000 deposit for 1 year, the best rate earns $510 versus approximately $185 at the national average. Always compare CD account rates at online banks before opening one at your local branch. To understand how APY works and compares across accounts, read our guide on what APY means in savings accounts.

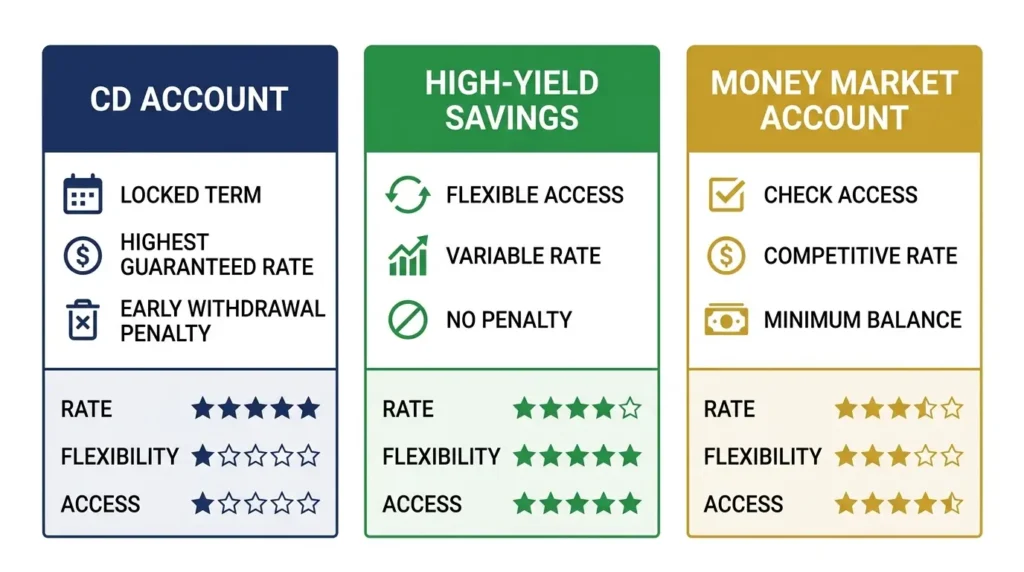

CD Account vs High-Yield Savings vs Money Market

| Feature | CD Account | High-Yield Savings | Money Market Account |

|---|---|---|---|

| Interest rate | Fixed — locked in at opening | Variable — changes with Fed rate | Variable — changes with Fed rate |

| Access to funds | Locked until maturity | Anytime, no penalty | Anytime (limited transactions) |

| Early withdrawal | Penalty (60–150 days interest) | No penalty | No penalty |

| Best current rate | Up to 5.10% APY | Up to 5.25% APY | Up to 5.00% APY |

| FDIC insured | Yes | Yes | Yes |

| Best for | Known future expense, rate lock | Emergency fund, flexible savings | Large cash reserves with check access |

In 2026, high-yield savings accounts actually offer slightly higher rates than most CD accounts — making them better for most everyday savings needs. A CD account wins when you want to lock in today’s rate before rates fall, or when you have a specific known future expense and want guaranteed return with no temptation to spend the money. For a full comparison of all savings account types, read our guide on what is a money market account and our guide on the best high-yield savings accounts 2026.

When a CD Account Makes Sense

Lock In Rates Before They Fall

When the Federal Reserve signals rate cuts ahead, locking in today’s higher rate with a CD account guarantees you earn the current rate for the full term — even as savings account rates decline. If you believe rates will be lower in 12–24 months, opening a multi-year CD today locks in the current high rate.

Saving for a Known Future Expense

A CD account is ideal for money earmarked for a specific future expense — a home down payment in 18 months, a car purchase in 12 months, or a wedding in 2 years. The locked nature of a CD account prevents you from spending the money impulsively while earning a guaranteed return until you need it.

Conservative Savers Who Want Guaranteed Returns

A CD account is one of the safest guaranteed returns available — FDIC-insured, fixed rate, zero market risk. For retirees or conservative savers who want predictable income from their cash savings without any exposure to market volatility, CD accounts are a reliable choice.

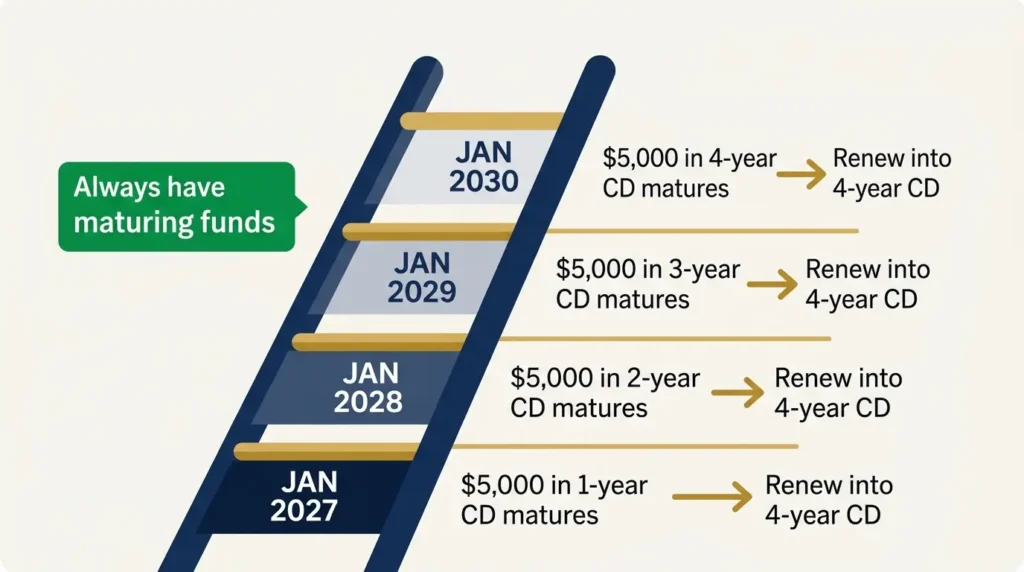

The CD Ladder Strategy

A CD ladder is a strategy to maximize CD account returns while maintaining regular access to funds. Instead of putting all your money in one long-term CD, you split it into multiple CDs with staggered maturity dates. Here is how a $20,000 CD ladder works:

- $5,000 in a 1-year CD — matures January 2027

- $5,000 in a 2-year CD — matures January 2028

- $5,000 in a 3-year CD — matures January 2029

- $5,000 in a 4-year CD — matures January 2030

Each year, one CD matures — giving you access to $5,000 annually. You can either spend the funds or roll them into a new 4-year CD at whatever the current rate is. This strategy captures higher long-term CD rates while ensuring you always have funds maturing within 12 months if you need them. The CD ladder is the most effective way to use CD accounts as part of a broader savings strategy.

Types of CD Accounts Available in 2026

- Traditional CD — fixed rate, fixed term, early withdrawal penalty. The standard CD account.

- No-Penalty CD — allows early withdrawal without penalty. Rates are slightly lower than traditional CDs but provide flexibility. Ideal if you are unsure about your timeline.

- Bump-Up CD — allows you to request one rate increase if rates rise during your term. Useful in rising rate environments.

- Jumbo CD — requires a minimum deposit of $100,000 in exchange for slightly higher rates. Only relevant for high-balance savers.

- IRA CD — a CD account held inside an Individual Retirement Account, combining the tax advantages of an IRA with the guaranteed return of a CD.

For most everyday savers in 2026, a traditional CD account or no-penalty CD from an online bank offers the best combination of rate and flexibility. Always check the early withdrawal penalty terms before opening any CD account — they vary significantly between institutions.

Frequently Asked Questions

What is a CD account and how does it work?

A CD account is a bank savings account that pays a fixed interest rate in exchange for keeping your money deposited for a set term — typically 3 months to 5 years. You deposit a lump sum, earn guaranteed interest at the agreed rate, and receive your principal plus interest at the maturity date. Early withdrawal triggers a penalty of 60–150 days of interest. CD accounts are FDIC-insured up to $250,000.

Is a CD account better than a savings account?

It depends on your needs. In 2026, high-yield savings accounts offer slightly higher rates (up to 5.25% APY) than most CD accounts (up to 5.10%), with full flexibility to withdraw anytime. A CD account wins when you want to lock in today’s rate before rates fall, or when you need the psychological discipline of locked funds. For emergency funds and everyday savings, a high-yield savings account is typically the better choice.

What is the minimum deposit for a CD account?

Most banks and credit unions require a minimum deposit of $500–$1,000 to open a CD account. Some online banks offer CD accounts with no minimum deposit — particularly for shorter terms. Jumbo CDs require $100,000 or more. Always verify the minimum deposit requirement before applying, as it varies significantly between institutions.

What happens when my CD account matures?

When your CD account matures, most banks send a notification and give you a grace period — typically 7–10 days — to decide what to do with the funds. Your options are: withdraw the money (principal plus interest), roll it into a new CD at the current market rate, or transfer it to a savings account. If you take no action during the grace period, most banks automatically renew the CD for the same term at the current rate.

Are CD accounts safe?

Yes — CD accounts at FDIC-insured banks are among the safest financial products available. Your deposit is guaranteed by the federal government up to $250,000 per depositor per institution. The interest rate is fixed and guaranteed regardless of market conditions. The only risk is opportunity cost — if rates rise significantly after you open a CD account, you are locked into a lower rate for the remainder of your term.

Final Thoughts: Is a CD Account Right for Your Money?

A CD account is a safe, guaranteed, and FDIC-insured savings tool that makes the most sense when you have money you know you will not need for a specific period and want to lock in a guaranteed rate. In 2026, with competitive CD rates at online banks reaching 5%+ for 1-year terms, a CD account offers a compelling no-risk return for the right portion of your cash savings.

Keep your emergency fund in a flexible high-yield savings account — never lock emergency money in a CD account. But for savings earmarked for a specific future goal, a CD account or CD ladder is a smart, disciplined way to maximize your guaranteed return. For the right framework to decide where every dollar of your savings belongs, read our guide on how to set financial goals.