📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

Credit card or debit card — which should you reach for when it’s time to pay? It seems like a simple choice, but the answer has significant implications for your financial security, credit score, rewards, and fraud protection. Most financial experts agree on a clear winner — and the answer might surprise you.

In this complete guide, you’ll learn the key differences between credit and debit cards, the advantages and disadvantages of each, when to use which card, and how to use credit cards responsibly to build wealth rather than debt.

Credit Card vs Debit Card: The Core Difference

The fundamental difference comes down to one thing: whose money you’re spending.

- Debit card: You spend your own money directly from your checking account. The funds are withdrawn immediately.

- Credit card: You borrow money from the card issuer and agree to pay it back later — ideally in full each month.

Both cards use the same payment networks (Visa, Mastercard, American Express, Discover) and are accepted at virtually the same locations. The difference lies entirely in where the money comes from and the protections that come with each.

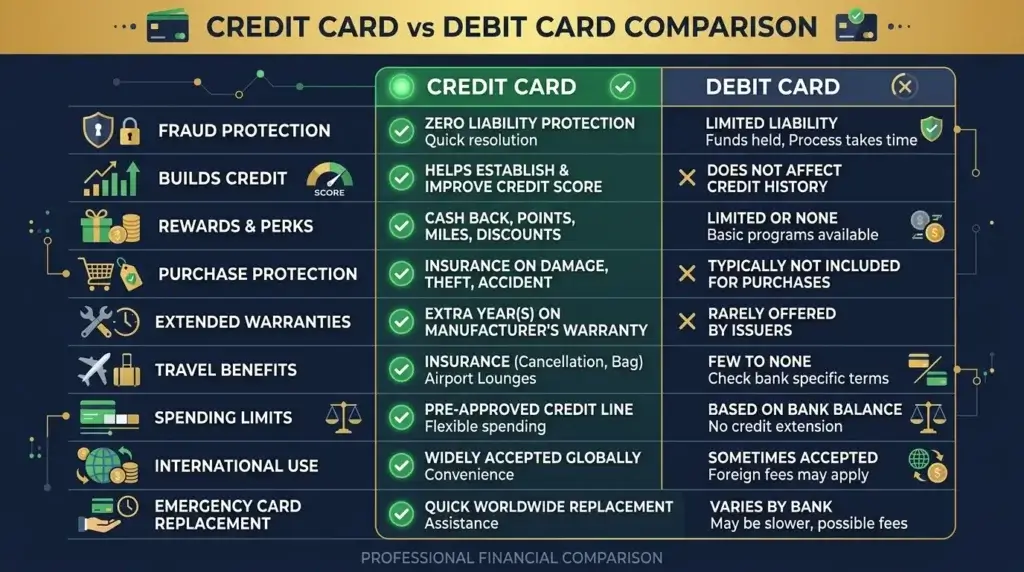

Credit Card vs Debit Card: Full Comparison

| Feature | Credit Card | Debit Card |

|---|---|---|

| Money source | Borrowed (pay back later) | Your own (withdrawn immediately) |

| Fraud protection | ✅ Excellent (zero liability) | ⚠️ Limited (time-sensitive) |

| Builds credit score | ✅ Yes | ❌ No |

| Rewards (cash back, points) | ✅ Yes | ❌ Rarely |

| Overspending risk | ⚠️ Higher (borrowed money) | ✅ Lower (limited to balance) |

| Interest charges | ❌ If not paid in full | ✅ None |

| Purchase protection | ✅ Extended warranty, dispute rights | ⚠️ Limited |

| Travel benefits | ✅ Often included | ❌ Rarely |

| Rental car coverage | ✅ Often included | ❌ Not included |

The Case for Credit Cards

1. Superior Fraud Protection

This is the most important advantage of credit cards. Under the Fair Credit Billing Act, your maximum liability for unauthorized credit card charges is $50 — and most major issuers offer $0 liability as a standard benefit.

With a debit card, your liability depends on how quickly you report the fraud. If you report within 2 business days, your liability is limited to $50. But if you wait 2 to 60 days, your liability can reach $500. After 60 days, you could lose everything in your account.

There’s another critical difference: with a credit card, the fraudulent charge never comes out of your bank account — you dispute it before paying. With a debit card, the money is already gone from your checking account, and you must wait for the bank to investigate and refund it (which can take days or weeks).

2. Builds Your Credit Score

Every time you use a credit card responsibly — making purchases and paying them off in full each month — you’re building a positive credit history. This directly improves your credit score over time.

Debit cards have absolutely no impact on your credit score. Using only a debit card means you’re missing one of the easiest ways to build credit — which affects your ability to get loans, rent apartments, and even land certain jobs.

3. Earn Rewards on Every Purchase

Many credit cards offer cash back, travel points, or other rewards on every purchase. A 2% cash back card on $2,000 of monthly spending earns $480 per year — just for using the card instead of a debit card for the same purchases you were already making.

Top reward rates by category:

- Groceries: 3% to 6% cash back

- Dining: 3% to 4% cash back

- Gas: 2% to 5% cash back

- All other purchases: 1.5% to 2% cash back

4. Purchase Protection and Extended Warranties

Many credit cards automatically extend the manufacturer’s warranty on purchases by 1 to 2 years. They also offer purchase protection — if something you bought is stolen or accidentally damaged within 90 to 120 days, the card may reimburse you. Debit cards offer none of these benefits.

5. Travel Benefits

Premium travel credit cards offer benefits that debit cards simply cannot match: rental car collision coverage, trip cancellation insurance, lost luggage reimbursement, airport lounge access, and no foreign transaction fees. If you travel even occasionally, a good travel credit card can save you significant money.

The Case for Debit Cards

1. No Risk of Debt or Interest Charges

The biggest advantage of debit cards is also the most obvious: you can only spend money you actually have. There is no risk of accumulating high-interest credit card debt because you’re spending from your own account. For people who struggle with overspending, this built-in limit is genuinely valuable.

2. No Application Required

Debit cards come automatically with most checking accounts. There’s no credit check, no application process, and no risk of rejection. If you have bad credit or are just starting to build credit history, a debit card is immediately accessible.

3. Easier Budget Tracking

Because debit card transactions immediately reduce your checking account balance, it’s easier to see in real time exactly how much money you have left to spend. Some people find this more psychologically effective for sticking to a budget than credit cards, where the bill comes later.

When to Use a Credit Card

Use your credit card for these situations — and pay the balance in full each month:

- ✅ Online purchases — Superior fraud protection if the merchant is compromised

- ✅ Travel bookings — Hotels, flights, rental cars (better protections and benefits)

- ✅ Large purchases — Extended warranty and purchase protection apply

- ✅ Gas stations — Debit card skimmers are more risky; credit is safer

- ✅ Recurring bills — Utilities, subscriptions (earn rewards passively)

- ✅ Restaurants and dining — High rewards categories, better fraud protection

When to Use a Debit Card

- ✅ ATM withdrawals — Avoid cash advance fees on credit cards

- ✅ When merchants charge credit card surcharges — Some small businesses add a fee for credit payments

- ✅ If you’re prone to overspending — The hard limit of your account balance provides automatic discipline

- ✅ Peer-to-peer payments — Venmo, Zelle, and Cash App are typically linked to debit/bank accounts

How to Use Credit Cards Responsibly

The credit card advantages above only apply if you use the card responsibly. Here are the non-negotiable rules:

Rule 1: Pay the Full Balance Every Month

This is the cardinal rule of credit card use. If you pay your balance in full each month, you pay zero interest — the card is essentially a free loan that earns you rewards. The moment you carry a balance, interest charges (typically 20% to 29% APR) can quickly erase any rewards you’ve earned.

Rule 2: Keep Your Credit Utilization Below 30%

Your credit utilization ratio — how much of your available credit you’re using — is 30% of your credit score. Keeping it below 30% (and ideally below 10%) maximizes your score. If your limit is $5,000, keep your balance below $1,500.

Rule 3: Never Miss a Payment

Set up autopay for at least the minimum payment to ensure you never miss a due date. Payment history is 35% of your credit score — a single missed payment can drop your score by 50 to 100 points. Set autopay for the full balance, not just the minimum.

Rule 4: Treat It Like a Debit Card

Only charge what you can afford to pay off this month. Never think of your credit limit as additional spending money — think of it as a convenience tool that earns you rewards on spending you were already going to do.

Which Card Should You Use? The Verdict

For most financially responsible adults, a credit card is the better choice for most purchases — but only if you follow the rules above. The combination of fraud protection, credit building, and rewards makes credit cards objectively superior to debit cards for everyday spending when used correctly.

| Your Situation | Recommended Card |

|---|---|

| You pay your balance in full every month | ✅ Credit card for most purchases |

| You sometimes carry a balance | ⚠️ Debit card until you build that habit |

| You’re building credit from scratch | ✅ Secured credit card (reports to bureaus) |

| You’ve struggled with credit card debt | ✅ Debit card until financially stable |

| You’re traveling internationally | ✅ No-foreign-fee credit card |

| ATM cash withdrawal | ✅ Debit card always |

Frequently Asked Questions

Is it better to use a credit card or debit card for everyday purchases?

Credit card, if you pay the balance in full each month. You get fraud protection, rewards, and credit building — all for free. If you tend to overspend, stick to a debit card until you build better spending habits.

Can someone steal money from my debit card?

Yes, and it’s more dangerous than credit card fraud. With debit card fraud, the money comes directly from your bank account. You must report it quickly to limit your liability. Credit card fraud never touches your bank account directly.

Does using a debit card hurt your credit score?

No — but it doesn’t help it either. Debit card transactions are not reported to the credit bureaus. Using only a debit card means you’re missing an easy opportunity to build your credit history.

What’s the best credit card for beginners?

For beginners with limited credit history, consider a secured credit card or a student credit card. The Discover it Secured Card and Capital One Platinum Secured Card are popular options. Once you’ve built a score above 670, you can upgrade to a rewards card. Read our guide on how to get your first credit card with no credit history for a full walkthrough.

Should I use a credit card for gas?

Yes — credit cards are actually safer than debit cards at gas stations. Gas pumps are a common target for card skimming devices. With a credit card, fraudulent charges don’t directly drain your bank account. Many credit cards also offer 2% to 5% cash back on gas purchases.

The Bottom Line

The credit card vs debit card debate has a clear answer for most people: use a credit card for most purchases — but only if you pay the full balance every single month. The fraud protection, credit building benefits, and rewards make credit cards significantly more valuable than debit cards for everyday spending.

If you’re ready to start using credit cards strategically, read our guide on how to build credit from scratch to understand the full picture. And if you’re looking for the right card to start with, check our list of the best secured credit cards for beginners.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Credit card terms and rewards programs change frequently. Always verify current offers directly with card issuers before applying.