📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

Most people glance at their credit card statement, check the minimum payment, and move on. But your credit card statement contains critical information that directly impacts your credit score, finances, and financial security. Knowing how to read it properly can help you catch errors, avoid unnecessary fees, and make smarter money decisions every month.

In this complete guide, you’ll learn every section of a credit card statement, what each number means, what to watch out for, and the three most important actions to take every time your statement arrives.

Why Reading Your Credit Card Statement Matters

Before diving into the details, here is why this skill is essential:

- Catch fraud early: Reviewing every transaction lets you spot unauthorized charges before they become a bigger problem.

- Avoid fees: Understanding due dates, minimum payments, and grace periods helps you avoid late fees and interest charges.

- Monitor your credit utilization: Your statement balance directly affects your credit score — knowing this number is critical.

- Track your spending: Your statement is a detailed record of where your money went each month.

- Verify accuracy: Billing errors are more common than most people realize — and you have the right to dispute them.

The 10 Key Sections of a Credit Card Statement

1. Account Summary

Usually at the top of the statement, the account summary gives you a quick snapshot of your account. It typically includes:

- Previous balance: What you owed at the end of last month’s billing cycle

- Payments and credits: Payments made and any credits applied during the billing period

- Purchases: Total new charges made during the billing period

- Fees charged: Any fees added (late fees, annual fees, etc.)

- Interest charged: Interest added if you carried a balance

- New balance: What you owe today — the total you need to pay

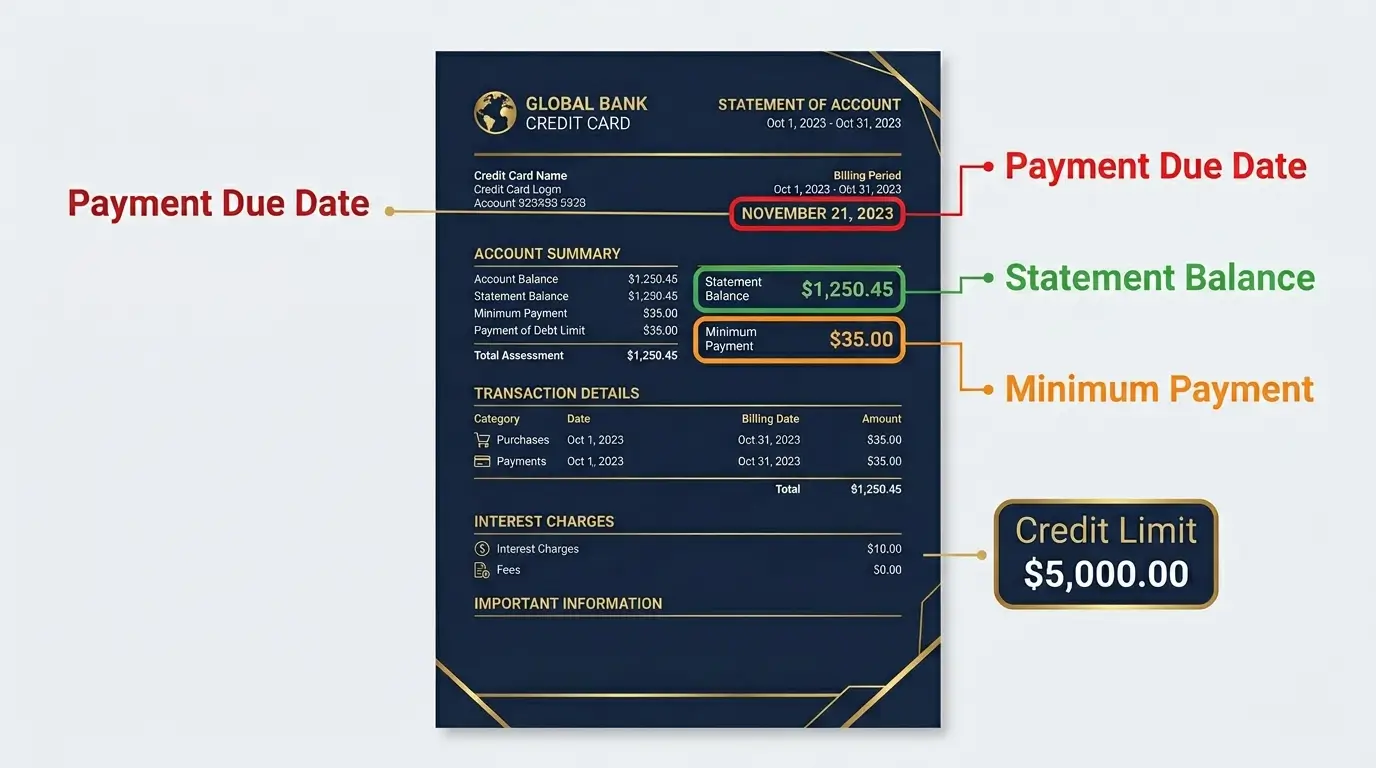

2. Payment Information

This is arguably the most important section. It contains three critical numbers:

- Payment due date: The date by which you must pay to avoid a late fee. Pay at least 3 to 5 days before this date to account for processing time.

- Minimum payment due: The smallest amount you can pay without triggering a late fee. Paying only the minimum is very costly — more on this below.

- Statement balance (New balance): The amount you owe in full. Paying this amount in full by the due date means you pay zero interest.

Pro tip: Always pay the statement balance in full — not just the minimum. The minimum payment is designed to keep you in debt as long as possible, maximizing the interest the bank collects from you.

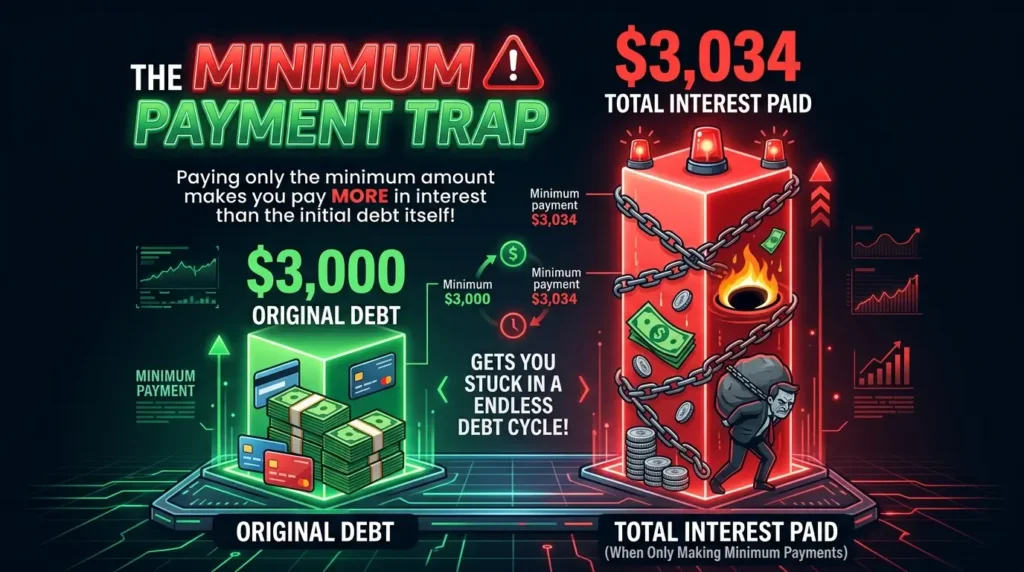

3. The Minimum Payment Warning

Since 2010, credit card statements in the US are legally required to include a minimum payment warning. This section shows you:

- How long it will take to pay off your balance if you only make minimum payments

- How much total interest you will pay over that period

- How much you’d need to pay monthly to eliminate the debt in 3 years

This section is eye-opening. A $3,000 balance at 22% APR, paid with minimum payments only, could take over 12 years to pay off and cost $3,000+ in interest alone — more than the original debt.

4. Credit Limit and Available Credit

This section shows:

- Credit limit: The maximum you’re allowed to charge on the card

- Available credit: How much credit you still have left to use (credit limit minus current balance)

- Cash advance limit: How much you can withdraw as cash (usually a fraction of your credit limit, with very high fees)

Your credit utilization ratio — your balance divided by your credit limit — accounts for 30% of your credit score. Keeping your balance below 30% of your limit (and ideally below 10%) is one of the fastest ways to improve your score.

5. Transaction List

The transaction list is a detailed record of every purchase, payment, fee, and credit applied to your account during the billing period. Each entry typically shows:

- Transaction date and posting date

- Merchant name and location

- Transaction amount

- Transaction type (purchase, payment, fee, credit)

Review every single transaction. Fraudulent charges and billing errors are caught here. If you see a charge you don’t recognize, contact your card issuer immediately. Under the Fair Credit Billing Act, you have the right to dispute errors within 60 days of the statement date.

6. Interest Charge Calculation

If you carry a balance, this section breaks down exactly how your interest was calculated. It shows your Annual Percentage Rate (APR) and your Daily Periodic Rate (APR divided by 365), which is applied to your average daily balance.

Different types of transactions often have different APRs:

- Purchase APR: For regular purchases (typically 18% to 29%)

- Cash advance APR: For cash withdrawals (often 25% to 30%, with no grace period)

- Balance transfer APR: For transferred balances (may be promotional 0%)

- Penalty APR: Applied after late payments (can be as high as 29.99%)

7. Rewards Summary

If your card earns rewards, this section shows:

- Points, miles, or cash back earned this period

- Total rewards balance available to redeem

- Any rewards expiration dates

- Redemption options and instructions

Check this section regularly to ensure you’re earning the rewards you expect and to redeem them before they expire.

8. Billing Period Dates

The billing period (or billing cycle) is the timeframe covered by the statement — typically 28 to 31 days. Any charges made after the billing period closes will appear on your next statement. Understanding your billing cycle helps you time large purchases to maximize your interest-free period.

9. Important Notices and Disclosures

This section contains legal notices, changes to your account terms, and important disclosures. While it’s easy to skip, always read it — card issuers are required to give you advance notice before changing your APR, fees, or other key terms. This is where you’ll find out about upcoming changes that may affect your card strategy.

10. Contact Information and Dispute Instructions

Your statement includes your card issuer’s customer service number and instructions for disputing billing errors. Note these down — if you spot a fraudulent charge or billing error, you’ll need this information to act quickly within the dispute window.

The True Cost of Paying Only the Minimum

The minimum payment trap is one of the most expensive mistakes in personal finance. Here is a real example of what minimum-only payments cost:

| Balance | APR | Min. Payment | Time to Pay Off | Total Interest Paid |

|---|---|---|---|---|

| $1,000 | 22% | ~$25/month | 5 years 3 months | $626 |

| $3,000 | 22% | ~$60/month | 12+ years | $3,034 |

| $5,000 | 22% | ~$100/month | 18+ years | $6,200 |

| $10,000 | 22% | ~$200/month | 25+ years | $14,000+ |

On a $10,000 balance, you would pay more in interest than you originally borrowed — and it would take 25 years. This is exactly why paying the full statement balance each month is the most important credit card habit you can develop.

3 Things to Do Every Time Your Statement Arrives

Action 1: Review Every Transaction

Go through the transaction list line by line. Flag anything you don’t recognize. Small test charges by fraudsters (often $1 or less) can be easy to miss. If you spot an error or unauthorized charge, call the number on the back of your card immediately.

Action 2: Note Your Credit Utilization

Divide your statement balance by your credit limit. If the result is above 30%, prioritize paying it down before the next statement closes — this is the number that gets reported to the credit bureaus and affects your score.

Action 3: Schedule Full Payment Before the Due Date

Schedule your full payment immediately after reviewing the statement — don’t wait until the due date. Set up autopay for the full statement balance to ensure you never accidentally carry a balance. If you can’t pay the full amount, pay as much as possible and make a plan to eliminate the remaining balance next month.

How to Dispute a Credit Card Charge

If you find an error or unauthorized charge on your statement, here is how to dispute it:

- Contact the merchant first — For billing errors (wrong amount, duplicate charge), contact the merchant directly. Many issues are resolved quickly this way.

- Call your card issuer — Use the number on the back of your card to report fraud or unresolved errors. Have the transaction details ready.

- Submit a written dispute — For significant disputes, follow up in writing within 60 days of the statement date. Under the Fair Credit Billing Act, the issuer must acknowledge your dispute within 30 days and resolve it within two billing cycles.

- Don’t pay the disputed amount — You are not required to pay a disputed charge while it’s under investigation.

- Monitor the resolution — Follow up to ensure the charge is removed or corrected on your next statement.

Frequently Asked Questions About Credit Card Statements

What is the difference between the statement balance and the current balance?

Your statement balance is what you owed when your billing cycle closed — this is the amount to pay in full to avoid interest. Your current balance includes any new charges made after the statement closed. To avoid interest, pay the statement balance (not the current balance, which may be higher due to recent purchases).

What happens if I miss my payment due date?

Missing your due date typically triggers a late fee (usually $25 to $40) and can trigger a penalty APR as high as 29.99%. If your payment is more than 30 days late, the issuer may report it to the credit bureaus, which can significantly damage your credit score. If you miss a payment accidentally, call your issuer immediately — many will waive the first late fee as a courtesy.

How long should I keep my credit card statements?

Keep statements for at least 60 days in case you need to dispute a charge. For tax purposes, keep statements that include deductible business expenses for at least 3 years. Most issuers provide online access to statements for 12 to 24 months.

What does “statement closing date” mean?

The statement closing date (or billing cycle end date) is when your billing period ends and your statement is generated. Any purchases made after this date will appear on your next month’s statement. The balance on this date is typically what gets reported to the credit bureaus.

What is a grace period?

The grace period is the time between your statement closing date and your payment due date — typically 21 to 25 days. During this period, you owe no interest on new purchases if you paid your previous balance in full. If you carry a balance from month to month, you lose the grace period and interest begins accruing immediately on new purchases.

The Bottom Line

Your credit card statement is one of the most important financial documents you receive each month. Taking 5 to 10 minutes to review it thoroughly can save you from fraud, unnecessary fees, and the devastating cost of minimum payment interest.

The three habits that matter most: review every transaction, keep your utilization below 30%, and pay your statement balance in full every month. Master these three and your credit card becomes a powerful financial tool rather than a debt trap.

Ready to take the next step? Learn how your statement balance affects your score in our guide on what is a credit score, or discover how to use credit strategically with our guide on credit card vs debit card. If you’re working on paying off existing card debt, read our comparison of the debt snowball vs debt avalanche methods.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Credit card terms, fees, and APRs vary by issuer. Always read your cardholder agreement and contact your card issuer directly for account-specific questions.