📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to retire early is the financial goal that motivates millions of Americans to take their money seriously — and with the right strategy, it is more achievable than most people believe. Learning how to retire early does not require a six-figure income, an inheritance, or extreme deprivation. It requires a high savings rate, low-cost index fund investing, and a clear understanding of the FIRE framework — Financial Independence, Retire Early. This complete guide on how to retire early explains the math, the strategy, and the exact steps to build the portfolio and lifestyle that allows you to leave work on your own terms in 2026.

What Does It Mean to Retire Early?

Retiring early means reaching financial independence — the point where your investment portfolio generates enough passive income to cover your living expenses indefinitely, without ever needing to work again. When you retire early under the FIRE model, you do not necessarily stop being productive. You stop being dependent on a paycheck. You work on what you choose, when you choose, because you want to — not because you need the income.

The typical FIRE goal is to retire early — often in your 40s or even 30s — rather than at the traditional retirement age of 65. The earlier you reach financial independence, the more years of freedom you gain. Someone who achieves financial independence at 45 instead of 65 gains 20 additional years of life outside mandatory employment — two full decades of time, health, and freedom that traditional retirement planning simply does not deliver.

What Is Your FIRE Number?

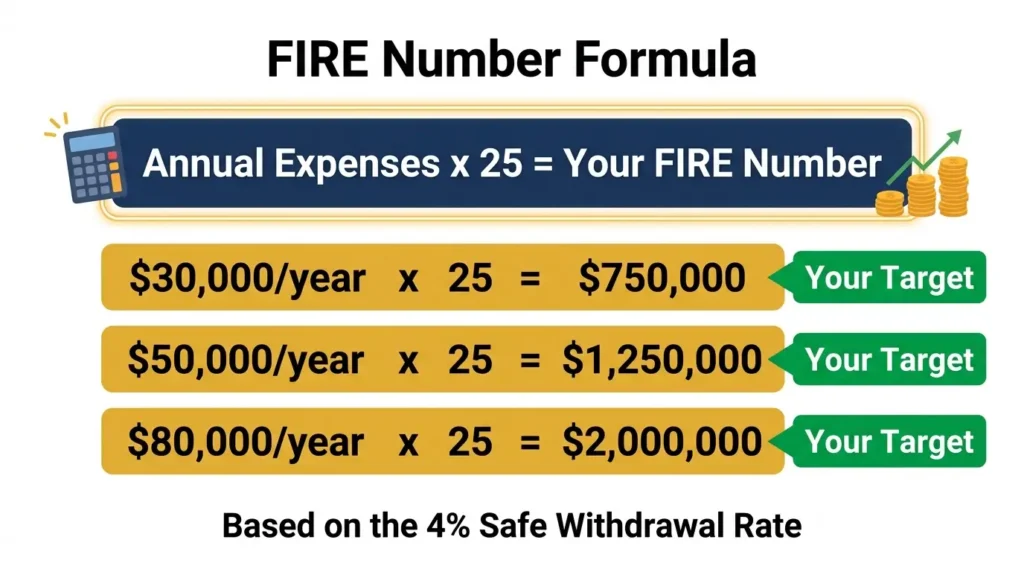

The first step to retire early is calculating your FIRE number — the exact portfolio size you need to achieve financial independence. The calculation is based on the 4% Safe Withdrawal Rate, derived from the Trinity Study: a portfolio invested in stocks and bonds can sustain a 4% annual withdrawal rate indefinitely with a very high probability of not running out of money over 30+ years.

The FIRE number formula is simple: multiply your annual expenses by 25.

| Annual Expenses | FIRE Number (25x) | Monthly Withdrawal at 4% | Lifestyle Description |

|---|---|---|---|

| $25,000/year | $625,000 | $2,083/month | Lean FIRE — frugal, minimal |

| $40,000/year | $1,000,000 | $3,333/month | Standard FIRE — comfortable |

| $60,000/year | $1,500,000 | $5,000/month | Standard FIRE — comfortable |

| $100,000/year | $2,500,000 | $8,333/month | Fat FIRE — luxurious lifestyle |

Your FIRE number is not fixed — it is directly controlled by your annual spending. Every dollar you permanently reduce from your annual expenses does two things simultaneously: it requires $25 less in your FIRE portfolio, AND it frees up an extra dollar per year to invest toward reaching that portfolio faster. Reducing spending is the most powerful lever to retire early. Read our guide on what is net worth to start tracking your progress toward your FIRE number today.

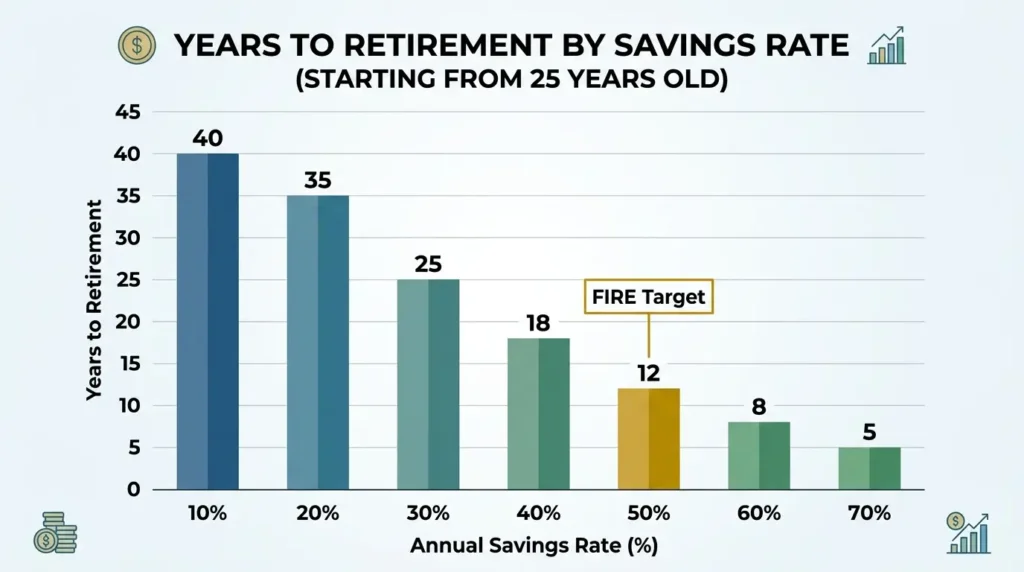

The Savings Rate Is Everything

To retire early, your savings rate — the percentage of your income you invest — is the single most important variable. Your savings rate determines how many years until you reach your FIRE number. Here is the mathematical reality, assuming a 7% real return on investments starting from zero:

| Savings Rate | Years to Financial Independence | Retire Early at (Starting at 25) |

|---|---|---|

| 10% | ~40 years | Age 65 (traditional retirement) |

| 20% | ~35 years | Age 60 |

| 30% | ~25 years | Age 50 |

| 40% | ~18 years | Age 43 |

| 50% | ~12 years | Age 37 |

| 60% | ~8 years | Age 33 |

| 70% | ~5 years | Age 30 |

Moving from a 20% to a 50% savings rate cuts 23 years off your working life. The path to retire early is not primarily about earning more — it is about aggressively widening the gap between your income and your expenses, and investing that gap in low-cost index funds. Read our guide on how to build wealth in your 30s for the decade-by-decade strategy.

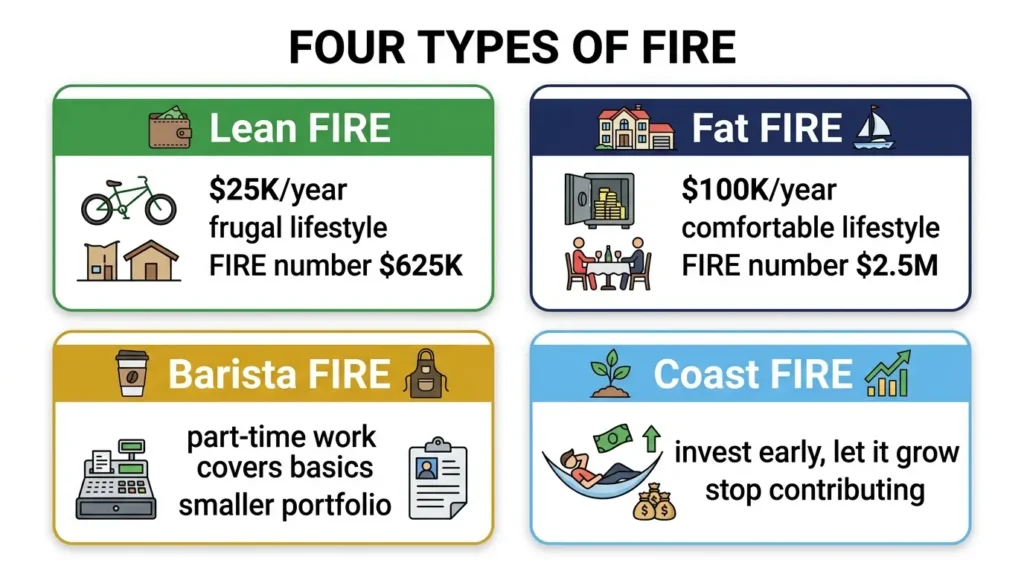

Types of FIRE: Which Path Is Right for You?

Lean FIRE

Lean FIRE means retiring early on a frugal budget — typically $25,000–$40,000/year in expenses, requiring a portfolio of $625,000–$1,000,000. Lean FIRE is achievable faster because both the required portfolio is smaller and the savings rate tends to be higher due to reduced spending. Best for people who genuinely value minimalism and low-consumption lifestyles over material abundance.

Fat FIRE

Fat FIRE means retiring early with a comfortable or even luxurious lifestyle — typically $80,000–$150,000/year in expenses, requiring a portfolio of $2,000,000–$3,750,000. Fat FIRE takes longer to achieve but provides financial independence without lifestyle sacrifice. Best for high earners who want freedom without giving up travel, dining, and experiences.

Barista FIRE

Barista FIRE is a hybrid approach: you build a smaller portfolio that covers most expenses, then supplement with part-time or flexible work that covers the rest. The “barista” name comes from working a low-stress part-time job (like a barista) for income and health benefits while your portfolio continues growing. Best for people who want to escape full-time employment before their full FIRE number is reached.

Coast FIRE

Coast FIRE means investing aggressively early in your career until your portfolio is large enough to grow to your FIRE number on its own — without any additional contributions. Once you hit your Coast FIRE number, you can “coast” — work a lower-stress, lower-paying job just to cover living expenses, while your existing portfolio compounds to full FIRE by traditional retirement age. This is the most accessible form of retire early planning for people in their 20s and early 30s.

How to Invest to Retire Early

The investment strategy to retire early is not complicated — it is consistent, low-cost index fund investing maximized across every available tax-advantaged account:

- Max your 401(k) to the employer match first — free money is the highest guaranteed return available ($24,500 limit in 2026)

- Max your Roth IRA every year — $7,500 in 2026, growing completely tax-free. Read our guide on what a Roth IRA is.

- Max your 401(k) beyond the match — up to the full $24,500 annual limit

- Open a taxable brokerage account — invest every additional dollar in low-cost index funds with no contribution limit

- Invest in broad market index funds — VOO, VTI, or FZROX at 0.00%–0.03% expense ratios. Read our guide on how to invest in index funds.

One important note for early retirees: the standard 401(k) and IRA have a 59.5 penalty-free withdrawal age. If you plan to retire early at 40 or 45, you need taxable brokerage investments to bridge the gap until retirement accounts are accessible. Plan your portfolio allocation accordingly — enough in taxable accounts to fund your early retirement years, with retirement accounts continuing to grow for later decades.

The 4% Safe Withdrawal Rate Explained

The 4% rule is the cornerstone of how to retire early planning. It states that a diversified portfolio of stocks and bonds can sustain annual withdrawals of 4% of the initial portfolio value — adjusted annually for inflation — for at least 30 years with a 95%+ success rate, based on historical market data. Here is how the math works in practice:

- You have a $1,500,000 portfolio

- Year 1: You withdraw $60,000 (4% of $1.5M)

- Year 2: You withdraw $61,800 (adjusted 3% for inflation)

- The remaining portfolio continues to grow through market returns, sustaining future withdrawals

For very early retirees (retiring at 35–45 with a 50+ year horizon), some FIRE researchers recommend a more conservative 3%–3.5% withdrawal rate to account for the longer time period. This means your FIRE number would be 29–33 times your annual expenses instead of 25 times.

Practical Steps to Retire Early Starting Today

- Calculate your current annual expenses — track every dollar spent for 3 months to get an accurate number

- Calculate your FIRE number — multiply annual expenses by 25

- Calculate your current net worth — the gap between your FIRE number and your net worth is the work ahead. Read our guide on what is net worth.

- Maximize your savings rate — reduce expenses aggressively, increase income deliberately, invest the difference immediately

- Open every tax-advantaged account available — 401(k), Roth IRA, HSA if eligible

- Invest 100% in low-cost broad market index funds — no active funds, no individual stocks

- Track your progress quarterly — watch your portfolio grow toward your FIRE number

- Build a withdrawal plan — decide which accounts to draw from first in early retirement to minimize taxes

The full financial plan framework for reaching these milestones is in our guide on how to create a financial plan. And for the decade-specific strategy for your 20s, read our guide on saving for retirement at 25 — the earlier you start, the lower your required savings rate to retire early.

Frequently Asked Questions

How much money do I need to retire early?

To retire early, you need 25 times your annual expenses — this is your FIRE number. If you spend $50,000/year, you need a $1,250,000 portfolio. If you spend $40,000/year, you need $1,000,000. The 4% safe withdrawal rate means a portfolio of that size can sustain your expenses indefinitely based on historical market returns. Reducing your annual expenses is the fastest way to lower your required number.

How to retire early with a normal income?

Most FIRE success stories come from people with average incomes who achieved a high savings rate — not high earners. On a $70,000 household income, saving and investing 40%–50% ($28,000–$35,000/year) can reach financial independence in 15–20 years. The key levers are: minimize housing costs (keep below 25% of income), eliminate car debt, cook at home, and invest 100% of income increases rather than inflating your lifestyle.

What age can you realistically retire early?

With a 50% savings rate starting at 25, financial independence is achievable by age 37. With a 40% savings rate, by age 43. With a 30% savings rate, by age 50. The earlier you start and the higher your savings rate, the earlier you can retire. Many FIRE practitioners retire in their 40s on incomes of $80,000–$120,000 per household — not by earning more, but by spending significantly less than their peers.

What do you do for health insurance when you retire early?

Health insurance is one of the most significant challenges to retire early before Medicare eligibility at 65. Options include: ACA marketplace plans (premium subsidies are substantial at FIRE-level incomes), Health Sharing Ministries, part-time work that provides benefits (Barista FIRE), a spouse’s employer plan, or COBRA for a transitional period. Many FIRE practitioners build healthcare costs directly into their annual expense estimate when calculating their FIRE number.

Is the 4% rule safe for early retirement?

The 4% rule was designed for 30-year retirements — meaning it has a 95%+ success rate for people retiring at 65. For early retirees with a 40–50 year horizon, a more conservative 3%–3.5% withdrawal rate significantly improves long-term portfolio survival rates. Most FIRE practitioners also maintain flexibility — reducing withdrawals during market downturns, doing occasional consulting work, or building in a cash buffer — to make the 4% rule more robust over longer periods.

Final Thoughts: How to Retire Early Is a Choice Available to More People Than They Think

Knowing how to retire early is not about escaping work — it is about building a life where work is optional. The FIRE framework gives you a clear mathematical target, a proven investment strategy, and the freedom to design your own timeline. Whether you aim for Lean FIRE at 35, Standard FIRE at 45, or Fat FIRE at 55, the path is the same: maximize your savings rate, minimize expenses, invest consistently in low-cost index funds, and let compound interest close the gap between where you are and where you want to be.

Every dollar you save and invest today is a dollar that earns more dollars while you sleep. That compounding, sustained over 10–20 years with discipline and intention, is how to retire early. Start tracking your FIRE number today, maximize every tax-advantaged account available to you, and commit to a savings rate that makes your early retirement timeline real.