📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

Roth IRA vs Traditional IRA — this is one of the most important retirement decisions you will make, and the right answer depends entirely on your tax situation. Understanding the Roth IRA vs Traditional IRA comparison is essential because both accounts offer powerful tax advantages, but they work in opposite directions. The Roth IRA vs Traditional IRA choice determines whether you pay taxes now or later — and that single decision can mean tens of thousands of dollars in retirement. This complete guide on Roth IRA vs Traditional IRA covers every key difference, the 2026 rules, and exactly how to choose the right one for your situation.

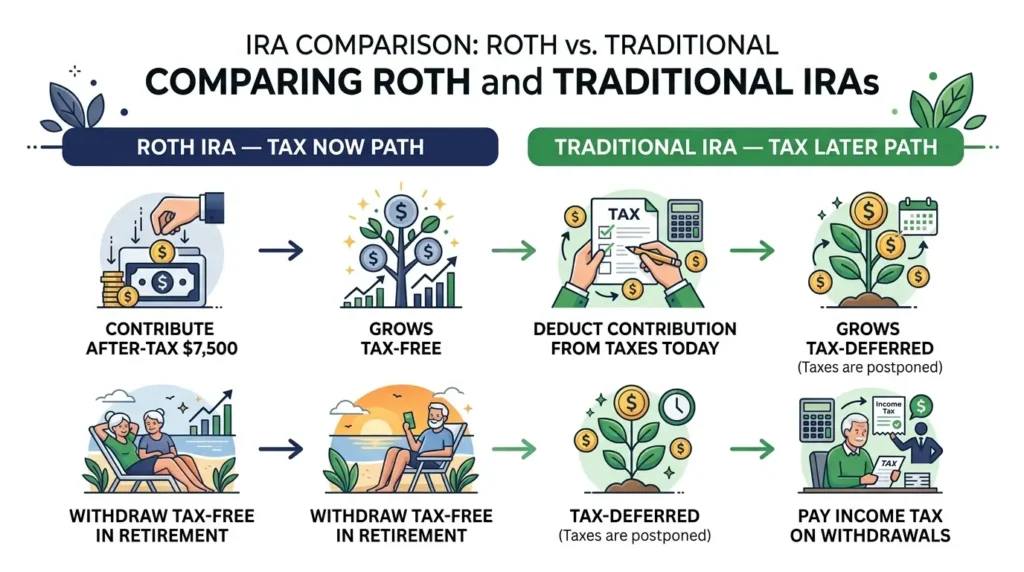

Roth IRA vs Traditional IRA: The Core Difference

The fundamental difference in the Roth IRA vs Traditional IRA comparison is when you pay taxes on your money:

- Roth IRA — you contribute after-tax dollars. Your money grows completely tax-free, and withdrawals in retirement are 100% tax-free. You pay taxes now, never again.

- Traditional IRA — you contribute pre-tax dollars (if you qualify for the deduction). Your money grows tax-deferred, and withdrawals in retirement are taxed as ordinary income. You defer taxes now, pay them later.

Both accounts grow through the same investment options — stocks, bonds, ETFs, mutual funds. Both have the same contribution limits. The only meaningful difference is when the IRS collects its share — and that timing determines which account wins for your specific situation.

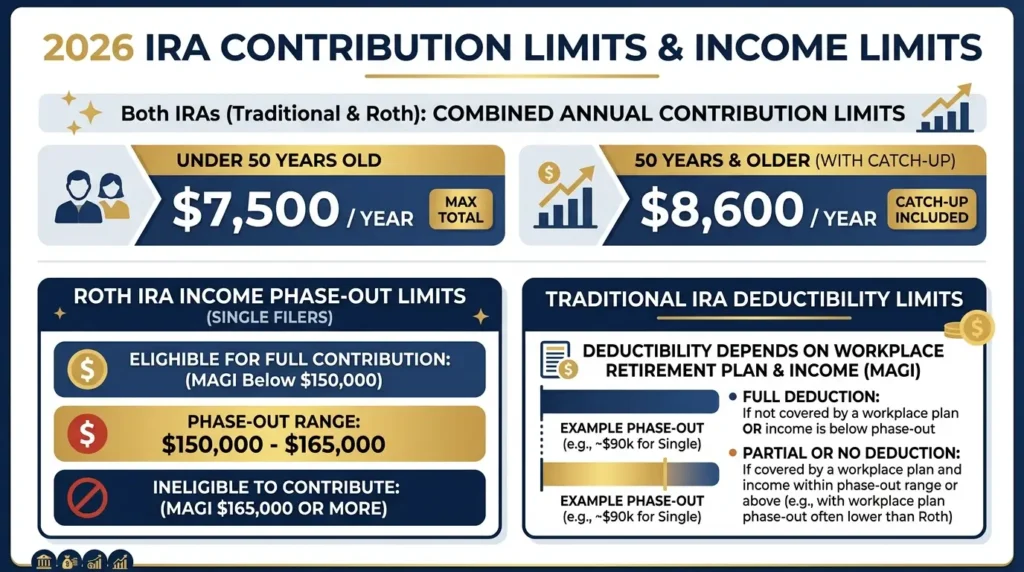

Roth IRA vs Traditional IRA: 2026 Contribution Limits

| Rule | Roth IRA (2026) | Traditional IRA (2026) |

|---|---|---|

| Annual contribution limit (under 50) | $7,500 | $7,500 |

| Annual contribution limit (50+) | $8,600 (catch-up) | $8,600 (catch-up) |

| Income limit to contribute | Yes — phases out $150K–$165K (single) / $236K–$246K (married) | No income limit to contribute |

| Tax deduction on contributions | No — after-tax contributions | Yes — if income qualifies |

| Tax on withdrawals in retirement | None — 100% tax-free | Yes — taxed as ordinary income |

| Required minimum distributions (RMDs) | None during owner’s lifetime | Yes — starting at age 73 |

| Early withdrawal penalty (before 59½) | Contributions: no penalty. Earnings: 10% penalty + tax. | All withdrawals: 10% penalty + tax |

Roth IRA vs Traditional IRA: Income Rules

Roth IRA Income Limits in 2026

To contribute to a Roth IRA in 2026, your modified adjusted gross income (MAGI) must be below the phase-out range. Above the upper limit, Roth IRA contributions are not allowed:

- Single filers: Full contribution allowed below $150,000. Phase-out $150,000–$165,000. No contribution above $165,000.

- Married filing jointly: Full contribution below $236,000. Phase-out $236,000–$246,000. No contribution above $246,000.

Traditional IRA Deductibility in 2026

Anyone with earned income can contribute to a Traditional IRA — but the tax deduction is only available if your income is below certain thresholds AND you or your spouse are not covered by a workplace retirement plan:

- If neither spouse has a workplace plan: full deduction at any income level

- If covered by workplace plan (single): deduction phases out $79,000–$89,000

- If covered by workplace plan (married filing jointly): deduction phases out $126,000–$146,000

If you earn too much to deduct Traditional IRA contributions AND too much to contribute to a Roth IRA, there is a strategy called the Backdoor Roth IRA — contributing to a non-deductible Traditional IRA and immediately converting it to a Roth IRA. This advanced strategy is worth exploring if you are a high earner.

Roth IRA vs Traditional IRA: Full Comparison

| Feature | Roth IRA | Traditional IRA | Winner |

|---|---|---|---|

| Tax on contributions | After-tax (no deduction) | Pre-tax (deductible if eligible) | Traditional (if you want deduction now) |

| Tax on growth | Tax-free | Tax-deferred | Tie |

| Tax on withdrawals | 0% — tax-free | Taxed as income | Roth |

| Income limits | Yes — restricted for high earners | No limit to contribute | Traditional (more accessible) |

| Required distributions | None ever | Required at 73 | Roth |

| Early access to contributions | Yes — anytime, no penalty | No — 10% penalty before 59½ | Roth |

| Best tax scenario | You expect higher taxes in retirement | You expect lower taxes in retirement | Depends on your situation |

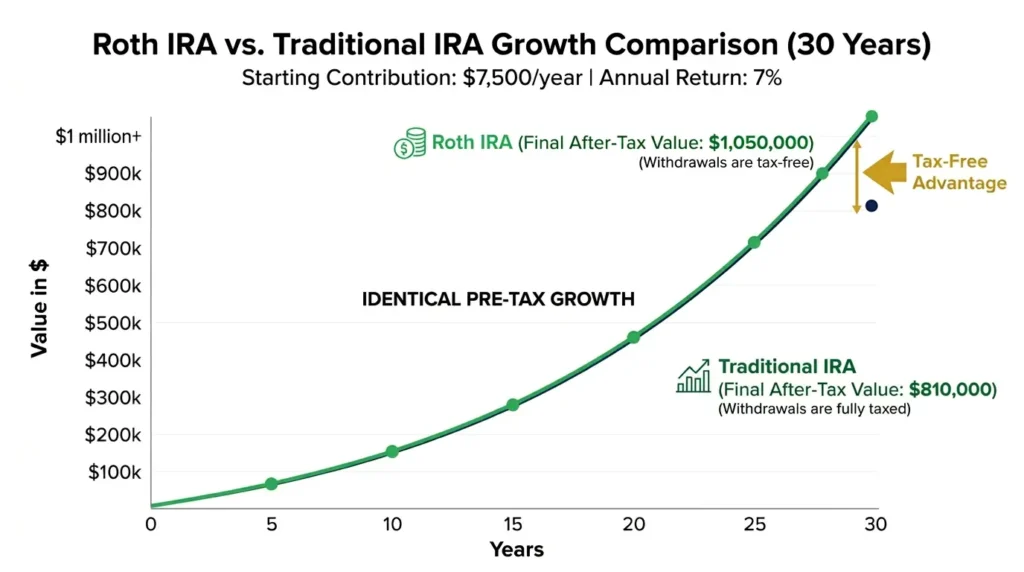

Which Produces More Wealth Over Time?

The Roth IRA vs Traditional IRA wealth comparison depends on one key variable: whether your tax rate is higher now or in retirement.

- If your tax rate is the same now and in retirement — both accounts produce identical after-tax wealth

- If your tax rate is higher in retirement than now — Roth IRA wins (you locked in a lower rate by paying taxes now)

- If your tax rate is lower in retirement than now — Traditional IRA wins (you got the deduction at a higher rate and will pay less later)

For most people in their 20s and 30s who are in lower tax brackets now and expect to earn more (and be in higher brackets) later, the Roth IRA is the mathematically superior choice. At age 25, paying a 22% tax now to avoid a potential 32% tax in retirement is an excellent deal.

For people in their peak earning years (40s–50s) in a high tax bracket who expect a lower income in retirement, the Traditional IRA deduction may produce more after-tax wealth by deferring taxes from a 35% bracket now to a 22% bracket in retirement.

When to Choose a Roth IRA

- You are in your 20s or early 30s — you are likely in a lower tax bracket now than you will be at peak earnings

- You expect your income to grow significantly over your career

- You expect tax rates to be higher in the future (a reasonable assumption given US government debt)

- You want flexibility — Roth contributions (not earnings) can be withdrawn penalty-free anytime for any reason

- You want to avoid required minimum distributions — Roth IRAs have no RMDs during your lifetime

- Your income qualifies — you are below the Roth IRA income limit ($150,000 for single filers in 2026)

For a complete guide on the Roth IRA, read our guide on what a Roth IRA is.

When to Choose a Traditional IRA

- You are in your peak earning years (40s–50s) in a high tax bracket and expect lower income in retirement

- You need the tax deduction now to lower your current-year tax bill

- Your income is too high for Roth IRA contributions (above $165,000 single / $246,000 married in 2026)

- You are self-employed and want to reduce taxable income significantly

- You expect tax rates to be lower in the future

Can You Have Both a Roth IRA and a Traditional IRA?

Yes — you can contribute to both a Roth IRA and a Traditional IRA in the same year, but your total contributions across both accounts cannot exceed the annual limit ($7,500 in 2026 for those under 50). For example, you could contribute $4,000 to a Roth IRA and $3,500 to a Traditional IRA — but not $7,500 to each.

Both IRAs can also be held alongside a 401(k) at work. The most common optimal strategy for many Americans in their 30s: contribute to 401(k) up to the employer match, then max the Roth IRA, then return to the 401(k). Read our guides on what a 401(k) is and saving for retirement at 25 for the complete retirement savings roadmap.

Frequently Asked Questions

Is a Roth IRA or Traditional IRA better for most people?

For most people in their 20s and 30s, the Roth IRA vs Traditional IRA comparison favors the Roth IRA. Younger investors are typically in lower tax brackets now than they will be at peak earnings or in retirement, making it advantageous to pay taxes now at a lower rate and enjoy tax-free growth for 30–40 years. The flexibility of Roth contributions — accessible without penalty anytime — also makes it the preferred choice for most beginners.

What are the income limits for Roth IRA vs Traditional IRA in 2026?

For the Roth IRA in 2026, single filers can contribute the full amount below $150,000 MAGI, with a phase-out up to $165,000. Married filing jointly: full contribution below $236,000, phase-out to $246,000. The Traditional IRA has no income limit for contributions — but the tax deduction phases out between $79,000–$89,000 for single filers covered by a workplace plan.

Can I convert a Traditional IRA to a Roth IRA?

Yes — a Roth conversion allows you to move money from a Traditional IRA to a Roth IRA at any time. You pay income tax on the amount converted in the year of conversion, but all future growth and qualified withdrawals are then tax-free. Roth conversions are a powerful strategy for people in low-income years or retirees in lower tax brackets.

What is the contribution limit for IRA accounts in 2026?

The 2026 IRA contribution limit is $7,500 per year for people under age 50, and $8,600 per year for people age 50 and older (catch-up contribution). This limit applies to the combined total of all IRA contributions — you cannot contribute $7,500 to a Roth IRA and another $7,500 to a Traditional IRA in the same year.

Should I max out my Roth IRA or 401(k) first?

The optimal order: first contribute to your 401(k) enough to capture the full employer match — that is a guaranteed 50%–100% return. Then max your Roth IRA ($7,500 in 2026). Then return to your 401(k) and contribute as much as possible toward the $24,500 annual limit. This order maximizes free money while prioritizing the most tax-advantaged account available.

Final Thoughts: Roth IRA vs Traditional IRA — Make the Decision Today

The Roth IRA vs Traditional IRA debate does not need to be resolved with perfect certainty — it needs to be acted on. For most people in their 20s and 30s, the Roth IRA is the stronger default choice. For high earners in their peak years, the Traditional IRA deduction may provide more immediate value. When in doubt, the Roth IRA’s flexibility — tax-free growth, no required distributions, penalty-free access to contributions — makes it the lower-risk choice.

Open whichever account fits your situation today, contribute monthly through low-cost index funds, and let compound interest do the work over decades. To understand how that growth compounds, read our guide on what is compound interest. And to see how both IRAs fit into your broader investment strategy, read our guide on the best investment apps for beginners to choose where to open your account.