📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is net worth? Net worth is the total value of everything you own minus everything you owe — it is the single most complete snapshot of your financial health. Understanding what is net worth matters because it is the number that tells you whether you are building wealth or falling behind, regardless of how much you earn. This complete guide on what is net worth explains how to calculate it, what yours means right now, how it compares to others your age, and exactly how to grow it year after year in 2026.

What Is Net Worth — The Simple Formula

What is net worth in simple terms? Net worth equals your total assets minus your total liabilities:

Net Worth = Total Assets – Total Liabilities

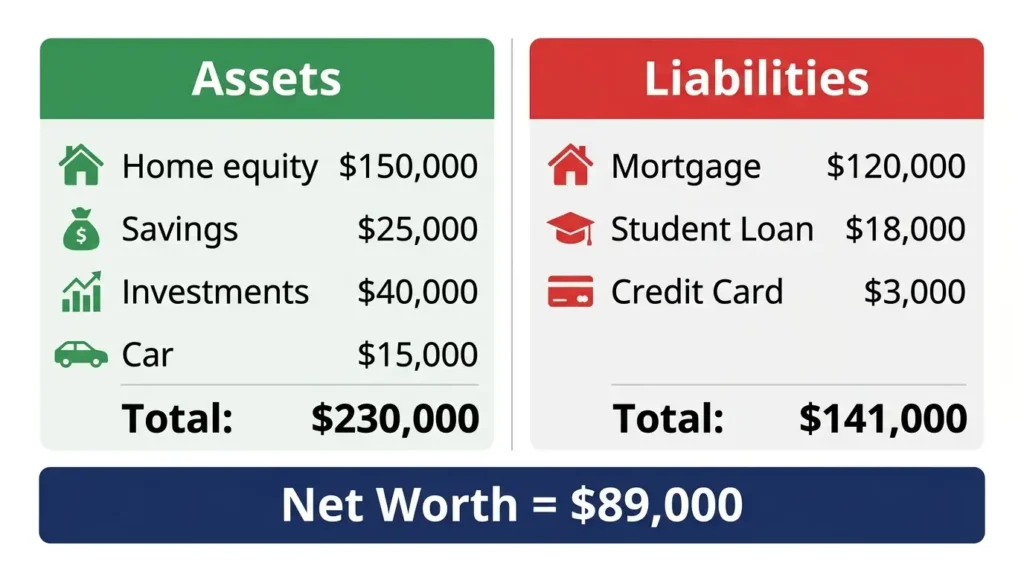

- If your assets total $200,000 and your liabilities total $80,000, your net worth is $120,000

- If your assets total $50,000 and your liabilities total $75,000, your net worth is -$25,000 (negative)

A positive net worth means you own more than you owe. A negative net worth means you owe more than you own — which is common for young adults with student loans and no savings. What matters is not where your net worth is today, but the direction it is moving over time.

What Are Assets and Liabilities?

To calculate what is net worth for yourself, you need to list both your assets and your liabilities accurately.

Assets — What You Own

Assets are everything you own that has monetary value:

- Cash and bank accounts (checking, savings, money market)

- Investment accounts (brokerage, Roth IRA, 401(k), index funds)

- Home equity (current market value of your home minus the mortgage balance)

- Vehicle value (current market value, not what you paid)

- Other real estate equity

- Business ownership value

- Valuable personal property (jewelry, collectibles, equipment)

Liabilities — What You Owe

Liabilities are all debts and financial obligations you currently owe:

- Mortgage balance (remaining amount owed on your home loan)

- Auto loan balance

- Student loan balance

- Credit card balances

- Personal loan balances

- Medical debt

- Any other money you owe to others

How to Calculate Your Net Worth Step by Step

Calculating what is net worth for your personal situation takes about 30 minutes. Here is the process:

- List every asset and its current value — check account balances, look up your home value, check your car’s current market value

- Add all asset values together to get your Total Assets

- List every liability and its current balance — check loan statements, credit card balances, and any other debts

- Add all liability balances together to get your Total Liabilities

- Subtract Total Liabilities from Total Assets — the result is your net worth

| Asset | Value | Liability | Balance |

|---|---|---|---|

| Checking account | $3,500 | Credit card debt | $4,200 |

| Savings account | $12,000 | Student loan | $22,000 |

| 401(k) balance | $18,000 | Auto loan | $8,500 |

| Roth IRA | $9,000 | Personal loan | $0 |

| Car value | $14,000 | Mortgage | $0 |

| Total Assets | $56,500 | Total Liabilities | $34,700 |

| Net Worth = $56,500 – $34,700 = $21,800 | |||

Update your net worth calculation every 3–6 months to track your progress. Most people find that simply tracking net worth regularly motivates them to make better financial decisions — because they can see the number moving in real time.

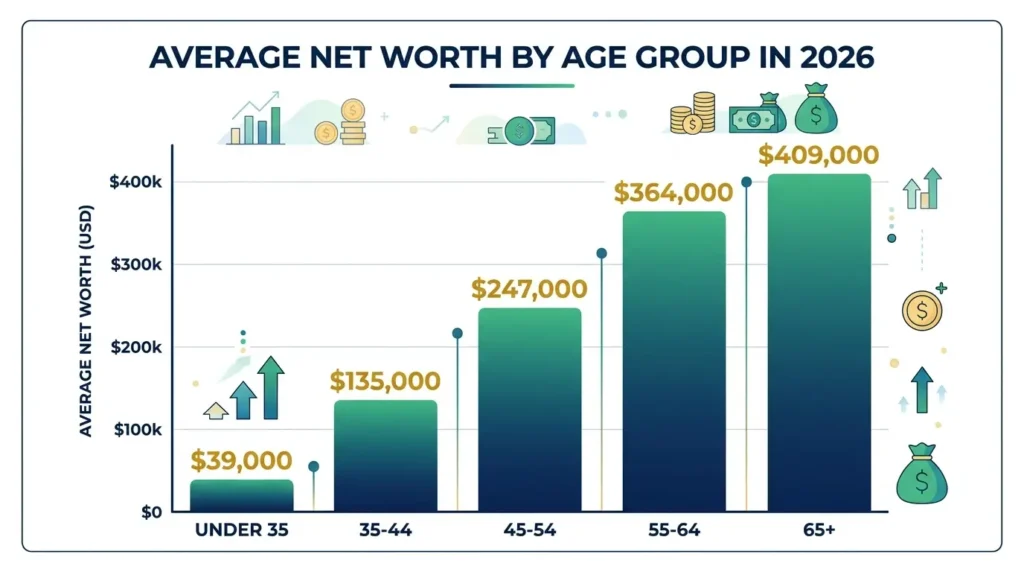

Average Net Worth by Age in 2026

One of the most common questions after learning what is net worth is: how does mine compare? Here are the average and median net worth figures by age group in the United States for 2026, based on Federal Reserve data:

| Age Group | Average Net Worth | Median Net Worth |

|---|---|---|

| Under 35 | $76,000 | $13,000 |

| 35–44 | $436,000 | $91,000 |

| 45–54 | $833,000 | $168,000 |

| 55–64 | $1,175,000 | $213,000 |

| 65–74 | $1,217,000 | $266,000 |

The median is more meaningful than the average because a small number of very wealthy individuals pulls the average up dramatically. The median represents the midpoint — half of Americans in each age group have more, and half have less. Do not compare your net worth to others as a measure of worth — use it as a personal progress tracker instead.

Is a Negative Net Worth Normal?

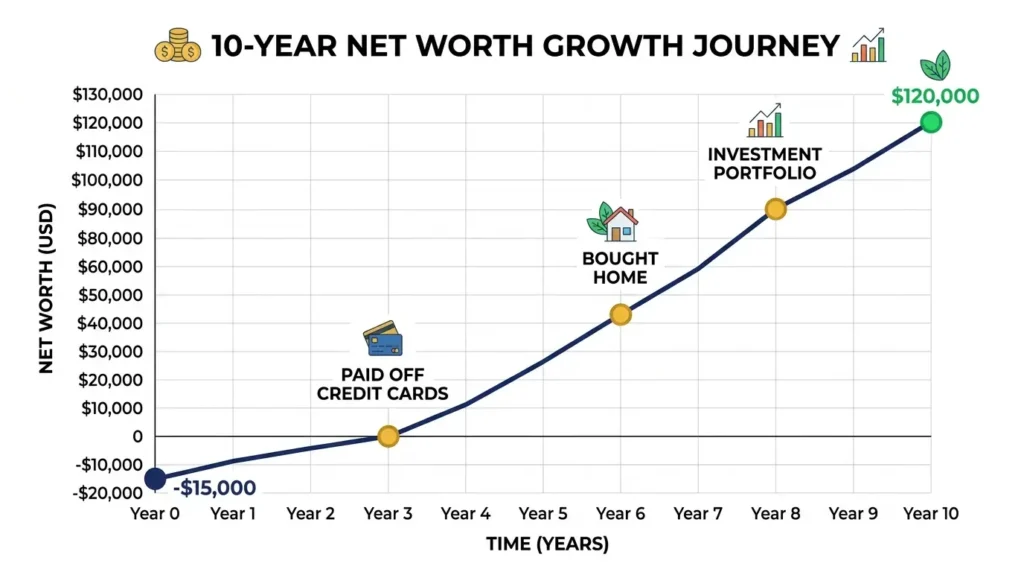

Yes — a negative net worth is extremely common, especially for people under 35. Student loans, car loans, and credit card debt often outweigh early savings and small asset values. A negative net worth does not mean you are failing — it means you are in the early stages of building wealth. The goal is to move the number upward every year.

The fastest ways to move from a negative to a positive net worth are: paying off high-interest debt aggressively, and building savings simultaneously. Even a $1,000 emergency fund and one less credit card balance can shift your net worth meaningfully. Read our guide on how to get out of credit card debt for the fastest debt elimination strategy.

How to Grow Your Net Worth

Once you understand what is net worth and where yours stands, the next step is growing it consistently. There are only two ways to increase net worth: increase assets or decrease liabilities. Here are the most effective strategies for both:

Increase Your Assets

- Invest consistently every month in index funds through a Roth IRA or 401(k). Read our guide on what a Roth IRA is to open one today.

- Build an emergency fund in a high-yield savings account — cash savings count as an asset. See our guide on how to build an emergency fund.

- Build home equity by making mortgage payments and allowing property values to appreciate over time

- Use dollar-cost averaging to invest consistently regardless of market conditions — read our guide on dollar-cost averaging

Decrease Your Liabilities

- Pay off high-interest debt first — credit cards at 20%+ APR destroy net worth faster than almost anything else

- Make extra payments on student loans to reduce the balance and the total interest paid

- Avoid taking on new debt for discretionary spending — every new liability directly reduces your net worth

- Refinance high-rate loans to lower interest rates when possible

Increase Your Income

Growing your income is the fastest multiplier for net worth growth. Every extra dollar earned that goes toward savings or debt repayment has a double effect — it increases assets and decreases liabilities simultaneously. Ask for raises, develop higher-value skills, and consider side income that can be directed entirely toward net worth growth. A solid budget helps you direct every income increase toward net worth improvement. Read our guide on how to make a budget to ensure every dollar has a plan.

How Often Should You Calculate Your Net Worth?

Calculate your net worth every 3–6 months. Quarterly reviews give you enough time to see meaningful progress without the noise of daily market fluctuations. Many people use the first day of each new quarter — January 1, April 1, July 1, October 1 — as their net worth calculation date.

Track it in a simple spreadsheet or notes app. Write down the date and total net worth each time. Over years, this becomes one of the most motivating financial records you own — a visual proof that your decisions and habits are building wealth. For a complete retirement-focused net worth strategy, read our guide on saving for retirement at 25.

Frequently Asked Questions

What is net worth and how do you calculate it?

Net worth is the total value of everything you own minus everything you owe. To calculate what is net worth for yourself, add up all your assets (cash, savings, investments, home equity, vehicle value) and subtract all your liabilities (mortgage, car loan, student loan, credit card balances). The result — positive or negative — is your net worth.

What is a good net worth by age?

A commonly cited target is to have net worth equal to your annual salary by age 30, three times your salary by 40, and six to seven times your salary by 60. However, the median net worth for Americans under 35 is approximately $13,000 — so many people are starting from a negative or very low number. Focus on the direction of growth rather than comparing to benchmarks.

Is it possible to have a negative net worth?

Yes, and it is very common — especially among people under 35 with student loans, car loans, or credit card debt that exceeds their savings and asset values. A negative net worth is a starting point, not a permanent condition. Consistent debt repayment and savings growth will move it upward over time.

Does your home count in net worth?

Yes — but only the equity portion. If your home is worth $300,000 and you owe $220,000 on the mortgage, your home contributes $80,000 to your net worth (not $300,000). As you make mortgage payments and the home value appreciates, the equity — and your net worth — grows automatically.

What is the fastest way to increase net worth?

The fastest ways to increase net worth are: paying off high-interest debt (which immediately reduces liabilities), investing consistently in index funds (which grows assets through compound interest), and increasing income while directing all extra earnings toward savings or debt repayment. All three simultaneously create the fastest net worth growth.

Final Thoughts: What Is Net Worth and Why You Should Track It

What is net worth? It is the most honest measure of your financial progress — more meaningful than your salary, your credit score, or the balance of any single account. Your net worth tells the full story: every asset you have built, every debt you still owe, and the gap between the two. Knowing what is net worth and tracking it regularly is what separates people who build wealth intentionally from those who wonder where their money went.

Calculate your net worth today — it takes 30 minutes and gives you a financial baseline that no other metric can provide. Then pick one action that increases it: open a Roth IRA, make an extra debt payment, or build your emergency fund. Every step moves the number in the right direction.