📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

What is a FICO score? A FICO score is the most widely used credit score model in the United States — a three-digit number between 300 and 850 that lenders use to evaluate how likely you are to repay a loan. Understanding what is a FICO score is essential because your FICO score directly determines the interest rates you qualify for, whether you get approved for a mortgage or car loan, and even whether a landlord will rent to you. This complete guide on what is a FICO score explains how it works, what each range means, and exactly how to improve yours in 2026.

What Is a FICO Score — The Simple Definition

A FICO score is a credit score created by the Fair Isaac Corporation — hence the name FICO. It was first introduced in 1989 and has since become the standard credit scoring model used by over 90% of top lenders in the United States. When a bank, mortgage company, car dealer, or credit card issuer checks your credit, they are almost certainly looking at your FICO score.

Your FICO score is calculated from the information in your credit reports at the three major credit bureaus: Equifax, Experian, and TransUnion. Because each bureau may have slightly different information, you technically have three FICO scores — one from each bureau. Lenders typically pull one or all three depending on the type of loan. To understand what goes into your credit reports in the first place, read our guide on what a credit score is.

What Factors Make Up a FICO Score?

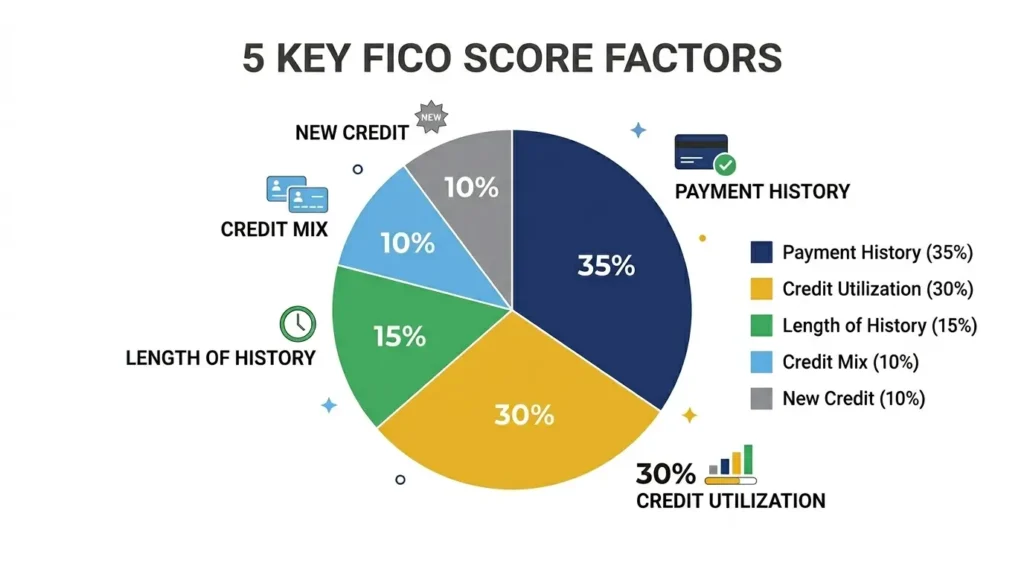

Your FICO score is calculated from five factors, each weighted differently. Understanding these factors is the key to understanding what is a FICO score and how to improve it:

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | Whether you pay bills on time every month |

| Credit Utilization | 30% | How much of your available credit you are using |

| Length of Credit History | 15% | How long your accounts have been open |

| Credit Mix | 10% | Variety of account types (cards, loans, mortgage) |

| New Credit | 10% | Recent credit applications and hard inquiries |

Payment history (35%) and credit utilization (30%) together make up 65% of your FICO score. This means the two most powerful things you can do to improve your FICO score are: pay every bill on time, every month — and keep your credit card balances below 30% of your limits.

FICO Score Ranges Explained

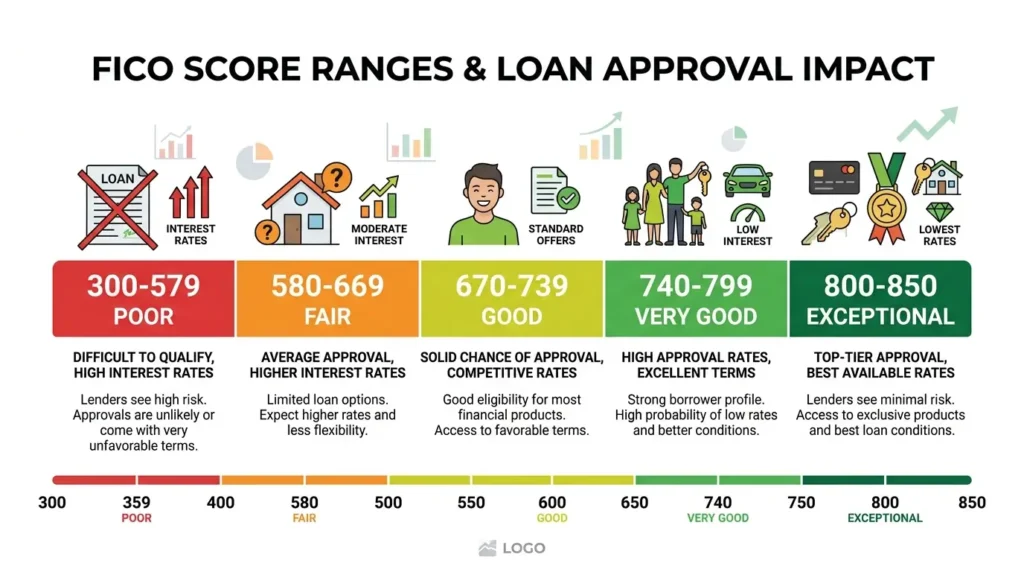

A FICO score ranges from 300 to 850. Here is what each range means in practice and how lenders typically respond:

| FICO Score Range | Rating | What It Means |

|---|---|---|

| 800–850 | Exceptional | Best rates on all products — elite tier |

| 740–799 | Very Good | Better-than-average rates, easy approvals |

| 670–739 | Good | Most lenders approve, decent rates |

| 580–669 | Fair | Some approvals, higher interest rates |

| 300–579 | Poor | Very few approvals, highest rates or denied |

The difference between a FICO score of 620 and 760 on a $300,000 mortgage can mean $100,000+ in additional interest paid over 30 years. A FICO score is not just a number — it is one of the most financially significant numbers in your life.

FICO Score vs Credit Score: Is There a Difference?

Many people use the terms interchangeably, but there is a technical distinction. A credit score is any score calculated from your credit report — there are many scoring models. A FICO score is specifically the score created by the Fair Isaac Corporation. Other scoring models include VantageScore, which is also commonly used.

For most practical purposes, when a lender says they are checking your credit score, they mean your FICO score. When a free app shows you a credit score, it may be a VantageScore rather than a FICO score — which is why the number can look slightly different. Both are based on the same underlying credit report data, but the calculation formulas differ slightly.

How Your FICO Score Affects Your Financial Life

Your FICO score affects far more than just loan applications. Here is a full picture of where your FICO score matters:

- Mortgage loans — your FICO score determines your interest rate and whether you qualify at all

- Auto loans — a higher FICO score means significantly lower monthly payments on car financing

- Credit cards — premium rewards cards with the best benefits require a FICO score of 700+

- Personal loans — FICO score determines APR, which can range from 6% to 36% based on your score

- Apartment rentals — most landlords require a minimum FICO score of 620–680

- Insurance premiums — in most states, your FICO score affects your auto and home insurance rates

- Employment — some employers check credit reports as part of background checks

How to Improve Your FICO Score

Understanding what is a FICO score is only valuable if you use that knowledge to improve it. Here are the most impactful actions to raise your FICO score:

Pay Every Bill on Time

Payment history is 35% of your FICO score — the largest single factor. Set up autopay for at least the minimum payment on every account to ensure you never miss a due date. A single missed payment can drop your FICO score by 60–110 points and stays on your report for 7 years.

Lower Your Credit Utilization

Credit utilization — how much of your available credit you are using — is 30% of your FICO score. Keep balances below 30% of your limit on every card. Ideally, stay below 10% for the maximum positive impact. Paying down credit card debt is one of the fastest ways to improve your FICO score. Read our complete strategy in our guide on how to improve your credit score.

Do Not Close Old Accounts

Length of credit history is 15% of your FICO score. Closing an old credit card shortens your average account age and reduces your total available credit — both of which hurt your FICO score. Keep old accounts open even if you rarely use them. Make one small purchase per month and pay it off to keep the account active.

Limit Hard Inquiries

Every time you apply for new credit, a hard inquiry appears on your report and can lower your FICO score by 5–10 points. Avoid applying for multiple credit products in a short period. If you are shopping for a mortgage or auto loan, multiple inquiries within a 14–45 day window are typically treated as one inquiry by FICO models.

How to Check Your FICO Score for Free

Many people do not know their FICO score — or pay for something they can get for free. Here are the best ways to check your FICO score at no cost:

- Credit card issuer app — many major card issuers (Discover, Citi, Chase, Capital One) show your FICO score for free in their mobile app

- Bank or credit union — some banks display your FICO score in online banking at no charge

- Credit monitoring apps — free services provide your credit score updated monthly, with alerts for changes

Checking your own FICO score is a soft inquiry and does not affect your score in any way. You should check your FICO score at least once per month to monitor your progress. If you are building credit from zero, read our guide on how to build credit from scratch for the complete beginner roadmap.

FICO Score Quick Reference Guide

| Action | FICO Score Impact | Time to See Results |

|---|---|---|

| Pay down credit card balance | +20 to +50 points | 30–45 days |

| Dispute and fix a credit error | +25 to +100 points | 30–60 days |

| Lower utilization below 10% | +30 to +60 points | 30–45 days |

| Become authorized user | +20 to +50 points | 30–60 days |

| 6 months of on-time payments | +40 to +80 points | 6 months |

| Miss one payment | -60 to -110 points | Immediate |

Frequently Asked Questions

What is a FICO score and why does it matter?

A FICO score is a three-digit credit score between 300 and 850 created by the Fair Isaac Corporation and used by over 90% of top US lenders. It determines whether you get approved for loans, credit cards, and apartments — and at what interest rate. A higher FICO score means lower borrowing costs and more financial opportunities throughout your life.

What is a good FICO score in 2026?

A good FICO score in 2026 is 670 or above. A score of 670–739 is considered Good and qualifies for most loans at reasonable rates. A Very Good score of 740–799 unlocks the best rates available. An Exceptional score of 800+ gives you access to the lowest interest rates on every financial product.

What is the difference between a FICO score and a credit score?

A credit score is any score calculated from your credit report. A FICO score is specifically the score made by the Fair Isaac Corporation, which is the most widely used model by lenders. VantageScore is another common credit score model. Both use the same underlying credit report data but calculate scores slightly differently.

How fast can I improve my FICO score?

Some improvements happen within 30–45 days — paying down a credit card balance or disputing a credit error can raise your FICO score quickly. Significant improvements of 60+ points typically take 6–12 months of consistent on-time payments and low utilization. Building from a poor FICO score to a good one generally takes 12–24 months.

Does checking my FICO score hurt it?

No. Checking your own FICO score is a soft inquiry and has zero impact on your score. Only hard inquiries — when a lender checks your credit to make a lending decision — can temporarily lower your FICO score. You should check your FICO score regularly to track progress and spot errors.

Final Thoughts: Your FICO Score Is a Financial Tool

Now that you understand what is a FICO score, you have the knowledge to take control of this crucial number. Your FICO score is not fixed — it changes every month based on your financial behavior. Pay on time, keep utilization low, avoid unnecessary hard inquiries, and monitor your score monthly. Over time, these simple habits will push your FICO score into the Very Good or Exceptional range and save you thousands of dollars in interest across every loan you take in your lifetime.

If you are starting from a low FICO score, read our step-by-step guide on how to improve your credit score. And if you have no credit history yet, our guide on how to get your first credit card is the best place to begin building your FICO score from scratch.

Copy tout