📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

The best high-yield savings accounts 2026 offer APYs that are 10 to 15 times higher than the national average — and choosing the right one can mean hundreds of dollars in extra interest every year. Whether you’re building an emergency fund, saving for a major purchase, or simply tired of watching your money earn next to nothing, this guide breaks down the top best high-yield savings accounts 2026 has to offer and explains exactly what to look for before you open one.

What Is a High-Yield Savings Account?

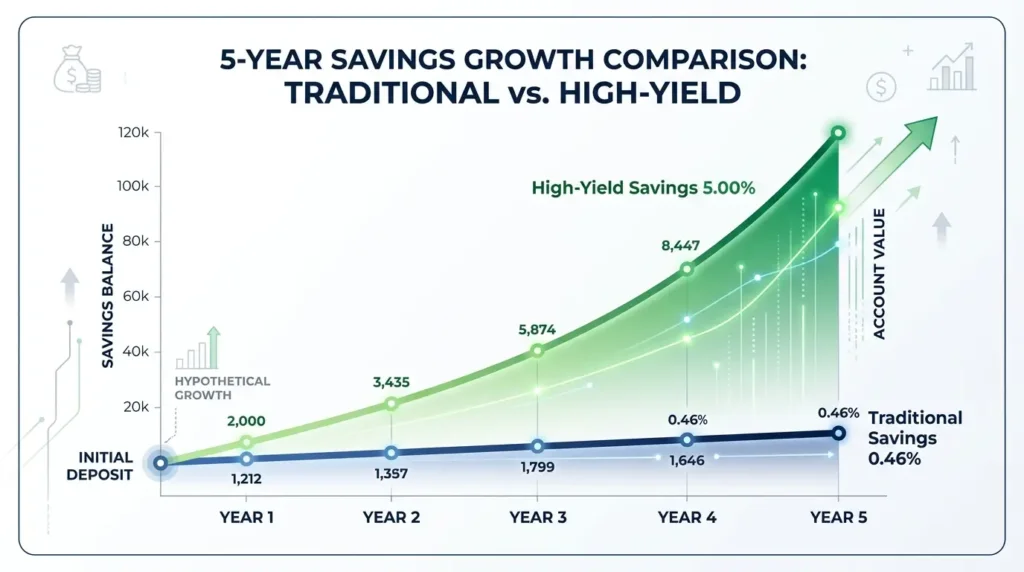

A high-yield savings account (HYSA) is a federally insured savings account that pays a significantly higher annual percentage yield (APY) than a standard savings account. While the national average APY at traditional banks hovers around 0.46%, top HYSAs in 2026 are offering rates between 4.50% and 5.25%. The difference adds up quickly: on a $10,000 balance, that gap represents over $400 in additional interest per year.

Most high-yield savings accounts are offered by online banks, which have lower overhead costs than brick-and-mortar institutions — and pass those savings on to customers in the form of higher rates. All reputable HYSAs are FDIC-insured up to $250,000 per depositor, making them just as safe as any traditional bank account. To understand exactly how APY works and how your interest compounds, read our guide on what APY means in savings accounts.

Best High-Yield Savings Accounts 2026: Our Top Picks

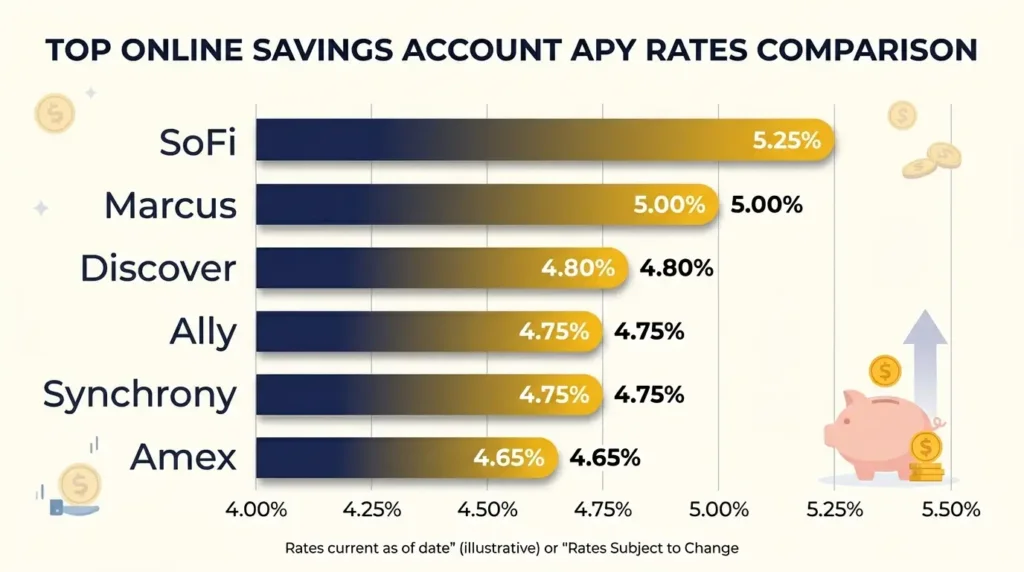

Here are the best high-yield savings accounts 2026 has available to U.S. residents, selected based on APY, fees, minimum balance requirements, accessibility, and overall value.

1. Marcus by Goldman Sachs — Best Overall

Marcus by Goldman Sachs consistently ranks at the top for its combination of a competitive APY, zero fees, and a trusted brand name. There’s no minimum balance requirement to open an account or earn the full APY, making it accessible for savers at any income level.

- APY: Up to 5.00%

- Minimum deposit: $0

- Monthly fees: None

- FDIC insured: Yes

- Best for: Savers who want a reliable, no-fuss account from a major institution

2. Ally Bank Online Savings — Best for Budgeting Tools

Ally Bank is one of the most popular online banks in the U.S., and its HYSA stands out for its built-in “buckets” feature — a savings organization tool that lets you separate money into labeled sub-accounts (emergency fund, vacation, new car) without opening multiple accounts.

- APY: Up to 4.75%

- Minimum deposit: $0

- Monthly fees: None

- FDIC insured: Yes

- Best for: Goal-based savers who want visual savings organization

3. SoFi High-Yield Savings — Best APY with Direct Deposit

SoFi offers one of the highest APYs in the best high-yield savings accounts 2026 lineup — but only when you set up direct deposit or maintain a qualifying balance. If you get paid via direct deposit, this account can be extremely lucrative.

- APY: Up to 5.25% (with direct deposit)

- Minimum deposit: $0

- Monthly fees: None

- FDIC insured: Yes (up to $2M through partner banks)

- Best for: People who use direct deposit and want the highest possible APY

4. Discover Online Savings — Best for Customer Service

Discover’s online savings account pairs a solid APY with 24/7 U.S.-based customer support. There are no fees of any kind — no monthly fee, no insufficient funds fee, no excessive withdrawal fee.

- APY: Up to 4.80%

- Minimum deposit: $0

- Monthly fees: None

- FDIC insured: Yes

- Best for: Savers who value customer service and a fully fee-free experience

5. American Express High-Yield Savings — Best for Amex Customers

The American Express HYSA offers a competitive rate with the trust of one of the most recognized financial brands in the world. It doesn’t come with a debit card — withdrawals are transfers to a linked bank account — which actually helps some savers resist dipping into their fund.

- APY: Up to 4.65%

- Minimum deposit: $0

- Monthly fees: None

- FDIC insured: Yes

- Best for: Existing Amex cardholders wanting to consolidate their financial relationship

6. Synchrony High-Yield Savings — Best ATM Access

Synchrony stands out because it offers an optional ATM card — giving you cash access when you need it while still earning a competitive rate. It also reimburses ATM fees charged by other networks.

- APY: Up to 4.75%

- Minimum deposit: $0

- Monthly fees: None

- FDIC insured: Yes

- Best for: Savers who want occasional ATM access without sacrificing a high APY

Best High-Yield Savings Accounts 2026: Side-by-Side Comparison

Here is how the best high-yield savings accounts 2026 compare side by side across the most important criteria:

| Bank | APY (2026) | Min. Deposit | Monthly Fee | ATM Card | FDIC Insured |

|---|---|---|---|---|---|

| Marcus by Goldman Sachs | Up to 5.00% | $0 | None | No | Yes |

| Ally Bank | Up to 4.75% | $0 | None | No | Yes |

| SoFi (with direct deposit) | Up to 5.25% | $0 | None | No | Yes (up to $2M) |

| Discover Online Savings | Up to 4.80% | $0 | None | No | Yes |

| American Express HYSA | Up to 4.65% | $0 | None | No | Yes |

| Synchrony HYSA | Up to 4.75% | $0 | None | Yes | Yes |

Note: APY rates are subject to change. Always verify current rates directly on the bank’s official website before opening an account.

What to Look for in a High-Yield Savings Account

APY — Read the Fine Print

Some banks advertise a high APY that only applies under specific conditions — setting up direct deposit, maintaining a minimum balance, or making a certain number of monthly transactions. Always check whether the rate is unconditional. An unconditional 4.75% APY may be worth more than a conditional 5.25% you don’t consistently qualify for.

Zero Monthly Fees

Every dollar in fees is a dollar that doesn’t compound. The best HYSAs charge absolutely no monthly maintenance fees. Avoid any account with fees you can’t easily waive.

No Minimum Balance Requirement

Most top HYSAs have no minimum deposit to open and no minimum balance to earn the full APY. This is especially important for beginners building their savings from scratch.

FDIC Insurance

Always verify that any savings account you open is FDIC-insured. This protects your deposits up to $250,000 per depositor, per institution. If a bank fails, your money is guaranteed. Never open a savings account at an institution that isn’t FDIC-insured.

Transfer Speed and App Quality

Since most HYSAs are at online banks, you’ll move money via electronic transfer. Look for fast transfer speeds — same-day or next-day to linked accounts — and a clean mobile app experience. Transfers that take 3–5 business days can be inconvenient in a real emergency.

How Much Interest Can You Actually Earn?

Here’s how much interest a balance would earn over one year at different APY levels:

| APY Rate | Interest on $5,000 | Interest on $10,000 | Interest on $25,000 |

|---|---|---|---|

| 0.46% (national avg.) | $23 | $46 | $115 |

| 4.65% (Amex) | $232 | $465 | $1,162 |

| 4.75% (Ally / Synchrony) | $237 | $475 | $1,187 |

| 4.80% (Discover) | $240 | $480 | $1,200 |

| 5.00% (Marcus) | $250 | $500 | $1,250 |

| 5.25% (SoFi w/ DD) | $262 | $525 | $1,312 |

The difference between leaving money in a traditional savings account and one of the best high-yield savings accounts 2026 offers amounts to $400–$1,200+ per year on a $10,000–$25,000 balance.

How to Open a High-Yield Savings Account

Opening a high-yield savings account is straightforward and takes 5–10 minutes online. Here’s the general process:

- Choose your account — use the comparison table above to pick the best fit for your needs

- Visit the bank’s official website — never open an account through a third-party link you don’t trust

- Provide your personal information — name, address, Social Security number, date of birth, and a government-issued ID

- Link your existing bank account — you’ll need routing and account numbers to fund the new account

- Make an initial deposit — most top HYSAs require $0 minimum, but even a small first transfer gets you started

- Set up automatic transfers — schedule recurring deposits from your checking account on payday

For a full step-by-step walkthrough including what documents you’ll need, see our guide on how to open a bank account online.

Is a High-Yield Savings Account Right for You?

A HYSA is the right move if any of these apply to you:

- You want to earn more on your existing savings without taking on any risk

- You’re building or maintaining an emergency fund — read our guide on how to build an emergency fund

- You have a short-term savings goal (vacation, down payment, car) within 1–3 years

- You’re tired of earning virtually nothing at your current bank

- You want a separate, harder-to-access account to avoid impulse spending

A HYSA is not a replacement for long-term investing. If your goal is retirement wealth-building, check our guide on what a 401(k) is. Use your HYSA for safe, accessible savings — and invest separately for long-term growth through a Roth IRA.

Frequently Asked Questions

What is the best high-yield savings account in 2026?

The best high-yield savings accounts 2026 depend on your needs. SoFi offers the highest APY (up to 5.25%) with direct deposit. Marcus by Goldman Sachs offers up to 5.00% with no conditions. Ally Bank stands out for its savings buckets feature. All are FDIC-insured with no monthly fees or minimum balance requirements.

Are high-yield savings accounts safe?

Yes. All reputable high-yield savings accounts are FDIC-insured up to $250,000 per depositor, per institution. Your money is fully protected even if the bank fails. Never open a savings account at an institution that isn’t FDIC-insured.

Can I lose money in a high-yield savings account?

No. Unlike stocks or ETFs, a high-yield savings account carries no market risk. Your principal is safe and FDIC-insured. The only way your balance decreases is if you withdraw money or pay fees — which is why choosing a no-fee account is important.

How often do high-yield savings account rates change?

HYSA rates are variable and typically move in response to Federal Reserve interest rate decisions. When the Fed raises rates, HYSA APYs tend to increase. When the Fed cuts rates, APYs typically decrease. Most banks adjust their rates within days of a Fed rate change.

Is interest from a high-yield savings account taxable?

Yes. Interest earned in a high-yield savings account is considered ordinary income and is taxable at the federal level. Your bank will send you a 1099-INT form at tax time if you earned $10 or more in interest during the year.

Final Thoughts: Stop Leaving Money on the Table

If your savings are sitting in a traditional bank account earning 0.01%–0.50% APY, you’re leaving hundreds — or even thousands — of dollars in potential interest on the table every year. The best high-yield savings accounts 2026 makes available are easy to open, charge no fees, require no minimum balance, and carry zero risk. Switching takes less than 10 minutes.

Once your savings are earning more, make sure they’re working toward a clear goal. Start with our guide on how to build an emergency fund — the foundation of any strong financial plan. And if you follow the 50/30/20 budget rule, a high-yield savings account is the natural home for your 20% savings allocation.