📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to set financial goals is one of the most foundational skills in personal finance — because without clear, written goals, your financial decisions are random and your progress is invisible. Learning how to set financial goals transforms money management from a stressful reaction to life’s demands into a deliberate, structured pursuit of what matters most to you. This complete guide on how to set financial goals walks you through the SMART goal framework, the right categories of goals to set, and exactly how to turn a vague wish into a specific plan with monthly action steps in 2026.

Why Setting Financial Goals Changes Everything

People who set clear financial goals consistently build more wealth, carry less debt, and report less financial anxiety than those who manage money without goals. The reason is simple: a goal gives every dollar a purpose. Without a goal, extra money disappears into discretionary spending. With a goal, the same extra money goes to a specific, meaningful target — an emergency fund, a vacation, a down payment, early retirement.

Setting financial goals also creates accountability. When you write down “save $12,000 for a down payment by December 2026,” you can measure your progress every month. That measurement is what separates people who achieve financial milestones from those who remain permanently busy but never seem to get ahead. For the complete framework that connects financial goals to a full money system, read our guide on how to create a financial plan.

How to Set Financial Goals the SMART Way

The most reliable framework for how to set financial goals is the SMART method. SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound. Every effective financial goal should meet all five criteria:

- Specific — the goal states exactly what you want to accomplish, not a vague wish. “Save more money” is not specific. “Save $8,000 in a high-yield savings account” is specific.

- Measurable — you can track progress with a number. “$8,000” is measurable. “More savings” is not.

- Achievable — the goal is challenging but realistic given your income and expenses. Setting a goal to save $3,000/month on a $4,000/month take-home salary is not achievable.

- Relevant — the goal aligns with your values and priorities. If owning a home is important to you, a down payment savings goal is relevant. If it is not a priority, it is not.

- Time-bound — the goal has a specific deadline. “By December 31, 2026” creates urgency. “Someday” does not.

Example of a SMART financial goal: “I will save $10,000 in my high-yield savings account as a starter emergency fund by December 31, 2026, by automating $835 per month on payday.” This goal is specific ($10,000), measurable (track monthly), achievable (based on income), relevant (safety net), and time-bound (end of 2026).

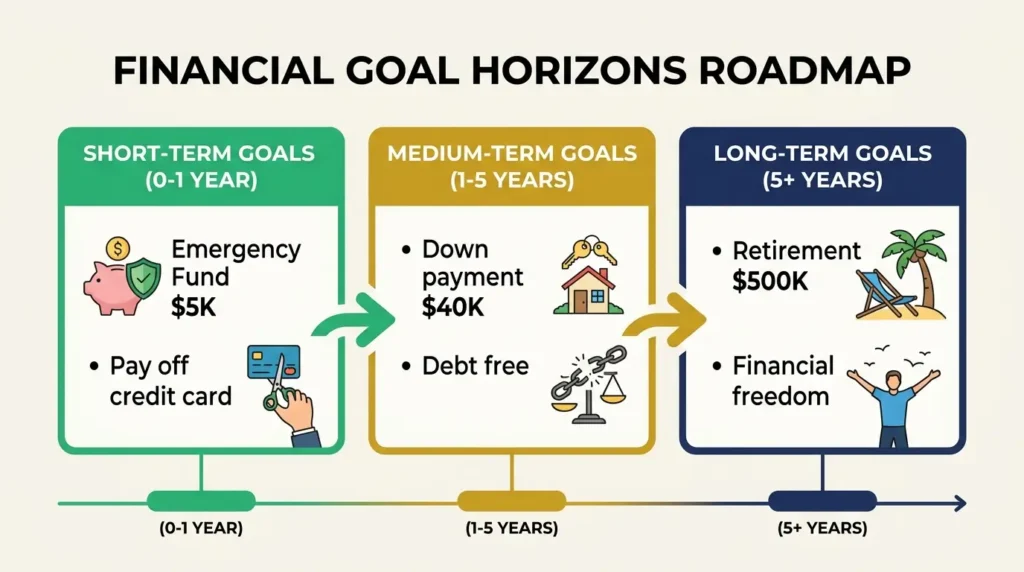

Types of Financial Goals by Time Horizon

When learning how to set financial goals, organizing them by time horizon helps you prioritize and sequence your efforts. Here is how to set financial goals across all three timeframes:

Short-Term Financial Goals (0–12 Months)

Short-term financial goals are urgent, foundational, or motivational wins that create the stability needed for longer-term goals. Examples:

- Build a $1,000 starter emergency fund by [specific month]

- Pay off [specific credit card] by [specific date]

- Open a Roth IRA and make the first contribution

- Reduce monthly restaurant spending from $400 to $200

- Increase your savings rate from 5% to 10% of income

Medium-Term Financial Goals (1–5 Years)

Medium-term financial goals require sustained effort over 1–5 years and typically represent major milestones. Examples:

- Build a full 6-month emergency fund ($15,000–$30,000 depending on expenses)

- Eliminate all non-mortgage debt

- Save a $40,000–$60,000 home down payment

- Reach $50,000 in investment accounts

- Increase your net worth to your annual salary by age 30

Long-Term Financial Goals (5+ Years)

Long-term financial goals define the life you are building toward. They require consistent action over years or decades. Examples:

- Retire at age [X] with [$ amount] in retirement accounts

- Build a $1,000,000 investment portfolio by age 60

- Own a home free and clear by age 55

- Reach a net worth of 25 times your annual expenses (financial independence)

- Build a college fund for your children through a 529 plan

Step-by-Step: How to Set Financial Goals That Stick

- Start with your values — ask yourself what financial security means to you, what experiences matter most, and what you are afraid of financially. Your goals should reflect these answers.

- Assess your current situation — calculate your net worth and monthly cash flow before setting goals. Read our guide on what is net worth to run your numbers.

- Set 1–3 goals per timeframe — too many goals compete for the same resources and momentum. Pick the most important one or two per category.

- Attach a dollar amount and date to every goal — “save money” becomes “save $500/month for 24 months to reach $12,000 by January 2027”

- Calculate the required monthly action — divide the goal amount by the number of months until the deadline

- Build the monthly amount into your budget — make the goal contribution automatic and non-negotiable. Read our guide on how to make a budget to build this into your system.

- Review progress quarterly — measure how close you are to each goal every three months and adjust if life changes

Financial Goals Examples: SMART vs Vague

| Vague Goal | SMART Financial Goal Version |

|---|---|

| “Save more money” | “Save $500/month automatically on payday, reaching $6,000 by December 31, 2026” |

| “Pay off debt” | “Pay $400/month extra toward my $8,000 credit card balance at 22% APR and eliminate it by April 2027” |

| “Invest for retirement” | “Contribute $625/month to my Roth IRA to max the $7,500 annual limit by December 31, 2026” |

| “Buy a house someday” | “Save $1,000/month in my HYSA to reach a $36,000 down payment by January 2029” |

| “Get my finances together” | “Build a $5,000 emergency fund, pay off my car loan, and open a Roth IRA by December 2026” |

How to Prioritize Competing Financial Goals

Most people have more financial goals than available money. When you cannot fund everything at once, use this priority order to set financial goals that build on each other:

| Priority | Financial Goal | Why First |

|---|---|---|

| 1 | $1,000 starter emergency fund | Prevents debt spiral from small surprises |

| 2 | 401(k) to full employer match | Guaranteed 50–100% return — never skip |

| 3 | Pay off high-interest debt | Guaranteed return = the interest rate |

| 4 | Full emergency fund (3–6 months) | Complete financial safety net |

| 5 | Max Roth IRA ($7,500/year) | Tax-free growth for decades |

| 6 | Other goals (house, college, travel) | Specific to your values and timeline |

Follow this order when setting and funding your financial goals. It is the same priority structure used in our guide on saving for retirement at 25 — a complete roadmap that shows how these goals compound over decades.

How to Track Your Financial Goals

Setting financial goals is only half the work. Tracking them consistently is what turns goals into achievements. Options for tracking financial goals:

- Spreadsheet — create a simple tab for each goal showing the target, current balance, monthly contribution, and projected completion date

- Budgeting app — apps like YNAB, Copilot, or PocketGuard allow you to set specific savings goals and track progress automatically

- Net worth tracker — updating your net worth quarterly shows overall progress across all goals simultaneously. Read our guide on what is net worth for the calculation method.

- Paper and pen — write goals on a card you see daily. The visibility alone increases follow-through significantly.

Review each financial goal at the end of every month. Did the automated transfer go through? Is the balance growing as planned? Are there any categories where you can redirect extra money? Monthly reviews take 15 minutes and dramatically improve goal achievement rates.

Frequently Asked Questions

What are good financial goals to set?

Good financial goals to set include: building a 3–6 month emergency fund, paying off all high-interest debt, maxing your Roth IRA each year, saving a home down payment, reaching 1x your salary in net worth by 30, and funding retirement to allow you to retire at your target age. The best goals are specific, time-bound, and directly tied to your values and life priorities.

What is the SMART framework for financial goals?

The SMART framework means every financial goal should be: Specific (exact dollar amount and what you will save for), Measurable (trackable monthly), Achievable (realistic given your income), Relevant (aligned with your values), and Time-bound (specific deadline). Instead of “save more money,” a SMART goal would be “save $500/month automatically to reach $6,000 by December 31, 2026.”

How many financial goals should I set at once?

Most people do best with 1–2 active goals per time horizon — one or two short-term goals, one or two medium-term goals, and one or two long-term goals. Having too many goals divides your resources and attention too thin, making all of them harder to achieve. Prioritize by the sequence of financial foundations (emergency fund first, then debt, then investing) before pursuing discretionary goals.

How do I set financial goals when I live paycheck to paycheck?

Start with one goal: save $1,000 as a starter emergency fund. Even $25–$50/month automated on payday creates forward momentum. Then focus on reducing one expense category to free up more monthly cash flow. Financial goals work at any income level — the initial amounts may be small, but the habit of goal-directed saving is what matters. As income grows, increase your goal contributions.

What is the difference between short-term and long-term financial goals?

Short-term financial goals are achievable within 12 months — building an emergency fund, paying off a credit card, or opening a retirement account. Long-term financial goals require 5 or more years of consistent effort — retiring comfortably, building a million-dollar investment portfolio, or owning a home outright. Both types are necessary: short-term goals build the foundation; long-term goals define the destination.

Final Thoughts: Set Financial Goals Today and Review Them Monthly

Knowing how to set financial goals is the skill that separates people who drift financially from people who build wealth deliberately. The process is not complicated: identify what matters to you, attach a specific dollar amount and deadline to each goal, automate monthly contributions, and review progress quarterly. That simple system — applied consistently — achieves more financial milestones than any complex strategy.

Start by setting one financial goal right now. Write it in the SMART format: what exactly, how much, by when, and how much per month. Then open your banking app and set up the automatic transfer. Financial goals set today compound into financial freedom tomorrow. Use our guide on the 50/30/20 budget rule to ensure your monthly budget has room for every goal you set.