📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

How to create a financial plan is one of the most powerful questions you can ask — because a financial plan is not just a budget or a savings goal. Learning how to create a financial plan means building a complete, written roadmap for every area of your financial life: income, spending, debt, savings, investing, and retirement. Most people navigate their finances without a plan and wonder why they never seem to get ahead. This complete guide on how to create a financial plan walks you through every step to build one yourself — no financial advisor required — in 2026.

What Is a Financial Plan and Why Do You Need One?

A financial plan is a written document that captures your current financial situation, your short- and long-term financial goals, and the specific steps you will take to reach each goal. It is the difference between drifting financially and moving with purpose. People who create a financial plan consistently accumulate more wealth, carry less debt, and report less financial stress than those who manage money reactively.

You do not need to be wealthy to create a financial plan — you need a financial plan to become wealthy. It is the map, not the destination. And unlike a plan created by a financial advisor that costs hundreds or thousands of dollars, a solid personal financial plan can be built entirely by yourself in a few hours using the steps in this guide.

What Does a Complete Financial Plan Include?

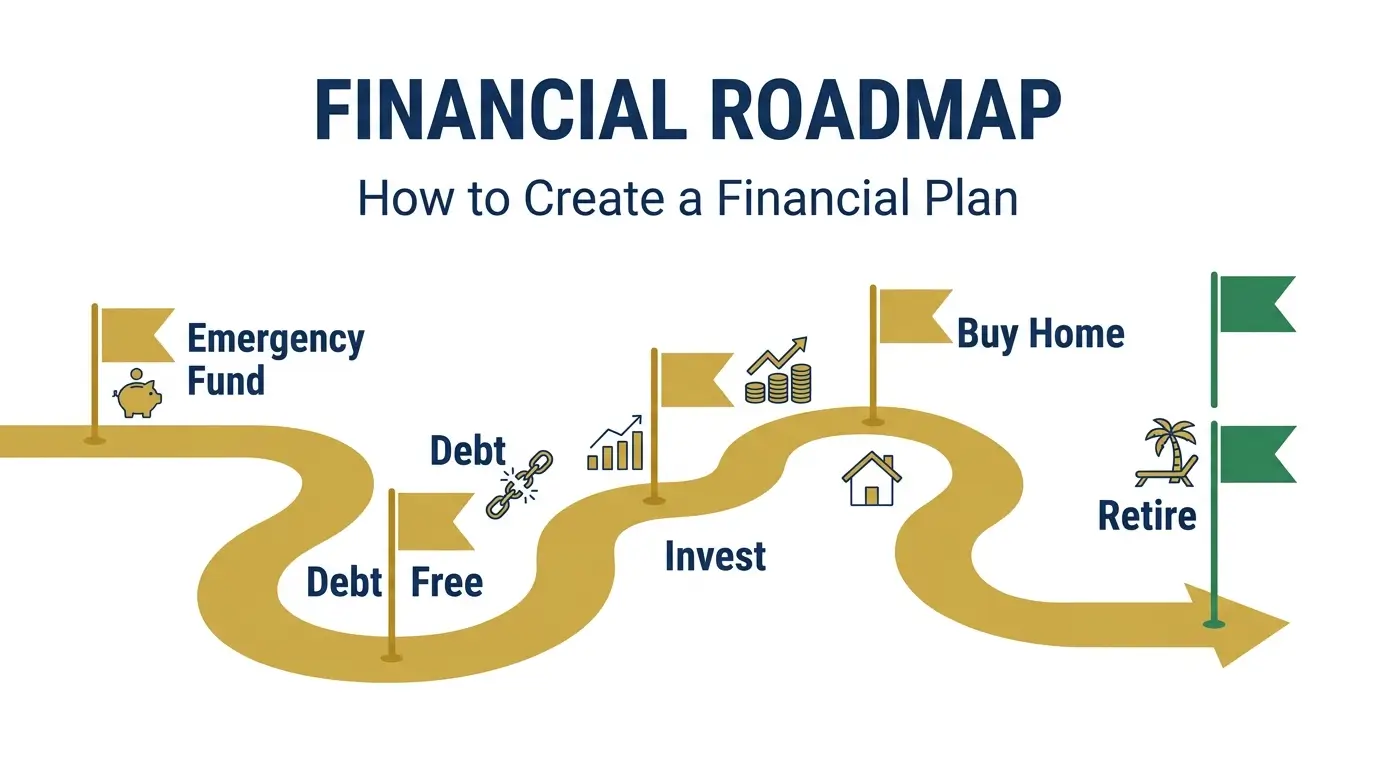

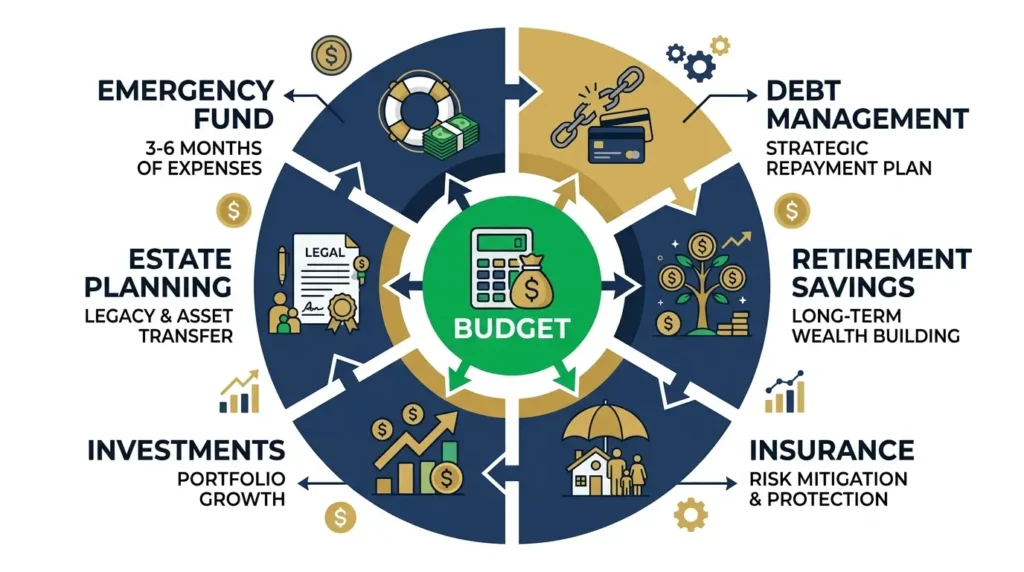

Before you create a financial plan, it helps to understand what it covers. A complete personal financial plan addresses seven areas:

- Budget — how much you earn, spend, and save each month

- Emergency fund — your cash safety net (3–6 months of expenses)

- Debt management — a strategy to eliminate all high-interest debt

- Retirement savings — 401(k), Roth IRA, and long-term investing

- Investment strategy — how your money grows outside of retirement accounts

- Insurance coverage — protection against life’s major financial risks

- Estate planning — ensuring your assets go where you want if something happens to you

Most beginners start with the first three — budget, emergency fund, and debt — and add the remaining components as their financial situation grows. That is exactly the right approach.

Step 1 — Assess Your Current Financial Situation

The first step to create a financial plan is total financial clarity — knowing exactly where you stand right now. This means calculating your net worth: everything you own minus everything you owe. Read our guide on what is net worth for the exact calculation method.

Gather the following information:

- Monthly take-home income (all sources)

- Monthly fixed expenses (rent, car payment, insurance, subscriptions)

- Monthly variable expenses (groceries, gas, dining, entertainment)

- All debt balances and interest rates (credit cards, student loans, car loans, mortgage)

- All savings and investment account balances

- Retirement account balances (401k, Roth IRA)

Many people discover significant surprises at this stage — forgotten subscriptions, underestimated spending, or more debt than they realized. This is the starting point, not a judgment. Write everything down.

Step 2 — Build Your Monthly Budget

Every financial plan is built on a budget. Without knowing what you earn and where every dollar goes, you cannot create a financial plan that actually works. A budget is not a restriction — it is the operating system of your entire financial plan.

The simplest framework to start with is the 50/30/20 budget rule: 50% of after-tax income to needs, 30% to wants, 20% to savings and debt repayment. For a complete step-by-step budget setup, read our guide on how to make a budget.

Step 3 — Set Clear Financial Goals

The heart of how to create a financial plan is defining what you are working toward. Vague goals — “save more money” or “pay off debt” — do not work. Specific, time-bound goals do. Organize your goals into three timeframes:

Short-Term Goals (0–12 months)

- Build a $1,000 starter emergency fund by [specific date]

- Pay off [specific credit card] by [specific date]

- Reduce monthly dining out spending by $150

- Open a Roth IRA and make the first contribution

Medium-Term Goals (1–5 years)

- Build a 6-month emergency fund ($15,000–$25,000)

- Eliminate all non-mortgage debt

- Save a $40,000 house down payment

- Reach a $50,000 investment portfolio

Long-Term Goals (5+ years)

- Retire at age [X] with [$ amount] in retirement accounts

- Reach a net worth of $500,000 by age 45

- Own a home free and clear by age 55

- Build a $1,000,000 investment portfolio by age 65

Write down each goal with a specific dollar amount and target date. Attach a monthly savings or payment amount to each one. Now your financial plan has structure — not just wishes.

Step 4 — Build Your Emergency Fund

No financial plan survives contact with real life without an emergency fund. Your emergency fund is the shock absorber that prevents one bad month — a car repair, a medical bill, a job loss — from destroying every other part of your financial plan. Start with $1,000, then build to 3–6 months of expenses.

Keep your emergency fund in a high-yield savings account earning 4%–5% APY — not in a checking account where it is too easy to spend. Read our complete guide on how to build an emergency fund for the full step-by-step system.

Step 5 — Create a Debt Elimination Strategy

High-interest debt is the greatest obstacle to building wealth in any financial plan. Your financial plan must include a specific, written strategy to eliminate all high-interest debt — and a timeline for doing it.

- List every debt with balance, interest rate, and minimum payment

- Choose a payoff method — avalanche (highest rate first) or snowball (smallest balance first)

- Calculate your payoff date for each debt

- Automate minimum payments on all debts

- Direct every extra dollar to the top debt on your list

Read our guide on how to get out of credit card debt for the complete debt elimination framework to include in your financial plan.

Step 6 — Build Your Retirement and Investment Strategy

Once your emergency fund is funded and high-interest debt is on a clear payoff path, your financial plan must address long-term wealth building. The order of operations:

| Priority | Action | 2026 Limit / Target |

|---|---|---|

| 1 | 401(k) to employer match | Never leave free money on the table |

| 2 | Max Roth IRA | $7,500/year |

| 3 | Max 401(k) | $24,500/year |

| 4 | Taxable brokerage | No limit |

Invest in low-cost index funds — S&P 500 ETFs or total market ETFs — inside every account. For the complete retirement savings strategy, read our guide on saving for retirement at 25.

Step 7 — Review and Update Your Financial Plan Quarterly

A financial plan is not a document you write once and file away. It is a living system that needs regular review to stay aligned with your life and goals. Here is the review schedule to build into your financial plan:

- Monthly — review your budget, check spending vs plan, update debt balances

- Quarterly — calculate your net worth, review goal progress, adjust contribution amounts

- Annually — review insurance coverage, update beneficiaries, assess whether goals need adjustment, review investment allocations

- After life events — marriage, children, job change, inheritance, or major purchase all require a financial plan update

Your One-Page Financial Plan Template

| Section | Your Information | Target / Date |

|---|---|---|

| Monthly net income | $________ | — |

| Monthly total expenses | $________ | Stay under income |

| Monthly savings rate | ____% | Target: 20%+ |

| Emergency fund balance | $________ | 3–6 months of expenses |

| Total high-interest debt | $________ | $0 by [date] |

| Retirement account balance | $________ | 1x salary by 30, 3x by 40 |

| Net worth | $________ | Growing every quarter |

| Top 3 financial goals | 1. ___ 2. ___ 3. ___ | With $ amounts and dates |

Print this template, fill it in, and put it somewhere you will see it monthly. The simple act of writing down your financial plan makes you significantly more likely to follow it.

Frequently Asked Questions

How do I create a financial plan for myself?

To create a financial plan for yourself, follow these steps: (1) calculate your net worth and current cash flow, (2) build a monthly budget, (3) set specific short, medium, and long-term financial goals with dollar amounts and dates, (4) build your emergency fund, (5) create a debt elimination strategy, (6) set up your retirement and investment accounts, and (7) review the plan quarterly. No financial advisor is required to create a solid personal financial plan.

What should a financial plan include?

A complete financial plan includes: a monthly budget, an emergency fund target and timeline, a debt elimination strategy, a retirement savings plan with specific accounts and contribution amounts, an investment strategy, insurance coverage review, and specific financial goals with target dates and dollar amounts. Most people start with the first three components and add the others over time.

How long does it take to create a financial plan?

A solid basic financial plan takes 2–4 hours to create from scratch — gathering financial data, building your budget, setting goals, and writing everything down. A comprehensive plan covering all seven areas may take 4–8 hours total. Once created, monthly reviews take 15–30 minutes and quarterly reviews take 1–2 hours.

Do I need a financial advisor to create a financial plan?

No — most people can create a solid personal financial plan entirely on their own using free tools and the steps in this guide. A fee-only financial advisor can add value for complex situations (significant estate, business ownership, complex taxes, approaching retirement), but for most Americans in their 20s through 40s, a self-created financial plan following proven frameworks is entirely sufficient.

How often should I update my financial plan?

Review your financial plan monthly for budget tracking, quarterly for net worth and goal progress, and annually for a full review of insurance, investments, and goal alignment. Update it immediately after any major life event — marriage, divorce, new child, job change, inheritance, or major purchase. A financial plan that is not reviewed regularly becomes irrelevant within 12–18 months.

Final Thoughts: Create a Financial Plan Today and Change Your Trajectory

Knowing how to create a financial plan is the single most comprehensive financial skill in this guide — because a financial plan brings together every other personal finance concept into one coherent system. It is not just a budget. It is not just a savings goal. When you create a financial plan, you build the complete roadmap for where you are going financially and exactly how you will get there.

Start with Step 1 today. Calculate your net worth. Build your budget. Write down three financial goals with specific dollar amounts and dates. That first hour of work creates the foundation that every subsequent financial decision will be built upon. Create a financial plan — and then work it, review it, and update it every quarter. Your financial future is not an accident — it is the result of the plan you create and follow today.