📢 Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. We only recommend products we genuinely believe in.

Zero-based budgeting is the budgeting method where every single dollar of your income is assigned a specific purpose — until your income minus your expenses equals exactly zero. Not because you’ve spent everything, but because every dollar has been deliberately allocated: to bills, groceries, savings, investments, or entertainment. Nothing is left unassigned and nothing is wasted.

In this complete guide, you’ll learn exactly what zero-based budgeting is, how it differs from traditional budgeting, how to set it up step by step, the best tools to use, and whether it’s the right approach for your financial situation. If you’re also curious about a simpler alternative, read our guide on the 50/30/20 budget rule to compare both approaches.

What Is Zero-Based Budgeting?

Zero-based budgeting (ZBB) is a budgeting method where you start from zero every month and assign every dollar of your income to a specific category — needs, wants, savings, or debt repayment — until the total reaches zero.

The formula is simple: Income − All Expenses = $0

This doesn’t mean you spend everything you earn. It means every dollar is intentionally accounted for. If you earn $4,000 per month, you decide in advance what every one of those 4,000 dollars will do — $1,200 for rent, $400 for groceries, $200 for utilities, $500 for savings, $300 for dining out, and so on — until all $4,000 is assigned.

The term “zero-based budgeting” was originally coined by accountant Pete Pyhrr in the 1970s as a business budgeting technique, but it was popularized for personal finance by Dave Ramsey and later by the budgeting app YNAB (You Need a Budget).

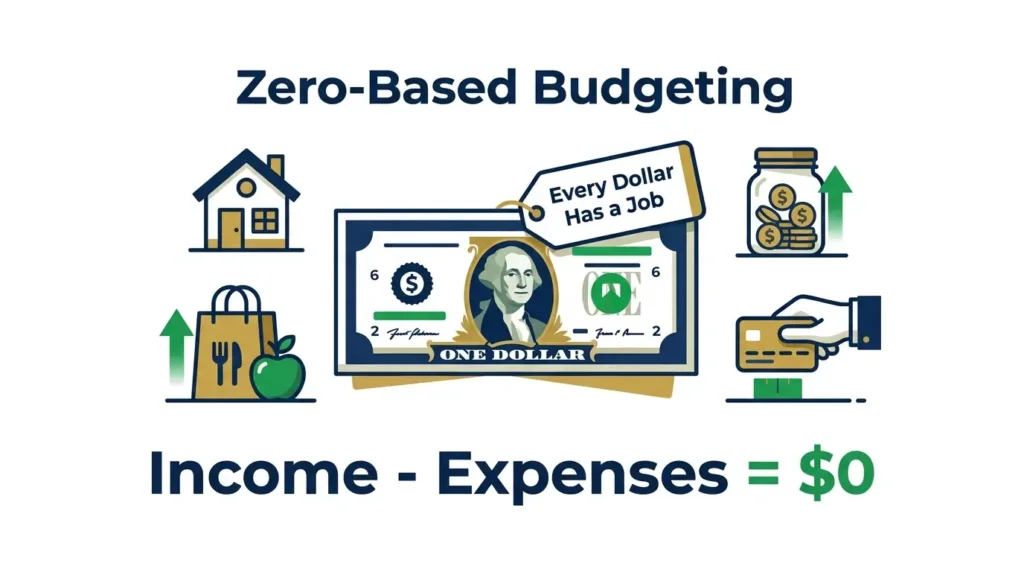

Zero-Based Budgeting vs Traditional Budgeting

Most people use a traditional approach to budgeting: they track what they spend and compare it to the previous month. Zero-based budgeting takes the opposite approach: you plan every expense before the month begins, rather than reviewing it after.

| Feature | Traditional Budgeting | Zero-Based Budgeting |

|---|---|---|

| Starting point | Last month’s spending | Zero — fresh start each month |

| Approach | Reactive (track after spending) | Proactive (plan before spending) |

| Every dollar assigned? | ❌ Leftover money often untracked | ✅ Every dollar has a job |

| Time required | Low — check occasionally | Medium — 30–60 min setup monthly |

| Control level | Moderate | Maximum |

| Best for | People who want low maintenance | People serious about goals or debt |

How Zero-Based Budgeting Works: Step by Step

Step 1: Calculate Your Monthly Income

Start with your total after-tax income for the month — everything that comes into your bank account. Include your salary, freelance income, side hustle earnings, and any other regular income. If your income varies, use the lowest month of the past three months as your baseline to budget conservatively.

Step 2: List All Your Expenses

Write down every expense you anticipate for the month. Organize them into categories:

- Fixed expenses: Rent/mortgage, car payment, insurance, subscriptions (same amount every month)

- Variable necessities: Groceries, utilities, gas (fluctuate but are essential)

- Savings and investments: Emergency fund, Roth IRA, 401(k) contributions

- Debt repayment: Extra payments above minimums on loans or credit cards

- Discretionary spending: Dining out, entertainment, shopping, subscriptions

- Irregular expenses: Annual subscriptions, car maintenance, medical (divided by 12 for monthly allocation)

Step 3: Assign Every Dollar

Now assign your income to the expense categories until you reach zero. Start with your most important categories: housing, food, utilities, minimum debt payments. Then allocate to savings and investments. Finally, assign what’s left to discretionary spending.

If you reach zero and still have categories unfunded, you need to reduce discretionary spending. If you assign everything and have money left over, give that money a job — put it in savings, invest it, or apply it as extra debt payment. Nothing should be “leftover.”

Step 4: Track Your Spending Throughout the Month

As you spend money during the month, track each transaction against its assigned category. When a category is empty, stop spending in that category until the next month. This real-time tracking is what makes zero-based budgeting so powerful — you always know exactly how much you have left in each category.

Step 5: Adjust and Roll Over

If you underspend a category (say you budgeted $300 for groceries and only spent $240), you have $60 left. In zero-based budgeting, this money doesn’t disappear — you reassign it to another category or add it to savings. At the end of the month, you start fresh for the next month with a new plan.

Zero-Based Budget Example: $4,000/Month Take-Home Pay

| Category | Type | Budgeted Amount |

|---|---|---|

| Rent | Need (Fixed) | $1,200 |

| Groceries | Need (Variable) | $350 |

| Utilities | Need (Variable) | $150 |

| Car payment | Need (Fixed) | $300 |

| Car insurance | Need (Fixed) | $120 |

| Health insurance | Need (Fixed) | $180 |

| Gas | Need (Variable) | $80 |

| Minimum debt payments | Need (Fixed) | $120 |

| Emergency fund | Savings | $200 |

| Roth IRA | Savings/Investment | $400 |

| Extra debt payment | Debt payoff | $200 |

| Dining out | Want | $150 |

| Entertainment | Want | $100 |

| Clothing/Shopping | Want | $100 |

| Subscriptions | Want | $50 |

| Total | $4,000 = $0 remaining |

Every dollar is assigned. Nothing is wasted. Nothing is unaccounted for. This is zero-based budgeting in action.

Advantages of Zero-Based Budgeting

1. Maximum Awareness of Your Spending

Zero-based budgeting forces you to confront every dollar you spend. There is nowhere for money to quietly disappear. Most people who switch to ZBB are shocked to discover how much they were spending on small, untracked purchases — subscription services, impulse buys, small daily purchases that add up significantly over a month.

2. Eliminates Mindless Spending

When every dollar is pre-assigned, you have to make a conscious decision before spending. You know exactly what you’re giving up when you buy something — if your entertainment budget is empty and you want to go to a movie, you have to take money from another category. This friction reduces impulse spending significantly.

3. Accelerates Debt Payoff and Savings Goals

Because zero-based budgeting ensures every dollar is intentionally assigned, it typically accelerates progress on financial goals. Money that was previously “disappearing” into untracked spending can now be redirected to debt payoff or savings. Many people who adopt ZBB find they can pay off debt significantly faster and build savings more quickly than they expected.

4. Adapts to Irregular Expenses

Zero-based budgeting handles irregular expenses well. You can create a “sinking fund” for predictable irregular expenses — divide the annual cost by 12 and set aside that amount each month. For example, if your car registration costs $240 per year, you budget $20 per month to a “car registration” category. When the bill arrives, the money is already waiting.

5. Works for Any Income Level

Zero-based budgeting scales to any income. Whether you earn $2,000 or $20,000 per month, the principle is the same: assign every dollar a job. At lower incomes, it helps ensure every dollar is used as effectively as possible. At higher incomes, it prevents lifestyle creep and ensures wealth is being built intentionally.

Disadvantages of Zero-Based Budgeting

1. Time-Intensive Setup

Creating a zero-based budget from scratch each month takes 30 to 60 minutes. For some people, this feels like too much effort. The solution: use a budgeting app (like YNAB) that automates much of the tracking and category management, reducing ongoing time commitment significantly.

2. Challenging with Variable Income

If your income fluctuates significantly month to month (freelancers, commission-based workers, gig workers), zero-based budgeting can feel stressful when you don’t know exactly what you’ll earn. The workaround: budget based on your lowest expected income month, and treat any additional income as a bonus to assign to savings or debt.

3. Can Feel Restrictive

Some people find the granular detail of ZBB feels overly constraining, especially for the discretionary spending categories. If you’re used to spending freely, having a hard stop when a category hits zero can feel uncomfortable at first. This feeling usually passes within 2 to 3 months as the benefits become apparent.

Best Apps and Tools for Zero-Based Budgeting

YNAB (You Need a Budget) — Best Overall

YNAB is built specifically around the zero-based budgeting philosophy. Its four rules align perfectly with ZBB principles: give every dollar a job, embrace your true expenses, roll with the punches, and age your money. YNAB is the gold standard for zero-based budgeting apps but costs $14.99/month or $99/year.

EveryDollar — Best Free Option

Dave Ramsey’s EveryDollar app is designed specifically for zero-based budgeting and offers a free tier. The free version requires manual transaction entry, while the premium version ($17.99/month) automatically syncs with your bank. It’s simpler than YNAB and ideal for beginners.

Google Sheets or Excel — Best Free DIY Option

A simple spreadsheet with income and expense categories works perfectly for zero-based budgeting. It requires manual entry but costs nothing. Create a template with your income at the top, list all categories below, and track the running total until it reaches zero. Check our guide on the best budgeting apps for 2026 for a full comparison of all options.

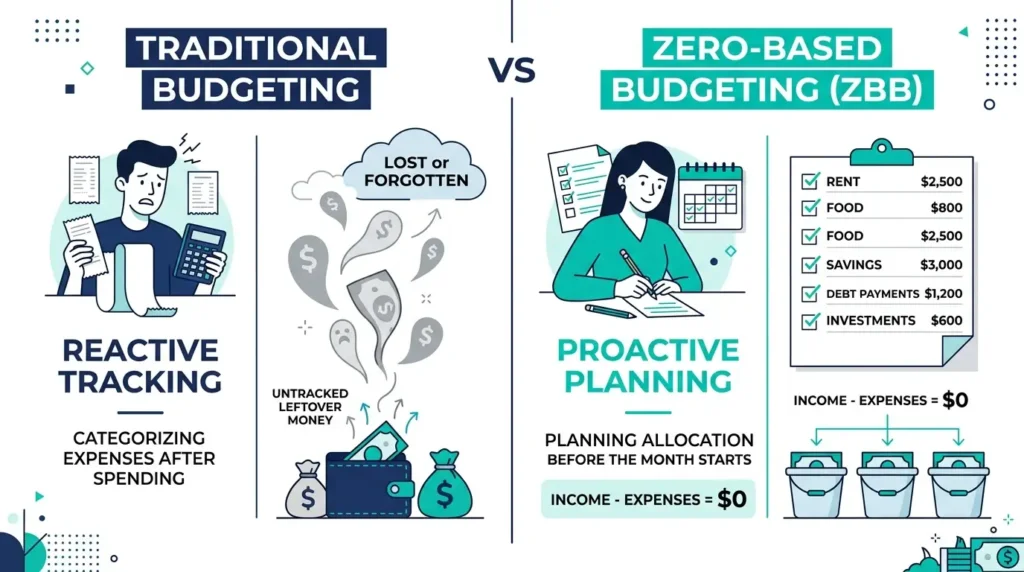

Is Zero-Based Budgeting Right for You?

Zero-based budgeting is the right choice if:

- ✅ You’re trying to pay off debt aggressively

- ✅ You feel like money disappears without knowing where it goes

- ✅ You have specific financial goals (house down payment, emergency fund, etc.)

- ✅ You’re willing to invest 30 to 60 minutes per month in financial planning

- ✅ You want maximum control and awareness of your finances

A simpler approach like the 50/30/20 rule may be better if:

- ✅ You prefer a low-maintenance budgeting system

- ✅ Your finances are already in good shape

- ✅ You find detailed tracking overwhelming or unsustainable

- ✅ You just want to ensure you’re saving 20% and living within your means

Frequently Asked Questions About Zero-Based Budgeting

Does zero-based budgeting mean spending all your money?

No — this is the most common misconception. Zero-based budgeting means giving every dollar a purpose, including savings and investments. If you earn $4,000 and budget $800 for savings, that $800 is “assigned” to savings — your budget still reaches zero, but you’re not spending all your money. You’re saving it intentionally.

How long does it take to create a zero-based budget?

Your first zero-based budget may take 60 to 90 minutes as you set up categories and figure out your actual spending patterns. Once the system is established, monthly maintenance typically takes 20 to 30 minutes for planning plus a few minutes each day or week for tracking transactions.

What if I forget to track a purchase?

Add it when you remember and adjust. Zero-based budgeting is not about perfection — it’s about intentionality. If you miss a few transactions, your budget won’t be exactly at zero, but the planning and awareness benefits are still significant. Budgeting apps like YNAB help by sending reminders and allowing quick entry from your phone.

Can I use zero-based budgeting if I’m paid bi-weekly?

Yes. You can either budget monthly (combining your two bi-weekly paychecks) or budget by paycheck. Budgeting by paycheck is actually easier for many people — assign the first paycheck to bills and fixed expenses due in the first half of the month, and the second paycheck to variable expenses and savings.

What happens to money left over at the end of the month?

In zero-based budgeting, leftover money doesn’t disappear — you reassign it. Common options: add it to your emergency fund, make an extra debt payment, invest it, or roll it forward into next month’s budget as a buffer. The key is that it gets a deliberate assignment rather than silently evaporating.

The Bottom Line

Zero-based budgeting is the most powerful budgeting method for people who are serious about taking control of their money. By assigning every dollar a specific job before the month begins, you eliminate mindless spending, accelerate debt payoff, and build savings faster than almost any other financial strategy.

The time investment — about 30 to 60 minutes per month — is small compared to the financial clarity and control you gain. If you’ve ever wondered where your money goes, zero-based budgeting will answer that question definitively.

Start this month: calculate your income, list every expense, assign every dollar until you reach zero. Your first budget won’t be perfect — but it will be a transformative step toward financial control. If you prefer a simpler starting point, try the 50/30/20 budget rule first and graduate to zero-based budgeting when you’re ready for more precision. You can also explore the best budgeting apps for 2026 to find the right tool to make ZBB effortless.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Individual budgeting results vary based on income, expenses, and financial circumstances.